Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

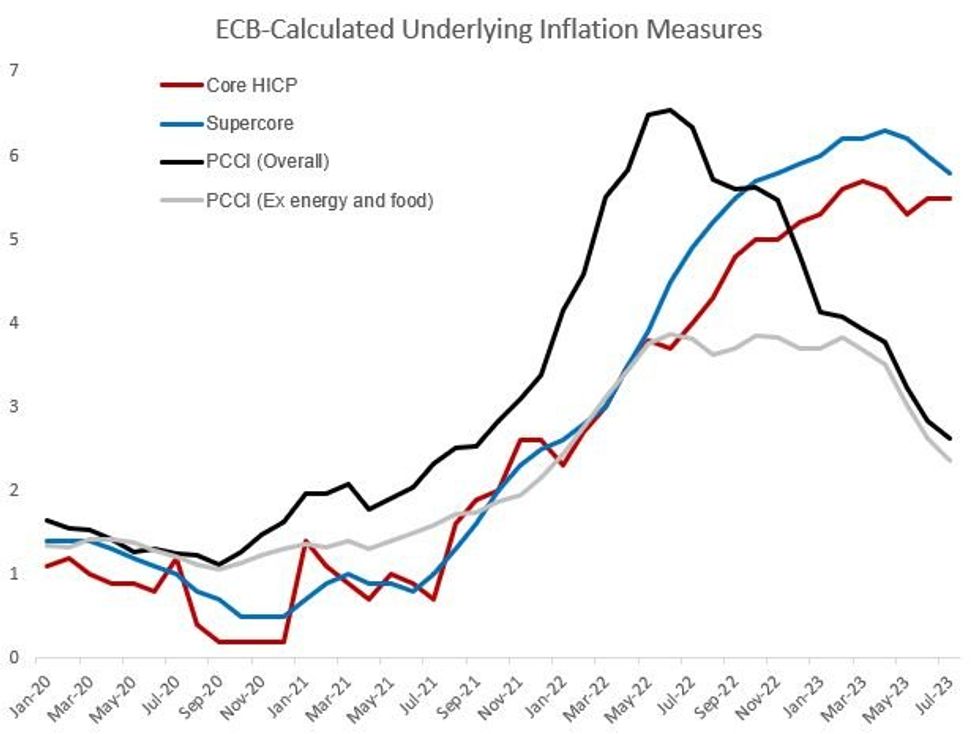

Over the weekend, the ECB published its estimate of Persistent and Common Component of Inflation (PCCI, a model-based approach) for July based on the final HICP reading. It showed continued sharp disinflation - overall Eurozone PCCI came in at 2.6% Y/Y (2.8% prior, 6.5% peak), ex-energy 2.8% (3.1% prior, 5.2% peak), and ex-energy/food 2.4% (2.6% prior, 3.8% peak). Those were the lowest readings since Sept 2021 for headline PCCI, and Dec 2021 for the two core measures.

- Based on a recent bulletin, ECB staff regard PCCI as a better (or at least as good) measure than any other underlying inflation indicator in terms of providing a medium-term forecast of the future headline HICP rate. It's also been mentioned several times by Pres Lagarde among other senior ECB members as one of the underlying measures they look at in setting policy.

- This is important as we go into the September ECB meeting as it provides more evidence that disinflation is set to continue in the months ahead, in addition to the trimmed mean/weighted median/Supercore measures that had previously been published (see our note here).

- It adds to the early August ECB finding that underlying inflation in the eurozone had probably peaked, and additional reason to shrug off stubborn Y/Y core (5.5% for the 2nd consecutive month in July, 7th in a row at 5.3% or above) in favour of a more forward-looking underlying metric.

- While next week's flash inflation readings will probably tip the balance, the downward momentum in PCCI is a key piece of ammunition for Governing Council doves who will be arguing for a hold next month (a 25bp hike is just over 50% market-implied) as they eye time to assess the impact of tightening already in the pipeline.

% Y/YSource: ECB, MNI

% Y/YSource: ECB, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok