Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Wk's Bond Rally Pace Slowing; Weekly Claims Declines

Bond yields continued to fall Thursday, but the week's pace has slowed, rates holding to a narrower range all session. Knock-on bid from EGBs continued to be a factor cited by sell-side desks, curve steepener unwinds running their course.- Tsys trimmed gains after lower than estimated weekly claims of 293k -- lowest since pre-pandemic, tame PPI at .5 and .2 core. Fast two-way immediately after release seeing better selling in 10s-30s from prop and real$ accts. Yield curves bouncing after week's broad flattening, finished the session mixed: 5s30s climbed back over 100.0 briefly, receded into the second half: +1.44 at 96.99.

- Surprise $5B 2pt issuance from Morgan Stanley weighed on 5s-10s on rate-lock hedging. More banks sure to follow as they exit earnings blackout. May help push total October issuance estimate over $125B.

- Fed Speak: "Supply chain constraints are clearly going to last longer than they hoped—well into the second half of next year in many sectors," said Jeffrey Lacker, former president of the Richmond Fed, noting that base year effects have already petered out. Six-month inflation is now running at a 7.2% annual rate, Lacker said. "As long as it's just supply chains, they can hold on a little longer. But the issues are pass-through and expectations, and on those fronts the data continues to erode."

- After the close the 2-Yr yield is down 1bps at 0.3481%, 5-Yr is down 2.4bps at 1.0452%, 10-Yr is down 2.3bps at 1.5142%, and 30-Yr is down 1.2bps at 2.0167%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00163 at 0.07200% (-0.00063/wk)

- 1 Month -0.00437 to 0.08588% (+0.00225/wk)

- 3 Month -0.00150 to 0.12225% (+0.00112/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00250 to 0.15925% (+0.00275/wk)

- 1 Year +0.00688 to 0.27263% (+0.02563/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $73B

- Daily Overnight Bank Funding Rate: 0.07% volume: $270B

- Secured Overnight Financing Rate (SOFR): 0.05%, $907B

- Broad General Collateral Rate (BGCR): 0.05%, $372B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $352B

- (rate, volume levels reflect prior session)

- Tsys 22.5Y-30Y, $2.001B accepted vs. $4.827B submission

- Next scheduled purchases, note Tuesday's double operation

- Fri 10/15 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

- Mon 10/18 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Tue 10/19 1010-1030ET: 2.25Y-4.5Y, appr $8.425B

- Tue 10/19 1100-1120ET: TIPS 1Y-7.5Y, appr $2.025B

- Wed 10/20 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Thu 10/21 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Fri 10/22 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

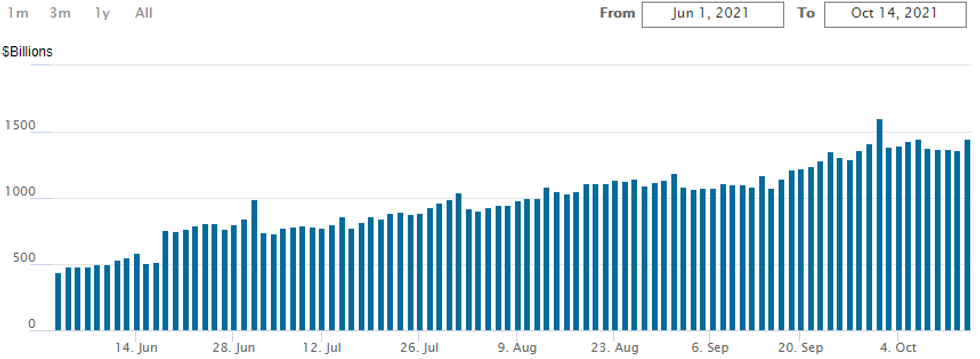

FED Reverse Repo Operation Usage Climbing

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,445.660B from 83 counterparties vs. $1.364.701B on Wednesday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options- Block, 10,000 short Dec 99.12/99.37 put spds, 5.0

- +20,000 Blue Dec 98.00/98.37 put spds, 11.0 vs. 98.36/0.36%

- +3,000 Jun 99.81/99.87 1x2 call spds, 1

- +7,500 short Dec 99.50/99.62 call spds, 1.5, still bid

- +3,000 Jun 99.81/99.87 1x2 call spds, 1

- -2,500 Green Dec 98.37/98.62/98.75/99.00 put condors, 12.0

- -2,500 Green Dec 98.37/98.62/98.75/99.00 put condors, 12.0

- -10,000 short Dec 99.50/99.62 put spds vs. Blue Dec 98.25/98.37 put spds, 5.75 net cr/conditional curve steepener

- 10,000 short Dec 99.25 puts, 2.5, 29.5k total on day

- +8,000 long Red Mar'23 99.25 straddles, 45.5 (45.0 set'), 99.23 ref

- 8,000 Blue Dec 97.75 puts, 1.0

- +5,000 Green Feb 97.62/98.00 3x2 put spds, 3.0

- Overnight trade

- +30,000 short Dec 99.50/99.62 1x2 call spds, 1.0, 99.37 ref

- 4,500 short Dec 99.25/99.37/99.43 2x1x1 put tree

- Block, 22,267 Blue Dec 98.37 puts, 13.5

- 16,000 Blue Oct 81/83 put spds

- 11,000 Green Oct 98.50/98.75 put spds

- 7,500 short Dec 99.37 straddles

- 7,000 short Dec 99.37/99.43/99.50 call flys

- 3,200 short Jun 98.37/98.62 put spds

- 3,000 Green Dec 98.43/98.62 put spds vs.

- 2,000 Blue Dec 98.12/98.25/98.50 put flys

- 2,500 Green Dec 98.87/99.00 put spds vs. 99.25/99.37 call spd

- 1,250 short Mar 99.00/99.25/99.37/99.50 put condors

- +14,000 TYX 131/TYZ 130 put diagonal calendar spd, 8 net/Dec over

- 5,000 FVX 121.75 puts

- +6,000 TYX 130.5/130.75 put spds, 2 vs. 131-18.5/0.06%

- Overnight trade

- 6,000 TYX 130.5/130.75 put spds, 3

- +7,500 TYZ 131/131.5 put spds, 13

- +5,000 FVZ 121.5/123 call over risk reversals, 1 vs. 122-12/0.48%

- +4,000 FVZ 122.75 calls, 13-15

EGBs-GILTS CASH CLOSE: Gilts Continue To Drive Bullish Retracement

European FI staged more impressive gains Thursday as yields retreat from the recent highs, with the core space seeing short-end GIlts and 10Y Bunds outperforming.

- The gains came against a backdrop of stronger equities and (somewhat counterintuitively given their role in the recent inflation narrative) commodity prices.

- The risk-on atmosphere helped periphery EGB spreads tighten (though Greece widened).

- Hard to pin the move on any particular factor, though it seems the hawkish BoE / inflation narrative weakening Gilts of late may have gone too far and the move is now unwinding. The violence of the UK move has arguably helped catalyse the Bund rally.

- BoE's Mann noted she was willing to hold fire on rate hikes, helping 2Y Gilts continue their rally later in the session.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

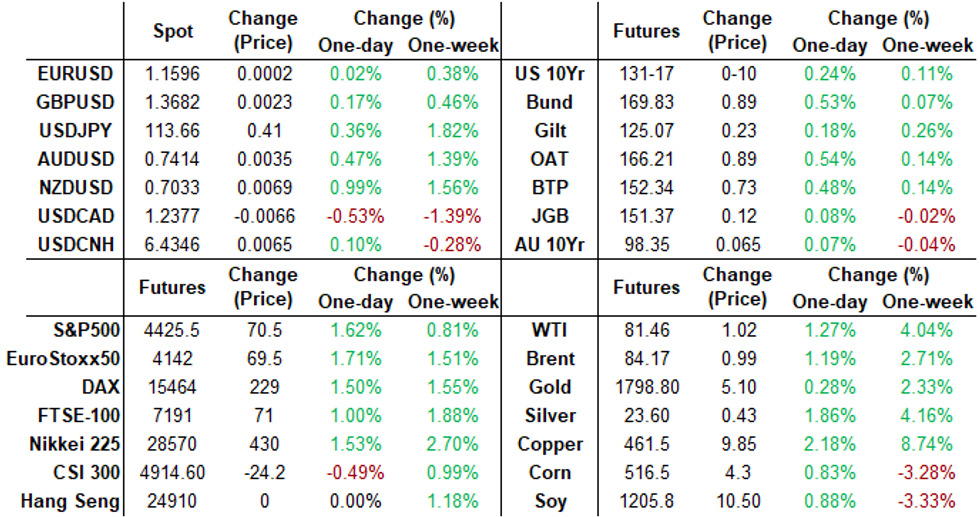

- Germany: The 2-Yr yield is down 2.3bps at -0.692%, 5-Yr is down 5.8bps at -0.537%, 10-Yr is down 6.4bps at -0.191%, and 30-Yr is down 6.1bps at 0.238%.

- UK: The 2-Yr yield is down 6.2bps at 0.514%, 5-Yr is down 6.4bps at 0.699%, 10-Yr is down 4.7bps at 1.042%, and 30-Yr is down 5.4bps at 1.289%.

- Italian BTP spread down 0.7bps at 102.4bps / Greek up 3.5bps at 109.1bps

EGB Options: Bund Short Cover; Large Sterling Put Structures

Thursday's European rates / bond options flow included:

- DUZ1 112.20/30/40c fly, bought for 2 in 4k

- OEZ1 135.25/135.50/135.75 call ladder bought for 1.5 in 4k

- RXX1 169put, bought for 27.5 in 5k (short cover)

- RXX1 168.5p, bought for 25.5 up to 29 in 7k (some suggest a short cover)

- 0RF2 100.25/100ps 1x2, bought for 2.25 in 2k

- 0LZ1 99.00/98.87/98.75p fly sold at 1.5 in ~26.5k (said to be rolling downstrikes)

- 2LZ1 98.88/98.75/98.62p fly, sold at 1.5 in ~48k

- 0LZ1 99.00/98.87 ps sold at 5.25 in ~30k

FOREX: JPY Resumes Slide, Testing Week's Lows vs. USD

- The greenback traded poorly Thursday, falling against most others in G10 as a lower, flatter yield curve drained recent greenback strength. The USD index showed below the 94.00 handle, but managed to recoup some of the lost ground just after the London close.

- JPY resumed recent weakness, underperforming all others as both equity markets and treasuries surged. USD/JPY traded either side of the 113.50 level, not quite touching the week's cycle highs of 113.80, but clearly signalling that another test of the highs is within range.

- Growth proxies and commodity-tied currencies extended Wednesday's outperformance, with NZD and CAD trading solidly throughout. NZD/USD traded at a new October high, topping the 50- and 100-dmas in the process at 0.7003 and 0.7026 respectively.

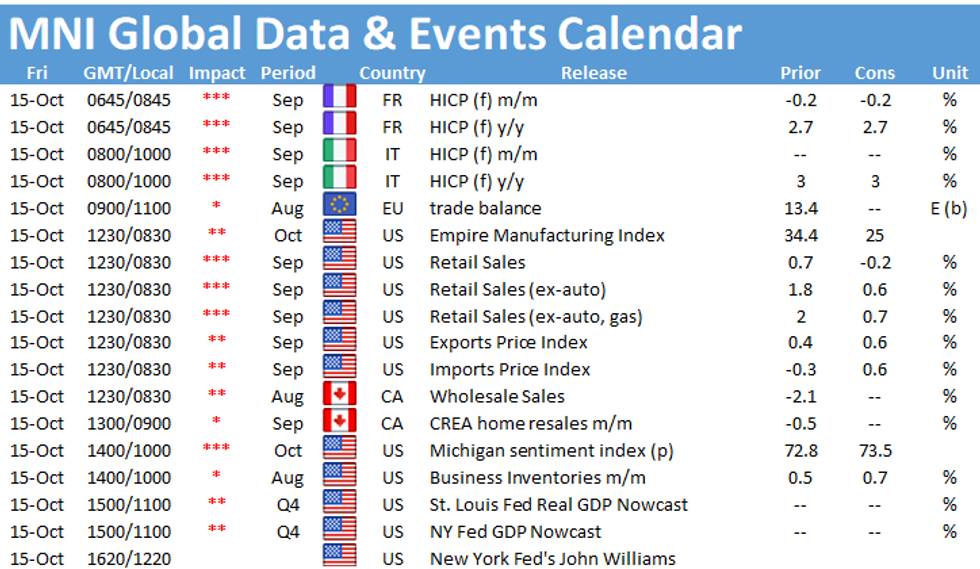

- US retail sales data for September crosses on Friday, with import/export price numbers also due. UMich data is prelim for October, so could also draw focus. Fed's Bullard, Harker and Williams are also due to speak.

FX: Expiries for Oct15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550-65(E1.3bln), $1.1600(E670mln), $1.1650(E738mln)

- USD/JPY: Y111.90-00($788mln), Y112.50-65($1.0bln), Y113.00-15($1.4bln), Y113.90-00($585mln)

- USD/CAD: C$1.2360-75($630mln), C$1.2480-00($1.9bln)

- USD/CNY: Cny6.40($891mln), Cny6.45($770mln)

PIPELINE: Surprise $5B Morgan Stanley 2Pt Post-Earnings

More banks sure to follow as they exit earnings blackout. May help push total October issuance estimate over $125B.- Date $MM Issuer (Priced *, Launch #

- 10/14 $5B #Morgan Stanley $2.5B each: 4NC3 +57, 11NC10 +100

- 10/14 $1B *Province of Manitoba 7Y global +20

- 10/14 $1B #Republic of Columbia 5.2% 05/15/49 tap 5.125%

EQUITIES: Wall Street Surges as Banks Crush Earnings Forecast

- Equity markets across the US rallied Thursday, with bank earnings being received positively across the Street. The likes of Bank of America and Morgan Stanley traded solidly after their Q3 reports, which painted a solid picture of internal financials as well as consumer health.

- Technology firms and material also traded solidly. The former benefited from a sharp downtick in Treasury yields, with the 10-yr yield dropping for a third consecutive session to test the 1.50% level despite trading above 1.60% at the beginning of the week.

- Technically, the e-mini S&P is now fast approaching the 50-dma at 4430.75, a break above which would be a solid bullish signal. A close above here opens gains toward 4472.00 - the late September high - a level which would open alltime highs printed a month and a half ago.

- Earnings season continues Friday, with Goldman Sachs, Charles Schwab and PNC Financial on the docket for Friday.

COMMODITIES: DoE Inventories Dent Crude Rally, But Outlook Remains Bullish

- WTI crude futures ticked lower on the release of the weekly DoE crude oil inventories data (one day delayed due to the Columbus Day holidays) with markets focusing on the considerably larger-than-expected build in headline crude stockpiles (+6.1mln bbls vs. Exp. +521k). This pressured front-month WTI futures to lows of $80.38, although losses were limited by the countering draw in gasoline inventories, at -2mln bbls vs. Exp. build of +947k.

- Despite the pullback in prices, the outlook remains bullish and the contract is holding onto recent gains. Monday's fresh high confirmed an extension of the current bullish price sequence of higher highs and higher lows, reinforcing the uptrend. Note that the $80.00 psychological hurdle has also been cleared. The focus is on $82.89, a Fibonacci projection.

- Gold held the bulk of the Wednesday rally, and has breached the 50-day EMA and resistance at $1787.4, the Sep 22 high. The resumption of strength reinforces short-term bullish conditions and the bullish engulfing candle pattern that signalled a potential reversal on Sep 3. The focus is on $1808.7 next, Sep 14 high. Initial firm support is at $1746.0, Oct 6 low. A break is required to undermine a bullish tone.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok