Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

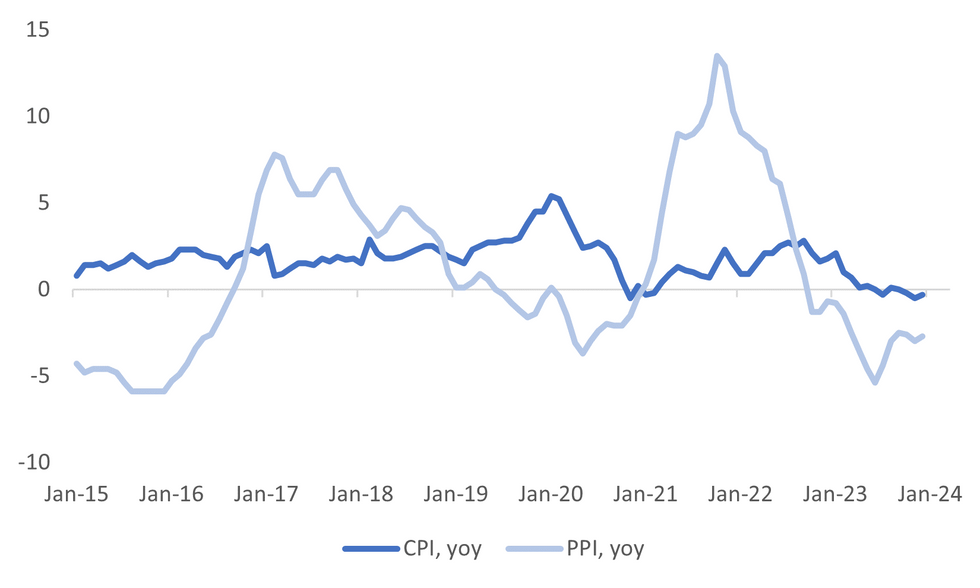

China Dec inflation outcomes were close to expected. The headline CPI fell -0.3% y/y (-0.4% forecast and -0.5% prior). In m/m terms we rose 0.1%, the first rise since September last year. Consumer goods were -1.1% y/y, services +1.0% y/y. Food prices were 0.5% y/y, non-food at -3.7% y/y, both slight improvement on Nov outcomes. Core (ex food & energy) was unchanged at 0.6% y/y.

- By product for CPI, there weren't a great deal of shifts versus Nov outcomes. Food and transport & communication were the biggest drags both down around -2% y/y. Positives remained in terms of clothing, medical care and recreation.

- On the PPI side, we were slightly weaker than expected at -2.7% y/y (-2.6% forecast, -3.0% prior). Again, there wasn't much shift from Nov trends in terms of the detail. Mining at -7.0% y/y remains the biggest drag, while manufacturing was -3.2% y/y. Consumer goods remained at -1.4%, weighed lower by food and durables.

- The data shouldn't really shift the macro narrative, albeit that deflation pressures didn't get any worse through the tail end of 2023 for China.

- As we noted earlier, market expectations are for a 10bps cut in the 1yr MLF on Monday.

Fig 1: China CPI & PPI Y/Y

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok