Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Duration Extends Sell-Off After Bell

Myriad Fed speakers continued to tow the Fed company line pre/post the release of the March FOMC minutes Wednesday.

- Fed Pres' Evans, Kaplan, Barkin, Daly and Fed Gov Brainard all see a brighter economic outlook ahead, transitory inflation pressures still a sign of improving strength while "participants reaffirmed the Federal Reserve's commitment to using its full range of tools to support the U.S. economy during this challenging time."

- Meanwhile Tsy Sec Yellen released a report proposing to raise $2.5T in tax revenue over 15 years, aiming to pay for President Joseph Biden's infrastructure plan, reduce inequality and curtail corporate profit shifting.Tsy Link

- Long bonds made new lows after the bell, loosely mirroring a late drop in equities off near record highs (ESM1around 4063.0 after the FI close). Yld curves bent steeper, but still well off late Feb highs with 5s30s around 148.50 after the bell.

- Large Eurodollar futures and option flows: Block: 20,000 Red packs (EDM2-EDH3) at +0.0175 from 1032-1043ET, most likely swapped but not seeing other side. Taking a stand on Summer 2023 volatility: near +40,000 Green Jun 92 straddles from 21.25 to 22.5.

- The 2-Yr yield is down 0.8bps at 0.1586%, 5-Yr is down 5bps at 0.8721%, 10-Yr is down 4.3bps at 1.6578%, and 30-Yr is down 2.6bps at 2.3207%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settles

- O/N -0.00163 at 0.07625% (+0.00150/wk)

- 1 Month +0.00237 to 0.11250% (+0.00212/wk)

- 3 Month -0.00375 to 0.19363% (-0.00612/wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00900 to 0.21000% (+0.00875/wk)

- 1 Year -0.00100 to 0.28525% (+0.00475/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $255B

- Secured Overnight Financing Rate (SOFR): 0.01%, $979B

- Broad General Collateral Rate (BGCR): 0.01%, $378B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $349B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, appr $6.001B accepted vs. $19.337B submission

- Next scheduled purchases:

- Thu 4/08 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

- Fri 4/09 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

US TSYS/OVERNIGHT REPO: Holding steady

Holding steady to Monday's levels, 10s lead specials. Bills reverse Monday bounce, current levels:

T-Bills: 1M 0.0101%, 3M 0.0101%, 6M 0.0330%; Tsy General O/N Coll. 0.04%

| Duration | Current | Old Issue |

| 2Y | 0.03% | 0.03% |

| 3Y | -0.26% | -0.17% |

| 5Y | 0.00% | -0.13% |

| 7Y | 0.02% | -0.08% |

| 10Y | -0.70% | -0.11% |

| 30Y | -0.24% | -0.02% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +40,000 Green Jun 92 straddles from 21.25 to 22.5

- -20,000 short Dec 91/93 put spds, 3.5 vs. 99.545/0.16%

- +5,000 short Sep 95/96 put spds 0.5 over the Red Sep 90/91/95/96 put condors

- +5,000 Gold Sep 73/76 3x2 put spds, 4.0

- +5,000 Green Sep 85/90 put spds, 22.0

- +10,000 short Sep 91/93/96 put flys, 3.0

- Update, total -20,000 short Dec 97/98 call spds, 1.0

- +2,700 Green Dec 75/80/85 put flys, 5.0

- -3,000 Blue Jun 80/82/85 put flys, 4.0

- +10,000 Green Jun 91/93 put over risk reversals, 0.5

- +3,600 TYM 134 calls, 11

- +2,000 TYM 127.5/129.5 2x1 put spds, 5

- 3,600 TYK 131/132.5 call spds, 47

- Overnight trade

- Block, +10,000 TYM 133 calls, 19

EGBs-GILTS CASH CLOSE: Eventful Session For Vaccines And Supply

A very busy session saw an early move into safe havens fade, but Bunds and Gilts ended stronger nonetheless. Periphery spreads ended a little wider, with large demand for BTP syndication.

- Syndications today: Italy sold new 50-yr BTP (E7bn) and tapped 7-yr syndication (E5bn) on combined books >E130bn; Portugal raised E4bn of 10-Yr PGB on books >E30bn. In auctions, Germany allotted E3.3bn of Bobl and UK GBP5bln total of Gilts.

- In data, Spain March services PMI beat expectations, while Italy missed; both <50.

- Afternoon attention was on dual press conferences by the EU and UK vaccine regulators on the AstraZeneca jab's potential links with blood clotting. EMA noting that vaccine's clots as a rare side effect, but otherwise no action taken, EU ministers to discuss at 1700BST. UK will offer under-30s an alternative (eg Moderna) but not expected to slow overall vaccine rollout.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.2bps at -0.703%, 5-Yr is down 0.8bps at -0.657%, 10-Yr is down 0.8bps at -0.324%, and 30-Yr is down 0.4bps at 0.231%.

- UK: The 2-Yr yield is down 1.1bps at 0.064%, 5-Yr is down 1.5bps at 0.358%, 10-Yr is down 2.4bps at 0.773%, and 30-Yr is down 2.2bps at 1.315%.

- Italian BTP spread up 0.8bps at 101.7bps/ Spanish spread up 0.5bps at 66.6bps

OPTIONS/EUROPE SUMMARY: Mostly Downside Buying

Wednesday's options flow included:

- RXK1 171/170ps, bought for 18 in 3.25k

- RXK1 168.5p, bought for 3 in 5k

- OEM1 134.75/134.50ps 1x1.5, bought for 1.25 in 5k and 1.5 in 5k

- OEM1 135.75c, bought for 11 in 2.5k

- ERZ2 100.50p, bought for 11.5 in 3k (ref 100.525)

- 2RM1 100.50/100.37/100.25p fly vs 0RM1 100.50p, bought the fly for 1.5 in 1.5k

- 0LU1 99.75^, sold at 17.5 in 1.45k

- 3LU1 / 3LM1 98.875/98.625 1x1.5 put spread (v 99.095 on 3LU1) bought for 1 in 13.5k

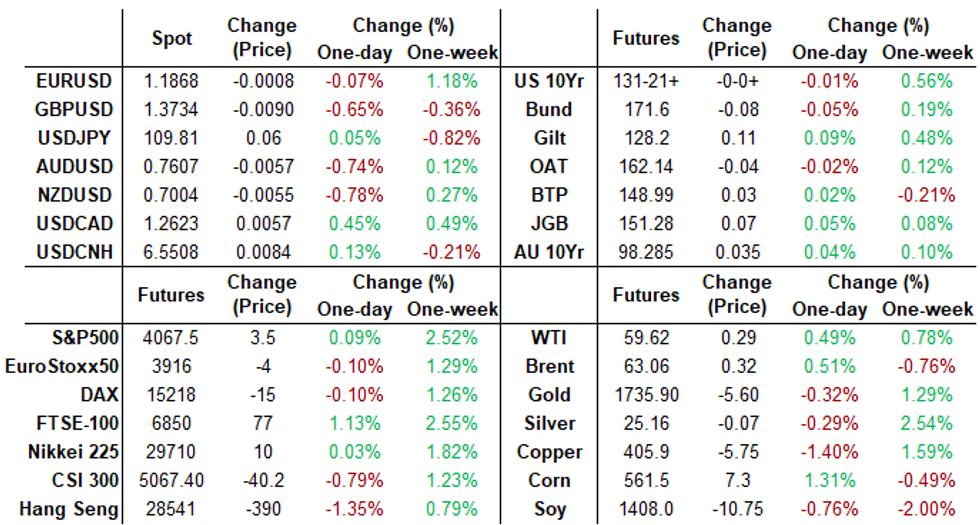

FOREX: Sterling Softens as Key Vaccine Restricted for Under-30s

- Speculation swirled ahead of a press conference from the UK's medicines regulator, which moved to restrict the distribution of the most widely used vaccine for those aged below 30. While the vaccine committee stressed that there was little risk to the overall vaccine plan, markets remain concerned that the switch could result in a delay to the planned easing of virus restrictions.

- This dampened sentiment hit GBP, which fell against all others in G10, and extended the pullback from the midweek highs to over 150 pips. Next support for GBP/USD undercuts at the 100-dma at 1.3678.

- Further demonstrating the risk-off theme were slips in antipodean currencies, with AUD and NZD falling alongside GBP. Similarly, the CHF and JPY were among the session's best performers.

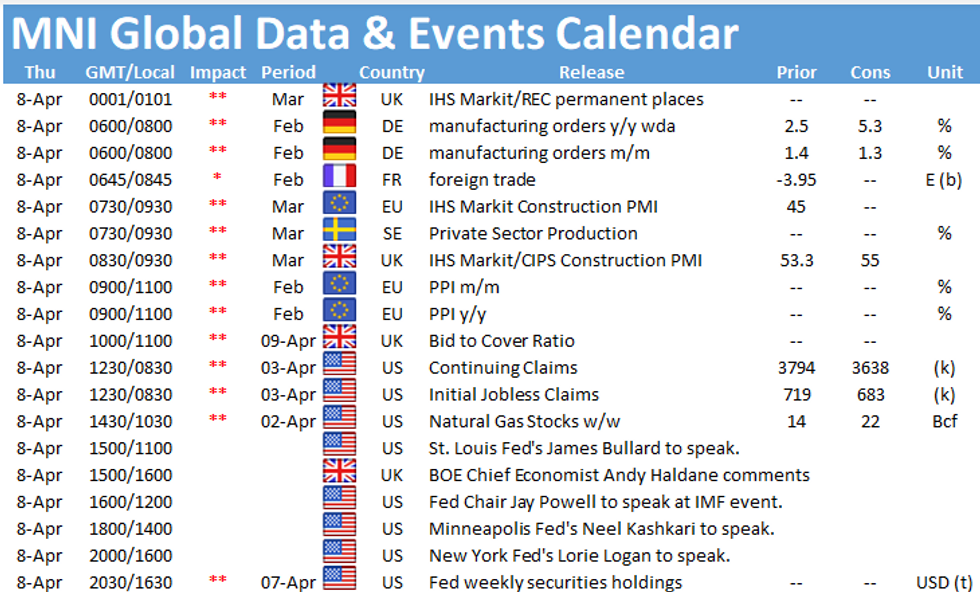

- Focus Thursday turns to Japanese trade balance and US weekly jobless claims data. Central bank speakers include Fed's Powell, Kashkari & Bullard.

FX OPTIONS: Expiries for Apr08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1690-1.1700(E2.1bln), $1.1720-25(E1.85bln), $1.1750-55(E1.1bln), $1.1800(E1.94bln, E1.76bln of EUR puts), $1.1840-50(E1.3bln), $1.1885-00(E3.2bln), $1.1910(E903mln)

- USD/JPY: Y108.45-55($1.3bln), Y108.60-70($1.5bln), Y108.80-86($1.2bln), Y109.00-05($561mln), Y109.50($742mln), Y109.75($810mln), Y110.15-20($535mln)

- EUR/GBP: Gbp0.8550(E931mln)

- AUD/USD: $0.7665-80(A$964mln), $0.7700-20(A$1.6bln)

PIPELINE: High-Grade Issuance Review

$12.7B to price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 04/07 $5B *Asia Development Bank (ADB) 5Y +2

- 04/07 $3B #Ontario 5Y +11

- 04/07 $1.5B #United Overseas Bank (UOB) $750M 5Y +48, $750M 10.5NC5.5 +123

- 04/07 $850M *EBRD 5Y FRN SOFR+19

- 04/07 $800M #Pacific Life Global 5Y +53

- 04/07 $550M #Northern Natural Gas +30Y +110

- 04/07 $500M #Brookfield Finance 10Y +107

- 04/07 $500M #Jabil 5Y +85

- Later in week:

- 04/08 $3.5B Organon $2B 7NC3, $1.5B 10NC

- 04/08 $1B Canadian Pension Plan (CPPIB) WNG 3.5Y +2

- 04/08 $500M AIIB WNG 5Y FRN SOFR+24a

- 04/08 $Benchmark KFW 2Y +0

- 04/08 $Benchmark Japan Bank of Int Cooperation (JBIC) WNG 3Y +9a, 10Y +26a

EQUITIES: Stocks Oscillate Either Side of Unchanged

- A relatively uneventful session for US stock markets as the S&P 500 traded either side of unchanged for much of the day. In futures space, the e-mini S&P managed to hold the bulk of the week's gains, raising the likelihood of a test on all time highs on any break higher.

- Communication services remain firm and were the strongest performing sector Wednesday. Energy and tech also traded well, but only posted marginal gains. Materials and industrials sectors countered, slipping to the bottom of the US table.

- In Europe, UK's FTSE-100 outperformed as GBP softened, while all other continental bourses were in retreat. Spain's IBEX-35 was the laggard, dropping 0.4% at the close.

COMMODITIES: Copper Falls 1.5% On Dampened Demand Outlook

- Copper extended its retreat from Monday's spike, falling 1.5% on Wednesday, amid concerns over Chinese demand and further signs of adequate supply.

- Rhetoric from Chinese government officials on the need to avoid asset bubbles is tempering investor enthusiasm for raw materials despite a broadly positive economic outlook. Additionally, Chile's central bank reported copper exports reached an eight-year high in March, further easing fears surrounding supply constraints.

- Precious metals had a very subdued session, broadly unchanged in line with the US dollar ahead of the release of the FOMC minutes.

- Crude futures dipped 2% before rebounding and posting marginal gains on Wednesday up roughly 0.4%. This price action continued the largely rangebound trade that has seen WTI crude close each of the past nine sessions less than $2 above or below $60 as investors continue to assess the multitude of counteracting factors in play.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok