Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWITZERLAND

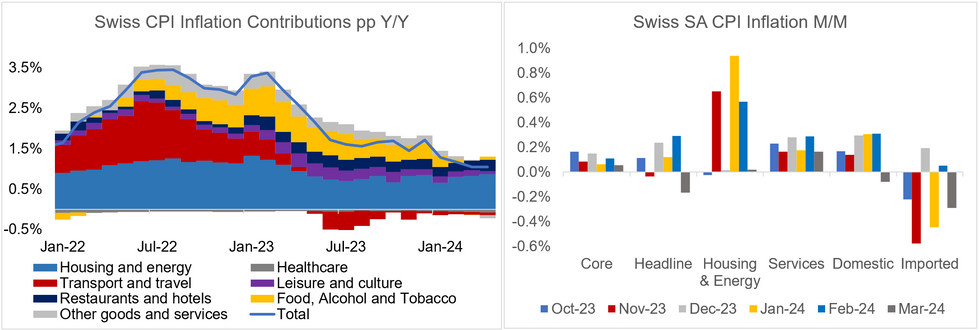

Swiss headline CPI inflation (released May 2 at 0730BST/0830CET) is expected to have accelerated in April after three consecutive slowdowns, with consensus standing at +1.1% Y/Y and +0.1% M/M (vs +1.0% and 0.0% in March, respectively). Core CPI is expected to have decreased further, however - consensus stands at +0.9% Y/Y (vs +1.0% Mar).

- Three categories will be in particular focus: housing, services, and imported inflation.

- Housing inflation has been the main driver of services and broader inflation in recent months (housing and energy category contributed over 0.8pp to the figure in March, see chart).For the past months, an anticipated uptick in housing inflation has only partially materialised - but a further acceleration is expected starting in April, reflecting a mortgage reference rate increase from December.

- Specifically, Raiffeisen Bank expects rental price inflation to increase to up to 8% Y/Y in the course of 2024 (vs 2.7% Mar).

- Imported inflation meanwhile went negative in the last months on a yearly basis (-1.3% Mar, -1.0% Feb), influenced by the stronger CHF. With the franc weakening since January 2024, it's plausible that the disinflationary impulse from imports will slow or reverse.

- Given that both these drivers would contribute upwardly towards the core measure, its projected deceleration is not immediately obvious to us - one potential downside risk to core would be a longer lag from the recent CHF depreciation, or if housing inflation once again fails to accelerate.

- While a headline figure in line with the 1.1% Y/Y consensus would start off the quarter well below the SNB forecast for Q2 of 1.4%, the projected uptick by the SNB might materialize at a later point, particularly when considering the housing price dynamics from above. The SNB forecasts a further uptick in Q3 (1.5% Y/Y).

MNI, SECO

MNI, SECO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok