Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

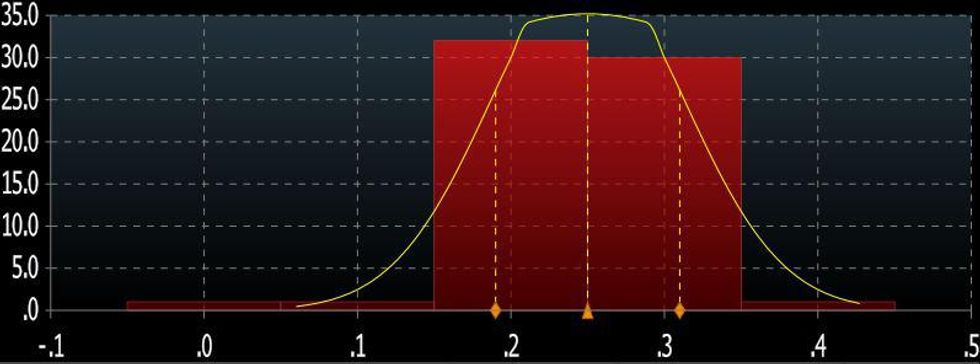

The Bloomberg survey median expectation for M/M September headline CPI is +0.3% (average 0.33%, std deviation 0.06%, range of 0.1-0.4%) and for core is 0.2% (average 0.25%, std deviation 0.06%, range of 0.0-0.4%, see chart below). In August, headline CPI came in at 0.3% while core was 0.1%. Y/Y, headline seen steady at 5.3% (5.3% prior), and core 4.0% (4.0% prior).

- For core, the average of 0.25% suggests an almost even split of opinion between 0.2 and 0.3%, and a reading inside 0.1-0.4% probably wouldn't be much of a market mover. And the the 0.4pp range is consistent with the survey estimates since June, though wider than the more typical 0.2pp range pre-pandemic.

- On the sell-side, above-consensus expectations for core CPI point to a re-acceleration of used car prices, with continued gains in housing costs. Some are also looking at new vehicle prices in this regard.

- Below-consensus expectations see used car prices impacting CPI only with a lag (ie showing up in Oct and beyond), while airfares/hotel prices are also seen negatively impacted by Delta effects.

Distribution Of Estimates For Sept Core CPI % M/MSource: Bloomberg Survey

Distribution Of Estimates For Sept Core CPI % M/MSource: Bloomberg Survey

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok