Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

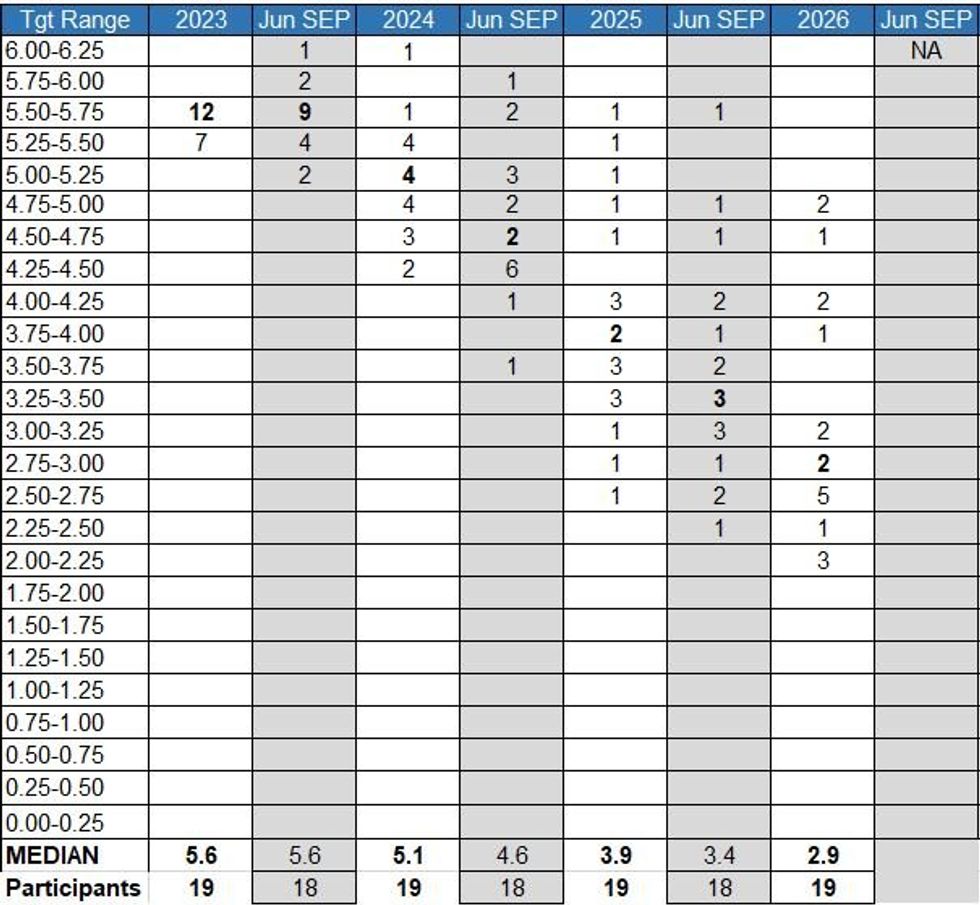

Below is how the distribution of dots for the median Fed Funds rate looks now versus the June SEP. A few standouts here:

- No FOMC participant is looking for 2 more hikes in 2023 but a comfortable 12-7 majority is looking for at least 1 more hike. This basically just shifts the top 3 dots lower and the bottom dots higher from the June projections, so no big change - just mark-to-marking that one hike has already happened and there are only 2 meetings left after this. But it underpins the tightening bias.

- For 2024, the distribution shifts higher along with the 50bp median increase to 5.1% - the lower dot goes from 3.6% to 4.4%, and the top dot goes to 6.1%. in other words, at most, the biggest dove sees either 4 or 5 quarter-point cuts next year, while at least one sees rates rising in 2024.

- For 2025 the distribution doesn't really move that much higher despite the 50bp rise in the median: it's a range of 2.6-5.6%, vs 2.4-5.6% prior.

- 2026 there are no real surprises, 11 of 19 members see rates below 3% and thus toward the longer run rate.

- For the longer-run dot which stays at 2.50%: we've gone from 7 to 8 dots at 2.50%, with 3 remaining at the bottom 2.375% and 2 staying at 2.625%, 1 staying at 3.00%, 1 at 3.25%, and 1 at 3.50% (new). The upper dot has moved from 3.625% to 3.75% where we have 2 dots. There is no longer a dot at 3.625%. There are only 18 dots in this column so presumably the St Louis Fed continues to not submit a longer-run dot despite the departure of Pres Bullard who conventionally did not submit a L-R dot.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok