Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KOREA

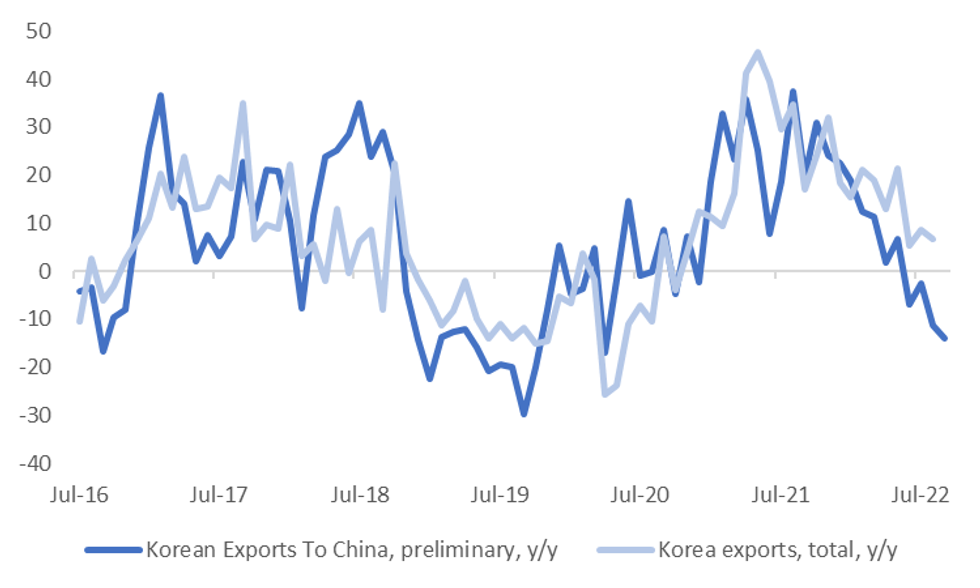

The headline drop in exports for the first 20-days of September of -8.7% y/y looks awful but the detail is not as bad. After accounting for fewer working days this September, average daily exports were +1.8% y/y. Chip exports also rose 3.4% y/y, which has been a recent source of weakness. There is also some light at the end of the tunnel for the trade deficit position.

- The country level detail showed China exports fell by -14% y/y, while to the US were down 1.1% y/y for the first 20-days. This shows that medium term headwinds to export growth persists though, amidst a weaker growth backdrop for China, see the chart below.

Fig 1: South Korea Exports - Total & China y/y

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

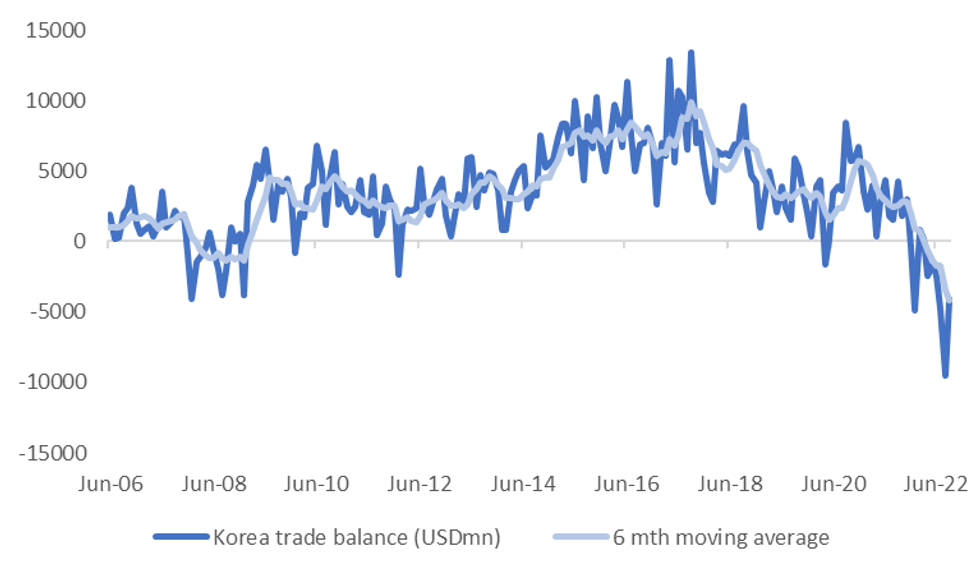

- The trade deficit was still wide at -$4.1bn for the first 20-days, but well in compared to August levels (-$10.2bn).

- Given the fact the full trade position for the whole month tends to improve on the first 20 day reading, we could see even further improvement once the data for the whole of September is released (October 1).

- The longer term trend still looks poor, see the second chart below. It may also be too early to declare victory. Recall earlier in the week reports suggested the country is on track to fill LNG reserves to 90% by November. Such flows should keep the energy import bill higher, all else equal, and by extension the trade deficit wider.

Fig 2: South Korean Trade Balance Trends

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok