Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CREDIT MACRO

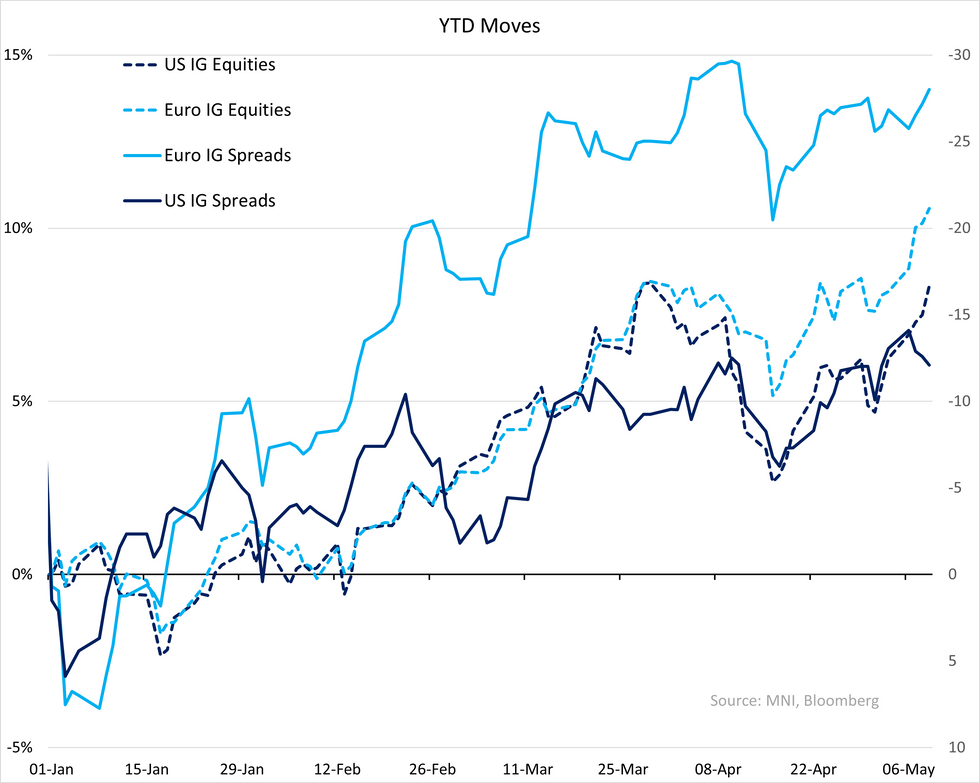

S&P futures +0.3% in low vol, CDX a tad tighter, $IG opening tighter as primary clears out. ETF flows were net flat yest.

- Firm inflows across credit bar small outflows in £IG. No surprise given the resilience we saw in secondary. €IG held relatively firm on Tuesday's primary pick-up & $IG is only +1 over the week as it went through just under half of May's expected supply (bbg surveyed).

- Next weeks supply expectations reflect the local hold back for 3 public holidays. €/£ IG & HY (incl. covered) at ~€30b up from the ~€10b expected this week (actual €18b) & $IG at $25-$30b down from $30b last week (actual $55b)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok