Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

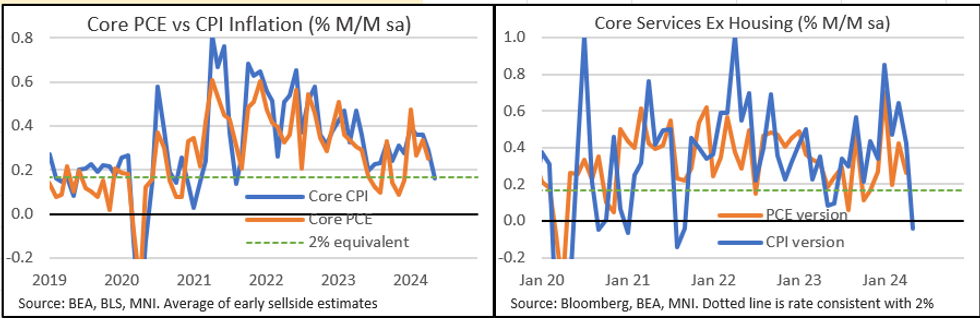

Today's PPI report (0830ET/1330UK) will as usual have implications for the Fed's preferred PCE inflation gauge, which for May is due out at the end of this month (Jun 28):

- Wednesday's large miss on CPI drove downward revisions to analysts' pre-release expectations for PCE, which now sits right around the 0.16% M/M core CPI reading we got yesterday - pending PPI today. That's a little unusual: in the 12 prior months, M/M core PCE has only exceeded core CPI twice, and not since January. On average over that period, CPI has exceeded PCE by 7bp (0.30% vs 0.23%).

- That's because the core CPI drop was driven in large part by downside surprises in auto insurance and airfares. PCE uses different measures for each of these categories, from the PPI report. In addiition, the PCE auto insurance measure has been softer than CPI's due to methodological differences.

- That puts attention squarely on airfares, auto insurance, and other categories that go from PPI>PCE (portfolio management, healthcare services) today.

- In April's PPI report, auto insurance rose by 0.12% M/M; portfolio management by 3.94%, healthcare services by 0.15%M/M; airfares dropped by 3.76%. All are subject to revisions.

- For the broader PPI aggregates: headline is seen decelerating +0.1% M/M (+0.5% prior), ex-food/energy at +0.3% M/M (+0.5% prior), and ex-food/energy/trade at +0.3% M/M (+0.4%).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok