Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

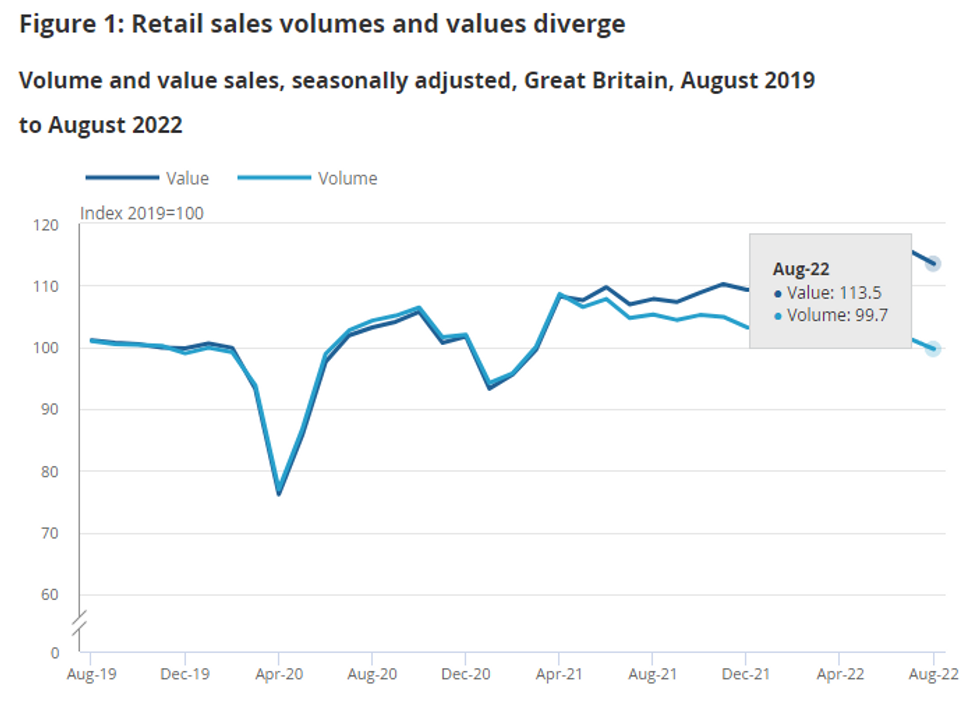

UK AUG RETAIL SALES INCL FUEL -1.6% M/M (FCST -0.5%); JUL +0.4%r M/M

UK AUG RETAIL SALES INCL FUEL -5.4% Y/Y (FCST -3.7%); JUL -3.2%r M/M

- UK retail sales recorded a contraction across all main sectors in August, the first time in over a year (following 2021 summer re-opening effects).

- Sales incl. auto contracted more than anticipated, by 1.6% m/m and by 5.4% y/y, with retail ex. auto closely following as inflation woes weigh on consumer demand.

- In order for UK retail sales to generate a flat contribution to Q3 GDP, sales need to be at 3.1% or above in September- an unlikely feat.

- Ahead of the UK markets opening, sterling was trading lower against the pound, falling to a near 40-year low on the data at $1.1418 -- just above the $1.1410 seen on Sept.

- Markets are pricing the growing likelihood of a Q3 recession (BOE anticipates Q4 as the kick-off) however the BOE will unlikely be swayed ahead of the meeting next Thursday, where at least another 50bp remains firmly in the picture.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok