Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Treasuries continued to march off last week's lows following lower than expected ADP private jobs gains, mixed ISM Services, and to some degree after the Bank of Canada cut rates.

- Strong buying in Information Technology sector shares helped Nasdaq index mark new all-time highs, S&P Eminis nearing May 23 all-time highs while DJIA gained - remained well off +40,000 all-time high.

- Focus on Thursday's Weekly Claims and Unit Labor Costs ahead of Friday's headline Non-Farm Payrolls.

US TSYS Already Anticipating In-Line to Lower NFP

- Treasuries looked to finish moderately higher Wednesday, upper half decent session range after early data-tied volatility. Treasury futures initially gapped higher after lower than expected ADP jobs gain of +152k vs. +175k est (192k prior down-revised to +188k).

- Not much of a reaction to in-line S&P Global US Services PMI final (54.8 vs. 54.8 est), while Composite PMI gains slightly (54.5 vs. 54.2 est).

- Fast two-way flow reported as Treasury futures retraced from a gap-bid to new session high of 110-12.5 (near April 5 levels) after mixed ISM Services data: Index higher than exp (53.8 vs. 51.0 est), lower Prices Paid (58.1 vs. 59.0 est), in-line Employment (47.1 vs. 47.2 est), higher New Orders (54.1 vs. 53.2 est).

- Late year rate cut projections have gradually gained vs. late Tuesday levels (*): June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -18% w/ cumulative at -4.8bp (-4.3bp) at 5.283%, Sep'24 cumulative -19.8bp (-19.3bp), Nov'24 cumulative -28.9bp (-27.8bp), Dec'24 -47bp (-44.3bp).

- Focus turns to Thursday's weekly claims and Unit Labor costs as well as the ECB policy announcement, followed by Friday's headline Non-Farm payrolls data.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00039 to 5.32791 (-0.00190/wk)

- 3M -0.00098 to 5.33751 (-0.00533/wk)

- 6M -0.01397 to 5.28465 (-0.02954/wk)

- 12M -0.03971 to 5.11324 (-0.08873/wk)

- Secured Overnight Financing Rate (SOFR): 5.33% (-0.02), volume: $2.092T

- Broad General Collateral Rate (BGCR): 5.32% (+0.00), volume: $787B

- Tri-Party General Collateral Rate (TGCR): 5.32% (+0.00), volume: $769B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $100B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $280B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage slips to $371.841B from $377.825B prior; number of counterparties at 76. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

SOFR/TEASURY OPTION SUMMARY

Heavier SOFR and Treasury option volumes turned mixed Wednesday as some accounts started to fade the ongoing rise in the underlying after this morning's lower than expected ADP private employment and mixed ISM services data. Late year rate cut projections have gradually gained vs. late Tuesday levels (*): June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -18% w/ cumulative at -4.8bp (-4.3bp) at 5.283%, Sep'24 cumulative -19.8bp (-19.3bp), Nov'24 cumulative -28.9bp (-27.8bp), Dec'24 -47bp (-44.3bp).

- SOFR Options:

- +6,000 0QZ4 96.25/2QZ4 96.50 call diagonals 2.75

- 3,000 SFRQ4 94.68/94.75/94.81/94.87 put condors ref 94.88

- +5,000 SFRQ4 95.00/95.12 call spds 1.875 ref 94.875

- +5,000 SFRZ4 95.25 calls, 19.0 ref 95.13

- -10,000 SFRU4 94.68/94.75 2x1 put spds .625 ref 94.885

- +5,000 SFRN4 94.62/94.68/94.87/94.93 iron condors 2.25 vs. 94.865/0.10%

- +12,000 SFRQ4 95.00/95.12/95.25 call flys, 1.0 vs. 94.895/0.05%

- Block, 7,000 SFRN4 94.75 puts 2.25 vs. SFRU4 94.68/94.81 put spds, 6.5 ref 94.88

- Block, 5,000 SFRZ4 95.06/95.75/96.50 broken call flys, 11.5

- Block, 5,000 SFRZ4 95.00/95.56/96.25 call flys, 12.0 ref 95.125

- 11,000 SFRZ4 94.75 puts ref 95.135

- 3,500 0QM4 95.50 puts ref 95.625 post-ADP

- +5,000 SFRH5 95.50/96.00 call spds, ref 95.385 pre-ADP

- 4,000 SFRZ4 95.00/95.12 4x3 put spds, ref 95.13

- Block, 3,100 SFRZ 94.37/94.62 2x1 put spds, 0.5 vs. 95.07/0.05%

- Block/screen, 5,500 SFRM4 94.56/94.62/94.68 put flys, 2.5 vs. 94.665/0.40%

- 1,500 SFRZ4 94.75/95.75 strangles ref 95.115

- 4,000 0QU4 96.00/96.50 call spds

- Treasury Options:

- Block, 5,000 UXYN4 114.5 calls, 38 ref 113-31.5

- over 5,700 TUN4 101.62 puts ref 102-05.25

- 3,000 FVQ4 106.75 calls, ref 106-20

- 6,500 wk2 TY 108 puts, 3

- Block/screen: 29,500 wk2 FV 106.25 calls vs. 7,625 FVU at 106-17 at 0823:35ET expires next week Friday

- Block/screen: 15,000 wk1 TY 109.5 calls 44 vs. 5,550 TYU4 at 110-02.5 at 0821:21ET, expires this Friday

- 5,000 wk2 TY 112.5/113 call spds ref 110-00.5

- Block, +10,000 TYN4 111 calls 19 vs. 109-30/0.28%

- 2,000 TYN4 112/113 call spds ref 109-30

- 2,000 TYU4 110.5 calls, 104 ref 109-29

- 2,000 TYN4 107.25 puts ref 109-31.5

- -3,000 wk2 TY 109 puts, 14 expire next week Friday

- +4,000 wk1 TY 109.25/109.75 put spds vs. 110.5 calls, 0.0 net, expire Friday

- +4,400 TYN4 109/109.75 put spds, 18 ref 110-00

- Block, -10,000 TYN4 109/109.5/110.25 broken call trees, 15 w/ TYN4 108.75 puts 13

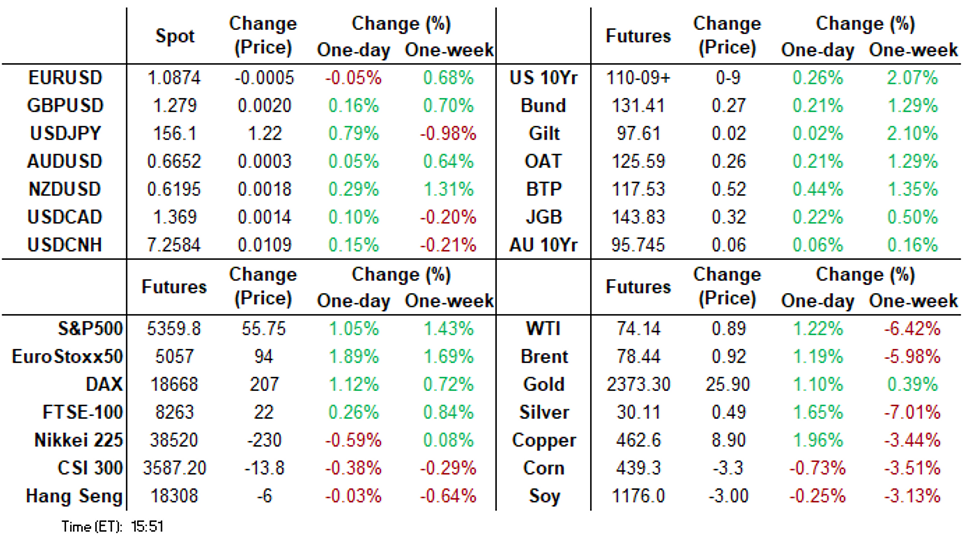

FOREX JPY Consolidates Early Decline, Moderately CAD Weakness as BoC Cuts

- Following the strong JPY rally this week, more optimistic price action for global equities has seen the Japanese Yen retrace substantially on Wednesday. USDJPY stands up 0.83% on the session, having risen back above the 156 handle, where it has been consolidating across the majority of the US session.

- On Tuesday, initial support was exposed at 154.66, the 50-day EMA. Despite the level being pierced (154.55 low), the strong subsequent bounce keeps this key support zone intact for now. Adding weight to this area, 153.93, a trendline drawn from the Dec 28 low, remains the key support. For bulls, a move above 157.71, the May 29 high, is required to resume a short-term uptrend.

- A first 25bp cut from the Bank of Canada and a signal to likely cuts ahead prompted some sharp initial weakness for the Canadian dollar. The immediate spike higher in USD/CAD saw the pair reach highs of 1.3741 before slowly edging back towards the 1.3700 mark as we approach the APAC crossover.

- With the ECB also taking place this week, it is worth noting that EURCAD printed as high as 1.4929, a fresh 6-month high. The cross notably pierced above trendline resistance from the July 2020 highs, and a close above this mark will be closely monitored in coming sessions.

- The more stable risk backdrop also weighed on the Swiss Franc, although the move lagged the Japanese Yen leg lower, as SNB’s Jordan’s recent hawkish remarks continue to add a short-term boost to the Swiss Franc. EURCHF continues to oscillate either side of 0.9700 and remains 2.2% below last week’s highs.

- EURUSD trades a tight range ahead of the ECB, just below the 1.0900 mark. Despite the pullback in EURUSD from Tuesday’s high, a bull cycle remains in play and sights are on 1.0933, a Fibonacci retracement.

- ECB decision and press conference takes focus on Thursday. US jobless claims is also scheduled, likely to play second fiddle to Friday’s US employment report for May.

FX OPTIONS: Expiries for Jun06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0850-65(E1.9bln), $1.0895-15(E5.2bln)

- USD/JPY: Y155.15($1.3bln), Y155.45-50($2.4bln), Y157.00($1.5bln), Y157.50($732mln), Y157.85-00($1.6bln), Y158.50($1.1bln)

- GBP/USD: $1.2550-65(Gbp1.1bln), $1.2845-60(Gbp680mln)

- EUR/JPY: Y167.80-00(E1.4bln)

- AUD/USD: $0.6700(A$507mln)

- NZD/USD: $0.6050(N$518mln)

- USD/CNY: Cny7.2450($1.2bln)

Late Equity Roundup: What Data Risk? Nasdaq, Eminis Make New All-Time Highs

- Stocks continue to extend gains in late Wednesday trade, Nasdaq marking new all-time-high of 17,151.44. Meanwhile, S&P Eminis climbing to 5360.00 session high -- not far off all-time-high of 5368.25 on May 23, DJIA around 38,830.0 still off May 17 all-time-high of 40,003.59.

- Information Technology and Communication Services sectors continued to lead gainers in late trade, semiconductor makers supporting the former: Applied Materials +5.83%, Lam Research +5.36%, Broadcom +5.35%, Micron +5.14%. Notable mention: cyber security company Crowdstrike surged 10.85% after beating Q1 results.

- Interactive media and entertainment shares buoyed the Communication Services sector: Meta +2.36%, Netflix +2.11%, News Corp +1.89%.

- On the flipside, Consumer Staples and Utility sector shares underperformed: household and personal products weighed on Staples as they unwound the prior session' support: Brown-Forman-5.36%, Bunge Global -3.62%, Target -2.27. Multi energy providers weighed on the Utility sector: Eversource -1.83%, DTE -1.47%, First Energy -1.39%.

- Meanwhile, notable earnings releases still to come this week: Five Below Inc, Semtech Corp, Victoria Secret, Toro, Vail Resorts and Docusign.

E-MINI S&P TECHS: (M4) Recovery Extends

- RES 4: 5417.75 2.00 proj of the Apr 19 - 29 - May 2 price swing

- RES 3: 5400.00 Round number resistance

- RES 2: 5372.73 1.764 proj of the Apr 19 - 29 - May 2 price swing

- RES 1: 5368.25 May 28 high and a bull trigger

- PRICE: 5360.50 @ 1505 ET Jun 5

- SUP 1: 5246.75/5205.50 Low Jun 3 / Low May 31 and a key support

- SUP 2: 5155.75 Low May 6

- SUP 3: 5099.25 Low May 3

- SUP 4: 5036.25 Low May 2

The uptrend in S&P E-Minis, remains intact. The recovery from last Friday’s low is a positive development, a continuation would open 5368.25, the May 25 high, and a breach of this level would resume the primary uptrend. A recent corrective pullback has resulted in a test of support at the 50-day EMA, at 5219.79. A clear break of this average is required to signal scope for a deeper retracement.

COMMODITIES Crude Finds Late Support, Gold Recovers

- Crude markets have found support during US hours, despite an unexpected crude stock build in the latest EIA data. WTI is likely readjusting after steep losses yesterday.

- WTI Jul 24 is up by 1.2% at $74.1/bbl.

- For WTI futures, the theme is bearish, with sights on $71.33 next, the Feb 5 low. Initial resistance is at $76.15, the May 24 low and a recent breakout level.

- Meanwhile, Henry Hub is up strongly from yesterday’s close, although it remains within yesterday's trading range.

- US Natgas Jul 24 is up 6.8% at $2.76/mmbtu.

- Gold has risen by 1.3% today to $2,356/oz, keeping the yellow metal in the $2,320-2,360 it has been in for most of the last nine sessions.

- A bear cycle in gold remains in play for now, although the medium-term trend structure is bullish and the recent move down appears to be a correction that is allowing an overbought condition to unwind.

- A resumption of gains would open $2,452.5 next, a Fibonacci projection. The 50-day EMA, at $2,312.0, represents a key support.

- Copper is up by 1.9% on the day at $462.5/lb.

- A clear break of support at 455.07, the 50-day EMA, would suggest potential for a deeper retracement. Key resistance has been defined at 519.90, the May 20 high.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/06/2024 | 0130/1130 | ** |  | AU | Trade Balance |

| 06/06/2024 | 0130/1130 | ** | | AU | Lending Finance Details |

| 06/06/2024 | 0545/0745 | ** |  | CH | Unemployment |

| 06/06/2024 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/06/2024 | 0700/0900 | ** |  | ES | Industrial Production |

| 06/06/2024 | 0730/0930 | ** |  | EU | S&P Global Final Eurozone Construction PMI |

| 06/06/2024 | 0800/1000 | * |  | IT | Retail Sales |

| 06/06/2024 | 0830/0930 | ** |  | UK | S&P Global/CIPS Construction PMI |

| 06/06/2024 | 0830/0930 | | UK | BOE's Decision Maker Panel Data | |

| 06/06/2024 | 0900/1100 | ** | | EU | Retail Sales |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 06/06/2024 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 06/06/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 06/06/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 06/06/2024 | 1230/0830 | ** | | US | Trade Balance |

| 06/06/2024 | 1230/0830 | ** | | US | Non-Farm Productivity (f) |

| 06/06/2024 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 06/06/2024 | 1245/1445 | | EU | ECB Monetary Policy Press Conference | |

| 06/06/2024 | 1400/1000 | * | | CA | Ivey PMI |

| 06/06/2024 | 1415/1615 | | EU | ECB's Lagarde presents monpol decision on podcast | |

| 06/06/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 06/06/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 06/06/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.