Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

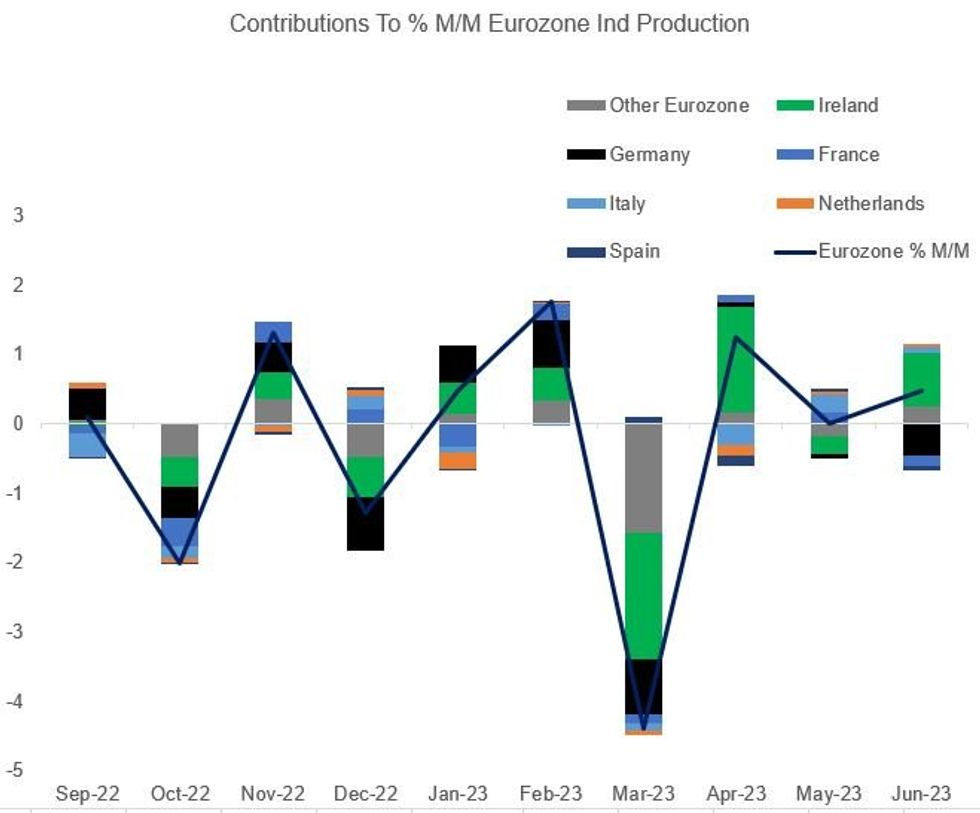

Based on the headline data, Eurozone industrial production beat expectations in June, rising 0.5% M/M (0.0% survey, 0.0% prior revised from +0.2%) and contracting 1.2% Y/Y (-4.0% survey, -2.5% prior revised from -2.2%).

- But the monthly rise obscures a much weaker picture, with most categories of production down both month-on-month and year-on-year: durable consumer goods fell by 0.1% M/M / 5.2% Y/Y, intermediate goods by 0.9% M/M / 6.3% Y/Y. and non-durable consumer goods fell by 1.1% M/M / up 0.2%. The mixed exceptions were energy production, which grew by 0.5% M/M but fell 7.8% Y/Y, and capital goods which declined by 0.7% M/M / rose by 4.4% Y/Y.

- June's data again highlights a key factor that muddies analysis of the short-term dynamics in IP: Ireland's (6% of Eurozone IP weighting) contribution was outsized, growing 13.1% M/M (after -4.5% in May, +25.7% in April, and -31.3% in March), while heavier hitters such as Germany (-1.3% M/M, nearly 40% of IP weighting), France (-0.9% M/M), and Spain (-0.9% M/M) all saw bigger contractions than the EZ aggregate.

- Removing Ireland's contribution of 0.8pp to the headline M/M figure brings the eurozone aggregate down to -0.3%. The Irish statistics agency is "carrying out a review of the seasonal adjustment methodology" for IP, but in the meantime, the monthly aggregate eurozone numbers are effectively a random walk.

- The broader picture is that while it has recovered slightly from 2023 lows, Euro area industrial production has basically flatlined since the pandemic and the level of activity is no higher than it was in 2017.

- With manufacturing weakness appearing to persist from IFO and PMI survey data, eurozone industry looks very much in recession.

Source: Eurostat, MNI Calculations

Source: Eurostat, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok