Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Russia War Keeps Mkts on Edge, Into Weekend; Strong Jobs Data

After initial two-way trade US Tsy futures broke narrow upside range after Feb employment data showed job gains +678k vs. +415k est, AHE declines MoM from 0.61% to 0.03.

- Overall data appears "mildly less inflationary, at least from the supply side" one desk commented. Decent data but markets remained on edge as Russia war in Ukraine entered day nine.

- Equities still trading weaker after FI close, SPX eminis off late morning lows (ESH2 4282.50L) to near middle of the range at 4307.5 at the moment -- still above first technical support of 4227.50/4101.75 Low Feb 25 / Low Feb 24 and a bear trigger. Markets remain on edge going into the weekend.

- Late session risk aversion: Tsys turn higher, additional selling in stocks after headlines noted access to Twitter and Facebook blocked in Russia -- social media outlets a non-state media source of news for Russians. WTI spiked to session highs of $115.36 in late trade as WH spokesperson said banning Russia oil imports had been discussed.

- While FI markets traded strong all day -- short end remained under heavy pressure: lead quarterly Eurodlr futures made new low for yr at 99.15 (-0.140), well past prior low of 99.205 from Feb 10 as 50bp liftoff pricing gains momentum -- 25bp hike on March 16 a foregone conclusion after Fed Chairman Powell sees as appropriate (Thu's Senate testimony).

- The 2-Yr yield is down 4bps at 1.4899%, 5-Yr is down 9.5bps at 1.6372%, 10-Yr is down 11bps at 1.7307%, and 30-Yr is down 6.7bps at 2.1533%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00086 at 0.07814% (+0.00100/wk)

- 1 Month +0.02100 to 0.31014% (+0.07957/wk)

- 3 Month +0.02700 to 0.61014% (+0.08714/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.04943 to 0.93943% (+0.11072/wk)

- 1 Year +0.02100 to 1.35286% (+0.02215/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $68B

- Daily Overnight Bank Funding Rate: 0.07% volume: $253B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $1.001T

- Broad General Collateral Rate (BGCR): 0.05%, $367B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $354B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- Next scheduled purchases

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

FED Reverse Repo Operation, New Low for Year

NY Federal Reserve/MNI

NY Fed reverse repo usage falls to $1,483.061B w/ 78 counterparties -- new low for the year vs. $1,533.992B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

US Treasury/Eurodollar Option RoundupOverall option volumes rather muted on the day -- even as lead quarterly extended new low for the year (EDH2 -0.130 to 99.15) -- perhaps a little too aggressively pricing in chance of 50bp liftoff at March 16 FOMC.

- Carry-over from Thu and overnight trade in lead quarterly Mar Eurodlr futures/3M LIBOR jump (+0.02700 to 0.61014% (+0.08714/wk) as traders look for extension of FRA/OIS widening to June -- possible link to increased funding concerns tied to Russia risk exposure for global banks.

- Meanwhile, Chicago Fed Pres Evans said on CNBC this morning -- the strong jobs data "DOESN'T REALLY CHANGE ANYTHING THAT FED CHAIR POWELL IS POSITIONING FOR" -- where Powell said 25bp hike appeared appropriate at Thu's Senate testimony. Fed enters media blackout at midnight Friday through March 17, day after the FOMC announcement.

- Salient Eurodollar option trade included scale buyer 10,000 Green Jun 97.50/97.75 put spds and over20,000 Mar 99.06 puts, 4.0.

- Treasury options saw scale buyer over 32,000 TYJ 126 puts on wide range of prices: 12-24.

- Block, 5,000 SFRZ2 98.18/98.43 put spds 10.0 vs. 98.475/0.10%

- +4,000 Apr 98.56/98/75 2x1 put spds, 6.0 2-legs over

- +10,000 short Sep 98.50/99.00/99.50 call flys, 6.0

- -5,000 Blue Jun 97.75/98.00 put spds, 7.5

- +5,000 Jun 98.62 puts, 18.0 vs. 98.79/0.40%

- Overnight trade

- 12,000 Mar 99.06 puts, 4.0

- Block, 10,000 Green Dec 97.00/97.50 put spd 3.0 over May 98.62/98.81 put spd

- 7,500 Jun 97.75/98.25 put spds

- 4,000 Jul 97.25/97.75 put spds

- 3,000 Dec 98.25/Mar 99.12 put calendar spds

- 3,000 Dec 98.75/99.00/98.00/98.25 put condors

- 4,000 Green Mar 99.00/99.12/99.25 put flys

- 3,000 Blue Apr 97.87 puts, 10.5

- 7,000 TYK 125 puts, 20-22

- +10,000 TYJ 126 puts, 16 total volume over 32k on wide range of prices: 12-24

- 5,000 TYM 131.5 calls, 40

- 4,000 TYJ 125/126 put spds, 9

- 2,300 FVJ 116.25/117.25 put spds

- Overnight trade

- 1,500 USK 147/149/151/153 put condors

- 4,000 FVM 116.5/117 put spds

- 3,800 TYM 132 calls, 34

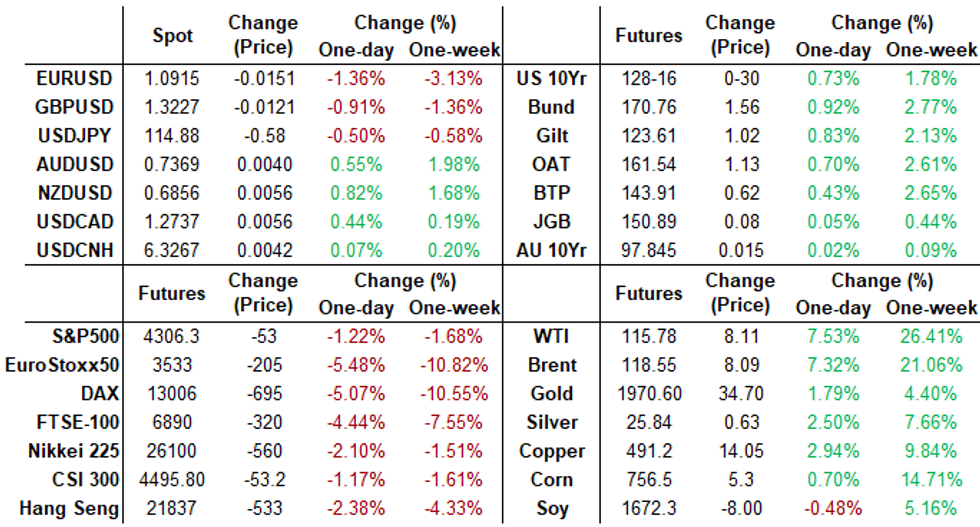

FOREX: Souring Sentiment Prompts Flight To Quality, Euro Crosses Extend Declines

- A deterioration in risk-sentiment surrounding the Ukraine war was characterised by renewed weakness in equities and further surges in the commodity complex, especially evident in crude futures, rising another 6%. In turn, this saw further significant pressure on Euro crosses as well as lending support to the greenback approaching the weekend.

- EURUSD trades 1.2% weaker as of writing and has made notable technical progress to the downside throughout the week. Moving average studies point south and the bearish price sequence of lower lows and lower highs remains intact. 1.1000 and 1.0976, a Fibonacci projection have both been cleared with the move lower falling just shy of the 1.0871 level, the low seen on May 25, 2020.

- Continued buoyancy of the commodity complex as well as geographical dynamics made Euro crosses an even more attractive short. EURJPY (-1.85%) EURAUD (-1.89%) and EURNZD (-2.19%) all cratered throughout the session, with rising tensions in Ukraine showing very few signs of this pressure on Euro crosses abating in the short-term.

- Overall, the greenback was boosted as market participants sought a flight to quality. The dollar index rose 0.75% to extend above the 98.00 mark, edging towards the best levels of Q2 2020. The dollar strength finally put LATAM FX on the backfoot with USDMXN rising to the best levels of the year above 20.90. Additionally, the euro weakness significantly weighed on emerging market currencies in the CEEMEA region, with HUF and PLN considerably lower on Friday and prompting the Polish central bank to intervene to support the Zloty.

- A light data calendar to kick off next week with Chinese trade balance figures and German factory orders. Naturally, developments over the weekend in Ukraine will determine the direction and volatility for currencies at the Wellington open.

FX: Expiries for Mar07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1085-00(E525mln), $1.1165-75(E1.2bln)

- USD/JPY: Y114.20-30($871mln), Y115.00-05($717mln)

- EUR/GBP: Gbp0.8230-35(E549mln), Gbp0.8510-15(E1.2bln)

- USD/CNY: Cny6.3000($699mln), Cny6.4000($783mln)

EQUITIES: Late Equity Roundup, Weaker, Inside Range Session

Equities still trading weaker heading into late FI trade, SPX eminis off late morning lows (ESH2 4282.50L) to near middle of the range at 4307.5 at the moment -- still above first technical support of 4227.50/4101.75 Low Feb 25 / Low Feb 24 and a bear trigger. Markets remain on edge going into the weekend.

- Late session risk aversion: Tsys turn higher, additional selling in stocks after headlines noted access to Twitter being blocked in Russia after Facebook blocked earlier -- social media outlets a non-state media source of news for Russians.

- Likely a stronger trigger: White House press secretary Jen Psaki said the US is considering banning oil imports from Russia. Crude prices certainly spiked higher on that, WTI surged to new high of 115.7.

- SPX leading/lagging sectors: Energy sector continues to outperform +2.05%, Utilities bounced to +1.71%%; Financial sector extends underperformance -3.04%, Information Technology -2.49%, Consumer discretionary -2.17%.

- Dow leaders: Chevron (CVX) has pared earlier gains on rating upgrade and surge in crude, paper squaring ahead the weekend. Boeing (BA) leads laggers now with financials close second: Goldman Sachs (GS) -8.87to 324.55, American Express (AXP) -8.75 to 171.15.

- RES 4: 4671.75 High Jan 18

- RES 3: 4586.00 High Feb 2 and a key resistance

- RES 2: 4473.77 50-day EMA

- RES 1: 4418.75 High MAr 3

- PRICE: 4305.00 @ 20:00 GMT Mar 4

- SUP 1: 4227.50/4101.75 Low Feb 25 / Low Feb 24 and a bear trigger

- SUP 2: 4055.60 Low May 19 2021 (cont)

- SUP 3: 4029.25 Low May 13 2021 (cont)

- SUP 4: 3990.50 0.764 proj of the Jan 4 - 24 - Feb 2 price swing

COMMODITIES: Oil Sees Yet Further Boost As US Eyes Russian Import Ban

- Crude oil prices rise sharply as the White House considers the banning of Russian oil imports, more than reversing an earlier dip on an Iranian deal sounding imminent.

- This further adds to growing Russia-Ukraine fallout fears, kickstarted by damage sustained to a nuclear power plant in fighting overnight.

- WTI is +7.0% at $115.2, approaching yesterday’s high of $116.57 which if cleared could open the psychological $120. In signs of how tight supply is, the US oil rig count surprisingly fell in latest weekly data despite such high prices.

- Brent is +6.5% at $117.66, with next resistance the psychological $120.

- Gold continues to flourish with this backdrop, rising +1.7% at $1968.7. Having cleared the bull channel top, it next eyes $1974.3 from the start of the Russian invasion after which it opens $1980.8 (2 proj of the Dec 15 – Jan 28-28 price swing).

- European natural gas meanwhile rises another 20% on the day, hitting record highs on extreme volatility in fears of Russia cutting off supply.

- Weekly gains: WTI +26%, Brent +20%, Gold +4.2%, European Nat Gas +104%

Monday-Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/03/2022 | 0645/0745 | ** |  | CH | unemployment |

| 07/03/2022 | 0700/0800 | ** |  | DE | manufacturing orders |

| 07/03/2022 | 1630/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 07/03/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 07/03/2022 | 2000/1500 | * | | US | Consumer Credit |

| 08/03/2022 | 0001/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 08/03/2022 | 0700/0800 | ** | | DE | industrial production |

| 08/03/2022 | 0800/0900 | ** |  | ES | industrial production |

| 08/03/2022 | 0900/1000 | * |  | IT | retail sales |

| 08/03/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 08/03/2022 | 1000/1100 | *** |  | EU | GDP (2nd est.) |

| 08/03/2022 | 1100/0600 | ** | | US | NFIB Small Business Optimism Index |

| 08/03/2022 | 1330/0830 | ** | | US | trade balance |

| 08/03/2022 | 1330/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 08/03/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 08/03/2022 | 1500/1000 | ** | | US | wholesale trade |

| 08/03/2022 | 1500/1000 | ** | | US | IBD/TIPP Optimism Index |

| 08/03/2022 | 1800/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.