Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

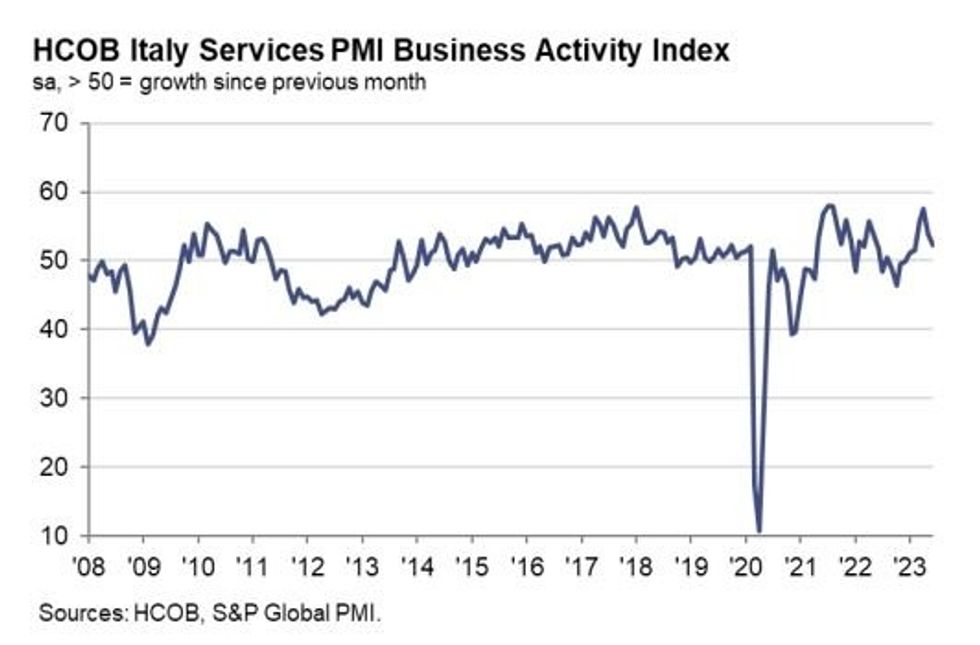

Italian PMI disappointed in June, posting a 52.2 reading (vs 53.1 expected and 54.0 prior), which combined with the weak manufacturing PMI (43.8) released Monday meant the composite reading fell into contractionary territory (49.7 vs 51.0 expected, 52.0 prior) for the first time this year (since December 2022).

- Overall while the headline Services figure showed continued expansion, there were evident signs of weakness in the key sector. Most notably throughout the report, rising interest rates are cited as a factor in weaker activity and sentiment, suggesting that the ECB's tightening is having an impact on Italian output.

- In contrast to the below-expected Spain Services PMI reading released earlier, Italian sentiment fell to a 6-month low with cited concerns including higher borrowing costs, recession fears and inflation persistence. Indeed, the Spanish report doesn't mention interest rates as a factor at all.

- On inflation, input costs hit the lowest in 2 years, though wages reportedly rose and suppliers were seen pushing price increases. Average output price inflation weakened to the lowest level since Oct 2021.

- New business growth while expansionary was the softest of the year so far (again on rising interest rates and widening economic activity).

- Services firms kept up hiring to relieve backlogs but the net rise in employment was weaker, and "there were some reports of the non-replacement of leavers given an uncertain outlook".

Source: HCOB, S&P Global

Source: HCOB, S&P Global

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok