Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS

The weak 30Y auction comes in the first refunding since last week's quarterly Treasury supply announcement, which was seen as less onerous than anticipated, particularly the implication that next quarter's coupon size increases were envisaged as being the last.

- Still, the duration that the market is being asked to absorb is significant - the $24B of 30Y nominal sold was below the pandemic highs of $27B but at that time the Fed was engaging in QE.

- The roughly $38B DV01 / $48B 10Y equivalent DV01 represented by yesterday's 30Y auction may have been lower than the net impact of those 2021 auctions (the Aug 2021 auction which was the last $27B was around $70B 10Y equivalent), but again the Fed was buying $8B monthly on the secondary market. The backdrop is less accommodative now.

- The 30Y auction showed a continued lack of end-user demand (see the high dealer takeup previously referenced), mirroring similar results in October's poor sales - the 3Y, 10Y, and 30Y auctions all tailed over 3 consecutive days, each showing higher primary dealer takeup.

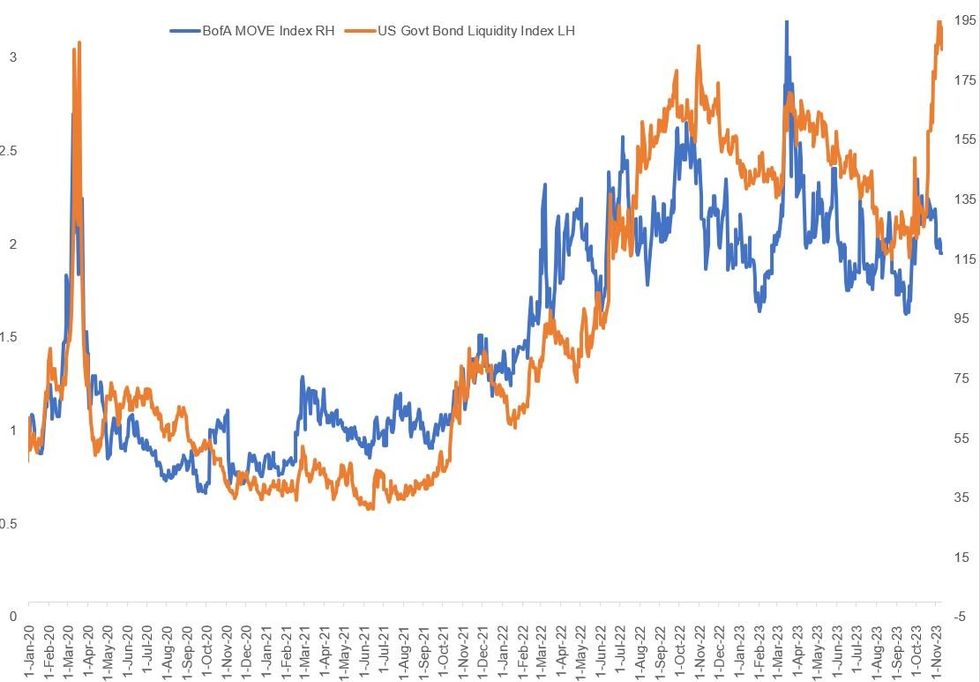

- To be sure, the 10Y sale this week saw only a modest tail, with decent periphery stats. And in terms of broader dislocations, we haven't really seen many major cracks appearing in Treasury markets apart from the sharp drop in prices. Fed facility usage remains unremarkable, while implied Tsy option volatility has been well behaved (see BofA MOVE).

- But greater volatility is testing liquidity (see the Bloomberg-calculated Gov't Bond Liquidity Index, which calculates persistent Tsy yield errors vs a fitted curve, which hit levels this week indicating even less liquidity than in 2020's pandemic panic). In that sense, with yields fluctuating so significantly, it's probably no surprise to see such a messy auction.

- As such the backdrop keeps primary issuance at the forefront for the next couple of months, with the 20Y sale on the 20th set to be the next major test.

Source: BofA, BBG, MNI

Source: BofA, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok