Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

(MNI Australia) Not surprisingly, the market has fairly downbeat expectations heading into tomorrow's monthly run of China activity prints for November. Consumer related segments are expected to remain particularly weak, along with property activity.

- Softer data outcomes in recent weeks haven't impacted China asset related sentiment though as the market focuses on the shift away from CZS. Still, weakness could extend in the near term, as the current wave of covid cases weighs on activity and places pressure on the health system.

- In terms of tomorrow's prints, Industrial production growth is expected to slow to 3.5% y/y (forecast range: 2.5% to 5.5%) from 5.0% in October.

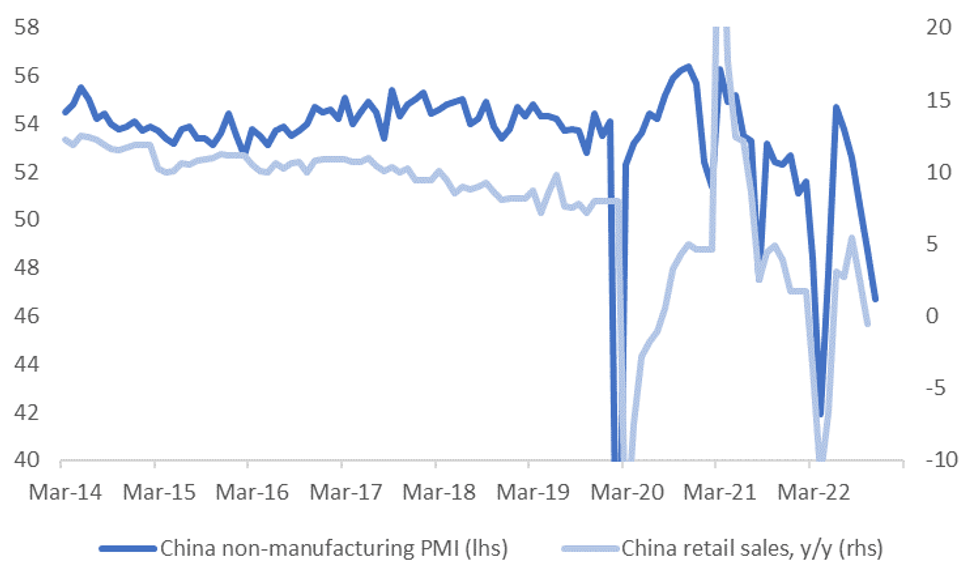

- Retail sales is forecast at -4.0% y/y (forecast range: -1.1% to -5.5%), versus -0.5% prior., see the chart below of the official non-manufacturing PMI and retail sales y/y.

- Fixed asset investment is forecast at 5.6% YTD y/y (forecast range: 5.4% to 5.8%), while property investment is expected to ease further to -9.2% YTD y/y (forecast range: -8.8% to -9.5%)

- The jobless rate is expected to nudge up to 5.6% from 5.5%, (forecast range: 5.5% to 5.7%).

- The 1yr MLF rate is also expected to be held unchanged at 2.75%, with no forecasters expecting a shift, while the rollover amount is expected lower at 500bn yuan (forecast range: 400bn to 800bn yuan). The previous amount was 850bn yuan.

- New home prices also print, there is no market forecast, -0.37% m/m was the prior.

Fig 1: China Non-Manufacturing PMI & Retail Sales Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok