Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

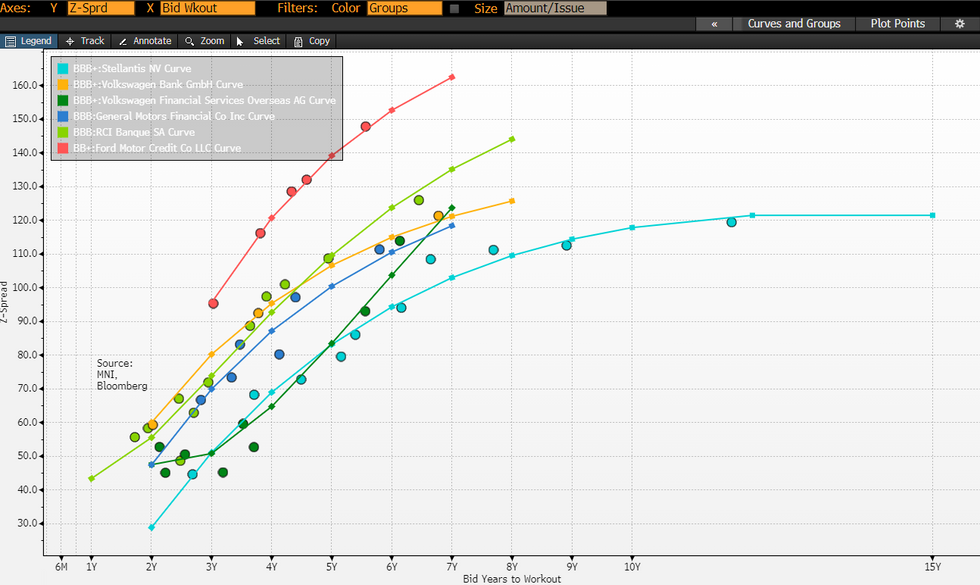

CONSUMER CYCLICALS

- GM reports 2Q24 results tomorrow.

- 1Q24 results were well received, featuring a 24% adj. EBIT beat and 4% FY24 guidance upgrade.

- FY Adj. EBIT consensus has moved up since, from $12.7bn to $13.9bn currently; that’s at the higher end of $12.5-14.5bn guidance.

- GM spreads have outperformed Stellantis by ~13bp over the past 3 months, driven mainly by STLA underperforming the sector with tight starting valuations.

- While the US OEMs have fared better than Europeans, the sector continues to face challenges including higher rates and extreme competition in China (34% of unit sales). Inventory has been building in the US which could lead to margin pressure.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok