Real-time Actionable Insight

Get the latest on Central Bank Policy and FX & FI Markets to help inform both your strategic and tactical decision-making.

Free Access

US TSYS: Core CPI Jumps 0.6%, Underscores Near-Term Rate Hikes

Tsys futures finish mostly higher, well off initial post data lows curves bull flattened (2s10s -9.665 at 27.771) as bonds discounted the April CPI inflation data: up 0.3% m/m in April and 8.3% y/y, Core CPI jumped 0.6% m/m and 6.2% y/y, a slowing from 6.5% last month.

- Short end weaker - anchored as additional three 50bp rate hikes gets baked in (chance of 75bp hike in near term back in realm of possibility. Nevertheless, analysts anticipate inflation softening in the coming months.

- Tsy futures holding near session highs but scaling back support slightly after $36B 10Y note auction (91282CEP2) tails: 2.943% high yield vs. 2.925% WI; 2.49x bid-to-cover off last month's 2.43x.

- Indirect take-up climbs to 70.30% vs. last month's 64.33% high; direct bidder take-up at 18.21 from 17.02%, while primary dealer take-up falls to 11.49% vs. 18.66%.

- Meanwhile, the U.S. Treasury said it posted a record budget surplus of USD308 billion in April, fueled by record tax receipts and lower outlays, versus a budget deficit of USD226 billion in the same month one year earlier.

- The fiscal year-to-date budget deficit was USD360 billion, following a record USD1.9 trillion deficit in the same period a year earlier, the Treasury said.

- Thursday focus on PPI Final Demand MoM (1.4% prior, 0.5% est); YoY (11.2%, 10.7%), weekly claims (192k) and $22B 30Y Bond auction (912810TG3)

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00229 to 0.82600% (+0.00743/wk)

- 1M +0.01100 to 0.85414% (+0.01200/wk)

- 3M +0.02200 to 1.42186% (+0.02000/wk) * / **

- 6M +0.03071 to 1.96271% (-0.00186/wk)

- 12M +0.02842 to 2.61671% (-0.07800/wk)

- * Record Low 0.11413% on 9/12/21; ** New 2Y high: 1.42186% on 5/11/22

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.83% volume: $72B

- Daily Overnight Bank Funding Rate: 0.82% volume: $253B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.78%, $914B

- Broad General Collateral Rate (BGCR): 0.80%, $348B

- Tri-Party General Collateral Rate (TGCR): 0.80%, $338B

- (rate, volume levels reflect prior session)

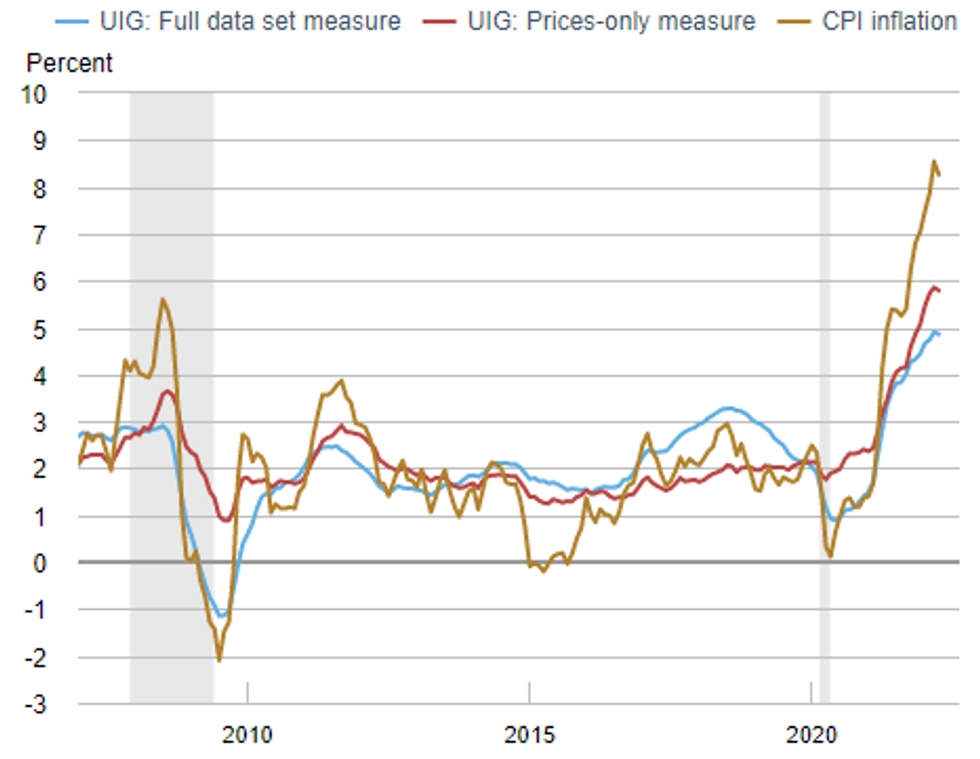

NY Fed Underlying Inflation Gauge

NY Federal Reserve

- The UIG "full data set" measure for April is currently estimated at 4.9%, similar to the previous month.

- The "prices-only" measure for April is currently estimated at 5.8%, a 0.1 percentage point decrease from the current estimate for the previous month.

- The twelve-month change in the April CPI was +8.3%, a 0.2 percentage point decrease from the previous month.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Tsys futures rebounding as bonds appear to be discounting the inflation data, short end anchored as additional three 50bp rate hikes gets baked in. Nevertheless, analysts anticipate inflation softening in the coming months.Yield curves bear - then bull-flattened on the day amid surge in rate hike hedging via various outright put buying and spread trade.

SOFR Options:

- +5,000 SFRU2 97.00/97.25 put spds, 3.0 ref 97.68

- +3,000 SFRU2 97.37/97.50/97.62 put flys, 1.75 ref 97.675

- +5,000 Jun 96.00/96.25/96.50 put flys, 2.25

- Block, 6,000 Green Sep 96.25/96.62 3x2 put spds, 7 net

- Bloc, 10,000 Jun 98.12 straddles, 11.0 vs. 98.155/0.18%

- Block, +10,000 short Dec 98.50 puts, 12.5 vs. 96.66/0.16%

- Overnight trade

- 4,800 short May 96.31/96.44 put spds ref 96.645

- +1,000 short May 96.37/96.50 3x2 put spds, 3.0 re 96.645

- +12,500 TYM 119 calls, 32-34, total volume over 25k

- Block, 10,000 TYM 115.5/117.5 3x2 put spds, 26 net vs. 4,200 TYM2 at 118-18

- Over +18,000 wk2 TY 118.5/119 put spds, 7 vs. 119-09.5/0.20%

- +6,500 wk2 TY 119.75 calls, 13 ref: 119-06.5

- +5,500 TYM 121 calls, 6 vs 118-29/0.06%

- 4,000 FVM 114 calls

EGBs-GILTS CASH CLOSE: Post-US CPI Reversal

European bond yields fully reversed a sharp rise after stronger-than-expected US inflation data over the course of Wednesday afternoon. Short end yields reversed lower as Fed hawkishness post-CPI was second-guessed. This allowed the UK and German curves to re-steepen after modest flattening earlier in the session.

- Periphery spreads fell sharply, mirroring risk-on moves in equities.

- Little impact from ECB headlines, as markets had already priced the news in: a BBG sources piece reporting ECB officials are increasingly seeing rates rising above zero this year, Pres Lagarde's comment that hikes could come "a few weeks" after net asset purchases in Q3 conclude left the door open for a July rate hike

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 2.2bps at 0.139%, 5-Yr is down 3.1bps at 0.659%, 10-Yr is down 1.5bps at 0.985%, and 30-Yr is down 0.2bps at 1.138%.

- UK: The 2-Yr yield is down 4.2bps at 1.286%, 5-Yr is down 3.3bps at 1.45%, 10-Yr is down 2.4bps at 1.824%, and 30-Yr is up 0.9bps at 2.064%.

- Italian BTP spread down 9.2bps at 190.9bps / Spanish down 6bps at 104.2bps

EGB Options: Bobl Put Condor Unwind, Mixed Rates Trade

Wednesday's Europe rates / bond options flow included:

- OEM2 127.00/126.25 ps, sold at 32.25 in 11k (unwinding the top leg of a put condor)

- ERU2 99.25/99.00ps, bought for 1 in 5k

- SFIU2 98.40/98.50/98.60 call fly bought for 1.25 in 3.5k

FOREX: Greenback Sustains Losses Despite Higher CPI

- The greenback headed into the April CPI release as the worst performing currency in G10, as markets positioned for a soft reading. This quickly reversed course following the release, with the greenback rallying in tandem with US yields while equities fell. Core CPI was 0.2ppts ahead of expectations, driven by services inflation. This helped drive rate expectations higher and prompted a wave of risk off.

- EUR/USD traded through overnight lows of 1.0526 to narrow in on the 1.0500 handle, before the price action partially reversed into the close - with markets adopting the view that the bar to larger hikes from the Fed remains high. For EUR/USD, however, the trend remains lower. Weakness through 1.0500 would open the YTD and cycle lows of 1.0472 next.

- Elsewhere, EUR/GBP traded well, with the cross topping 0.8550 as the European Union warned that they would suspend the post-Brexit trade deal should the UK move to unilaterally revoke the Northern Ireland protocol. The renewed concern surrounding the Brexit Withdrawal Agreement pushed GBP to be the poorest performer in G10 Wednesday.

- UK preliminary GDP data crosses Thursday, with markets expecting 1.0% growth on the quarter and 8.9% on the year. US PPI data is also due, in which markets will be watching for any follow through of inflationary pressure after Wednesday's above-forecast CPI. ECB's de Cos and Makhlouf are also due to speak.

FX: Expiries for May12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0400(E507mln), $1.0600(E1.3bln), $1.0625(E793mln), $1.0675-85(E1.1bln)

- GBP/USD: $1.2400(Gbp690mln)

- EUR/GBP: Gbp0.8580-00(E503mln)

Late Equity Roundup: Second Half Reversal, Tech Sees Red

Stocks having a rough go Wednesday, had reversed early gains after CPI inflation across the US rose 0.3% m/m in April and 8.3% y/y, but bounced back near highs by midmorning as longer Tsys discounted the inflation metric. Support evaporated, however, SPX emini futures extending session lows in the second half (ESM2 3937.5).

- Technicals for SPX eminis: S&P E-Minis remain vulnerable following last week’s sharp reversal in ESM2 from 4303.00 (May 4 high) and Mon’s move lower that resulted in a breach of support at 4056.00 (May 2 low). A clear break of this support confirmed resumption of the underlying downtrend w/ attn on 3892.98, a Fibonacci projection.

- Earnings cycle winding down, Walt Disney (DIS) and Rivian Automotive (RIVN) after the close.

- SPX leading/lagging sectors: Energy sector outperforms but off highs (+2.19%) as energy and equipment servicing names outpace O&G consumables. Utilitiessector up next (+1.32%) outpacing Materials (+0.78%).

- Laggers: Extending losses Consumer Discretionary (-3.02%) and Information Technology (-2.86%) weighed by hardware makers.

- Meanwhile, Dow Industrials currently trades -342.5 points (-2.9%) at 11400.09, Nasdaq -228.82 points (-0.71%) at 31945.59.

- Dow Industrials Leaders/Laggers: United Health Care (UNH) had traded 500.23 high before noon reversed direction trading 487.81 late. Chevron (CVX) +3.57 at 164.36 and Caterpillar (CAT) +3.69 at 206.68. Laggers: Microsoft (MSFT) -7.98 at 261.54, Apple (AAPL) -7.64 at 146.84 and Home Depot (HD) continues to sag -5.50 at 285.66.

- RES 4: 4509.00 High Apr 21 and a key short-term resistance

- RES 3: 4393.25 High Apr 22

- RES 2: 4328.66 50-day EMA

- RES 1: 4099.00/4303.50 High May 9 / High Apr 26/28

- PRICE: 3952.00 @ 1525ET May 11

- SUP 1: 3947.25 Intraday low

- SUP 2: 3892.98 2.23 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 3: 3843.25 Low Mar 25 2021 (cont)

- SUP 4: 3820.25 2.50 proj of the Mar 29 - Apr 18 - 21 price swing

S&P E-Minis remain vulnerable following last week’s sharp reversal from 4303.00, May 4 high, and this week’s extension of the downtrend. Monday’s move lower resulted in a breach of support at 4056.00, May 2 low. A clear break of this support confirms a resumption of the underlying downtrend and opens 3892.98 next, a Fibonacci projection. On the upside, key resistance has been defined at 4303.50, the Apr 26/28 high.

COMMODITIES: Oil Clears 20-Day EMA On Stronger Demand, Limited Supply

- Oil prices surge after two day’s of sizeable declines, following potential improvements in China’s Covid situation and a boost from EIA data showing gasoline inventories dropping to their lowest level of 2022 as crude production falls for the first time since Jan whilst diesel stockpiles hit a 17-year low.

- It comes despite Hungary holding firm in its stance against being part of the EU oil ban against Russia, only withdrawing its veto threat against sanctions if its imports via pipelines were excluded.

- WTI is +5.8% at $105.51, clearing the 20-day EMA of $103.56 whilst opening $111.37 (May 5 high).

- The most active strike in the CLM2 contract remained in puts for the second day running, at $95/bbl.

- Brent is +4.6% at $107.18, clearing the 20-day EMA of $106.58 whilst opening $114.00 (May 5 high).

- Gold is +0.76% at $1852.19 on the back of stronger US inflation, nearing resistance at $1865.4 (May 10 low) with support formed at the intraday low of $1832.1.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/05/2022 | 2301/0001 | * |  | UK | RICS House Prices |

| 12/05/2022 | 0001/0101 | ** | | UK | IHS Markit/REC Jobs Report |

| 12/05/2022 | 0600/0700 | ** | | UK | Index of Services |

| 12/05/2022 | 0600/0700 | ** | | UK | UK Monthly GDP |

| 12/05/2022 | 0600/0700 | *** | | UK | Index of Production |

| 12/05/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 12/05/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 12/05/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 12/05/2022 | 0600/0700 | *** | | UK | GDP First Estimate |

| 12/05/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 12/05/2022 | 1230/0830 | *** | | US | PPI |

| 12/05/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 12/05/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 12/05/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 12/05/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 12/05/2022 | 1535/1135 |  | CA | BOC Deputy Gravelle speech on commodity shocks. | |

| 12/05/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/05/2022 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 12/05/2022 | 1800/1400 | *** |  | MX | Mexico Interest Rate |

Why Subscribe to

MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.