Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

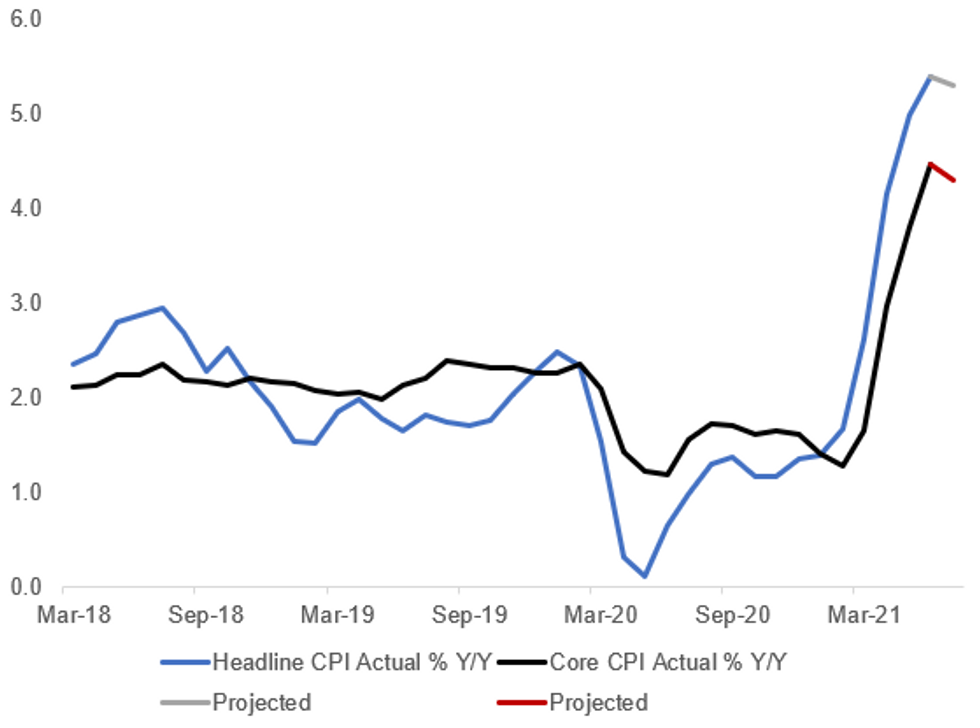

U.S. CPI growth likely slowed in July, with the Bloomberg survey median pointing to a 0.5% M/M gain following June's 0.9% increase. CPI is seen rising 5.3% Y/Y after rising 5.4% in June. (PDF preview)

- Ex-food and energy median is +0.4% M/M vs +0.9% June, with Y/Y 4.3% vs 4.5% in June.

- Probably most closely eyed in the release will be the sequential progression of core M/M CPI: the range of estimates runs from 0.2-0.6%, with avg 0.44% and standard deviation of 0.09%.

- A common theme in analysts' expectations for the July reading is for energy prices keeping headline CPI elevated, whereas "transitory" components such as used car prices set to see waning core upside pressures (though others such as airfares may continue to underpin).

- On the flipside, there's a close focus on shelter prices - which is seen as the biggest upside risk to the overall "transitory" narrative into year-end and 2022.

- Some are eyeing idiosyncratic categories that capture re-opening price pressures / labor passthrough: for example, restaurant prices.

Source: BLS, BBG, MNI

Source: BLS, BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok