Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

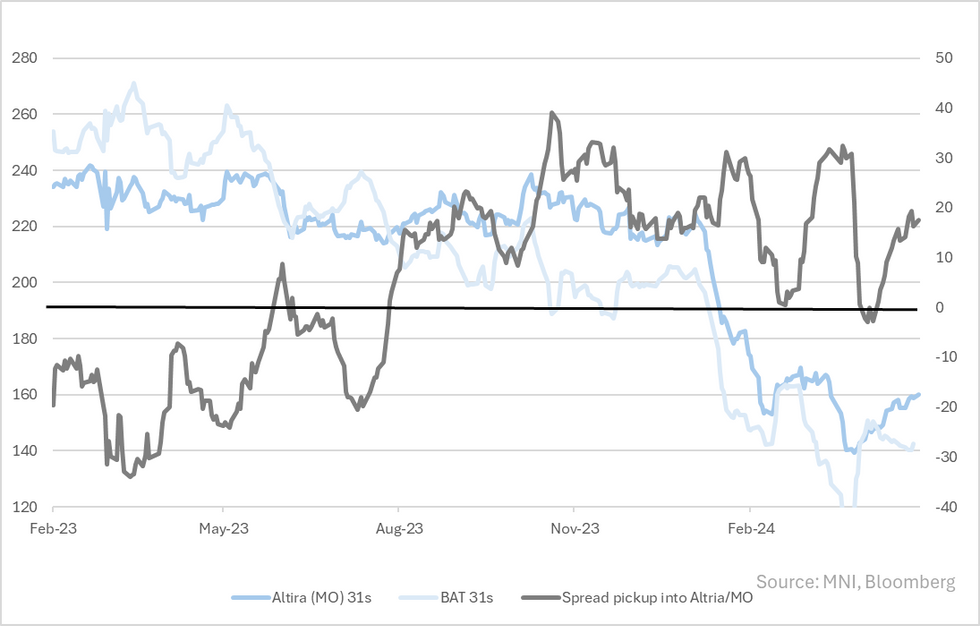

- Altria, a pure-play on US Tobacco, was given a outlook downgrade from Moody's last week. Curve already trades to BBB ratings but as we've noted multiple times its held firm in the face of BAT underperformance - a move we found a tad confusing on fundamentals. Signs of that reversing now (below).

- Moody's downgrade is on similar read-through as us on Q1 earnings; US volume headwinds in traditional combustibles not being offset by pricing. That is while it continues sizeable equity returns in the face of low (~14%) non-combustibles exposure.

- We'd again caution above BAT RV with 1) BBB tobacco tends to underperform on spread sell-offs & 2) BAT is more exposed to Euro area regulation (for e.g. impact see Ahold's headwind from Netherlands Tobacco retailing bans).

- BAT31s received the cold shoulder in primary last month - its still trading wide of pricing, which at the time came with a 20bp NIC. Tendering long-end and £ & $ skewed lines since (as part of its planned deleveraging) has done little to give support.

- As an aside on Altria, it does has a 8% stake in IG brewer AB Inbev {ABI BB Equity} valued at ~$9.5b.

Altria earnings from last month; https://marketnews.com/altria-mo-a3-bbb-pos-bbb-s-...

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok