Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

DATA REACT

Lots of positives from the July payrolls report which will further encourage the FOMC to acknowledge that "substantial further progress" has been achieved on employment by the time the September meeting rolls around, so long as the August report doesn't unduly disappoint.

- The +943k payrolls added and upward revisions mean the US economy is now 5.7mn jobs short of pre-pandemic levels (146.8mn vs 152.5mn). Gov Waller, for one, said yest that 800k-1mn in Jul and Aug would constitute "substantial" progress for a September taper announcement.

- The main U-3 unemployment rate came in much lower than expected, at 5.4% (5.7% expected, 5.9% prior). As a benchmark: the June Fed SEP median forecast was 4.5% end-year.

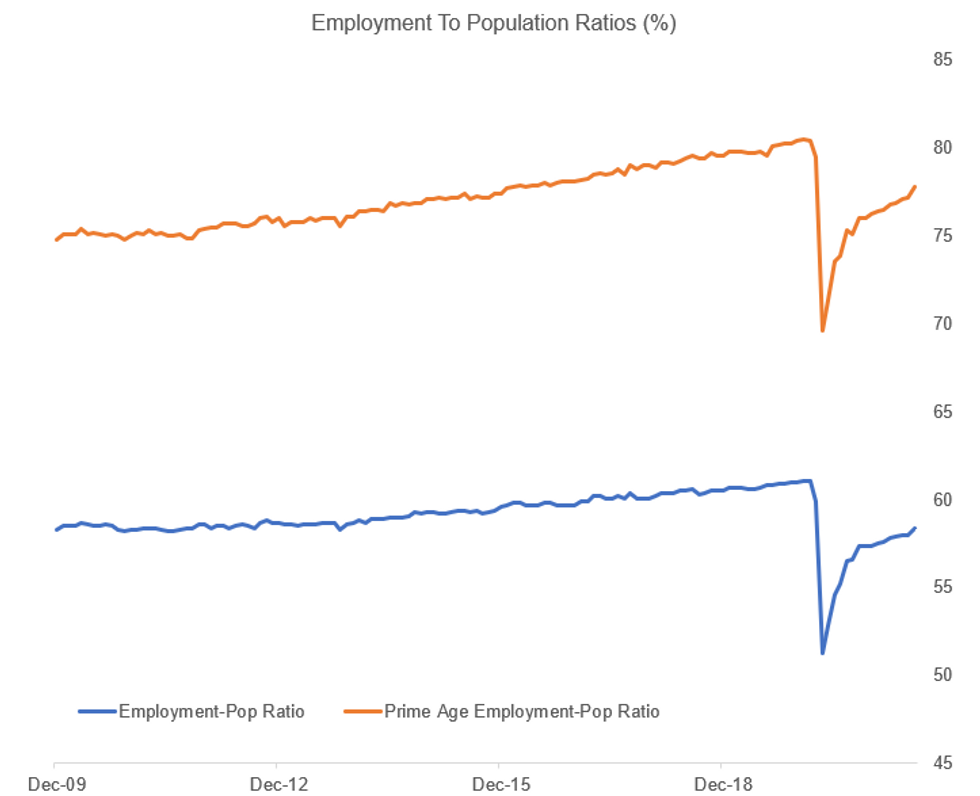

- The fairly steady (participation rate (+0.1pp to 61.7%) was a bit confounding, with the labor force growing by just 261k - but the Fed will be encouraged by the biggest rise in the employment-to-population ratio since October (+0.4pp to 58.4%, vs pre-pandemic peak of 61.1%). For prime age workers (25 to 54), the ratio rose 0.6pp (to 77.8%, vs pre-pandemic peak of 80.5%).

- U-6 Underemployment fell sharply to 9.2% (from 9.8% prior).

- Re the Fed's concern over the breadth of the recovery from pandemic, there were some positives here too: Black and Hispanic unemployment fell by 1.0pp (9.2%) and 0.8pp (6.6%) respectively, while leisure and hospitality jobs gained 380k. And long-term unemployed dropped 600k from June.

- Maybe taking the shine off a bit: government payrolls contributed heavily: +240k. Private payrolls were revised up in June by 107k but a higher base meant they came around in line with expectations in July, +703k vs 709k survey. The education sector (private + public) lost 1.01mn jobs non-adjusted, but that was +271k seasonally adjusted.

Source: BLS, MNI

Source: BLS, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok