Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

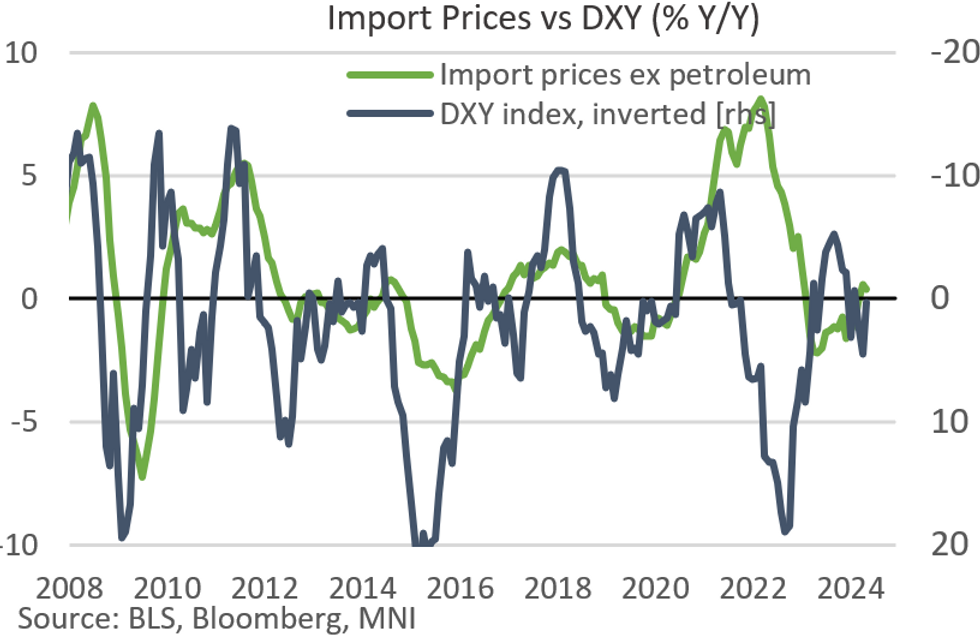

Import Prices ex-Petroleum pulled back more sharply than expected in May, to -0.3% M/M (+0.2% expected, +0.6% prior rev from +0.7%), the lowest since June 2023. Overall, import prices fell -0.4% M/M (-0.1% expected, +0.9% prior unrev), the lowest since December 2023.

- From an inflation perspective, we took special note of the sharp fall pullback in industrial supplies/materials ex-petroleum (-0.7% M/M vs +2.7% April - 23% of the Index), with moderation in capital goods imports (28% of the index) to -0.1% (+0.1% prior) and consumer goods ex-automotives (-0.2% M/M (-0.1% prior - 17% of the index).

- Note that there is no seasonal adjustment to these figures, though so it is tough to draw conclusions from the sequential data apart from suggesting that April's jump was a one-off.

- The Y/Y comparison is arguably of greater importance on a comparative basis: ex-petroleum import prices rose by 0.4% Y/Y, a downtick from 0.6% in April and quite soft, though still above the negative prints through most of 2023 and Q1 2024. The relatively steady dollar on a Y/Y basis and supply chain pressures flattening out vs post-pandemic fluctuations imply relatively steady ongoing import price pressures.

- On the other side of the ledger, export prices pulled back sharply as well, to -0.6% M/M from +0.6% prior.

- Overall, this report will be seen dovishly by policymakers for two reasons: first, with Fed chair Powell singling out the unusual recent uptick in import prices and the impact on core goods inflation, this will add marginally to evidence from May's CPI and PPI reports that inflation moderated last month. Second, May core PCE tracking estimates (which ranged from 0.10-0.17% coming into the report) will be biased slightly downward if anything after this reading.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok