Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI SECURITY: Kremlin: Russia Intends To Develop Relations With Turkey

- MNI TURKEY: Turkey: Improving Ties With West Will Not Harm Relations With Russia

- MNI NATO: Vilnius Summit To Provide Clarity On Ukraine's NATO Membership Prospects

- MNI NATO: Stoltenberg: Ukraine To Join NATO When Allies Agree And Conditions Are Met

- XI, BIDEN TO TALK IN MONTHS AHEAD, BLINKEN TELLS NBC, Bbg

- US TREASURY: LARGE POSITION REPORTS REQUIRED FOR POSITIONS AS OF APRIL 28 AND MAY 5; REPORTS ARE DUE BY NOON EDT ON JULY 17 .. CALLING FOR LARGE POSITION REPORTS FROM ENTITIES HOLDING $10.2 BLN OR MORE OF 6-MONTH TREASURY BILL THAT MATURED ON JUNE 8, 2023, Reuters

Key Links: MNI US CPI Preview: Core Seen Softer On Used Cars Drag / MNI INTERVIEW: Real Wage Growth Boost In Coming Months For UK / MNI: EC Call For Prudent ‘24 Fiscal Policies To Support ECB

US TSYS: Markets Roundup: Curves Flatten Ahead June CPI

- Generally quiet trade Tuesday, carry-over support in intermediate (TYU3 +5.5 at 111-10, 3.976% yield) to long-end rates from Monday while curves scaled back a portion of steepening (2s10s -3.704 at -90.719) over the last week ahead tomorrow's CPI inflation metric.

- Consensus puts core CPI inflation at 0.3% M/M in June as it slowed from a modest beat of 0.44% in May. There is no evidence that the downside miss in nonfarm payroll gains last Friday has deterred FOMC participants from signaling their preference to raise rates twice more this year.

- An above-expected print and/or a report with strong details in ex-shelter services would reinforce the "higher for longer" theme; a miss most impactful for September pricing.

- Fed Funds implied rates remain unchanged for the Jul 26 decision (+22bp) but beyond that have edged higher on the day after reversing an overnight decline that continued from yesterday’s second half softer trading.

- Cumulative change from 5.08% effective: +22bp Jul (unch), +28.5bp Sep (unch), +35bp Nov (+1bp), +30bp Dec (+1bp), +21.5bp Jan (+1bp). Rates are first seen lower than they are today with the May meeting (-8bps, +0.5bp on the day). Cuts from Nov terminal: 5bp Dec’23, 63bp Jun’24 and 135bp Dec’24.

- Fed speaker schedule for tomorrow includes: Richmond Fed Barkin (0830ET), MN Fed Kashkari (0945ET), Atlanta Fed Bostic (1300ET) and Cleveland Fed Mester (1600ET)

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00257 to 5.19643 (+.01942/wk)

- 3M +0.00159 to 5.30109 (+.00262/wk)

- 6M -0.00096 to 5.40243 (-.01257/wk)

- 12M -0.02333 to 5.38527 (-.06915/wk)

- Daily Effective Fed Funds Rate: 5.08% volume: $125B

- Daily Overnight Bank Funding Rate: 5.07% volume: $270B

- Secured Overnight Financing Rate (SOFR): 5.06%, $1.506T

- Broad General Collateral Rate (BGCR): 5.04%, $597B

- Tri-Party General Collateral Rate (TGCR): 5.04%, $586B

- (rate, volume levels reflect prior session)

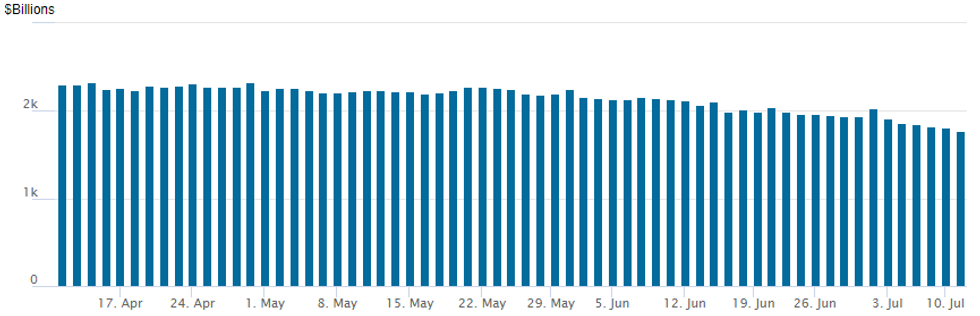

FED Reverse Repo Operation: Continues to Recede

NY Federal Reserve/MNI

Latest operation falls to $1,775.796B, lowest since early May'22, w/ 101 counterparties, compared to $1,811.981B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

Better put volumes on net carried over from overnight trade, fading the carry-over support in underlying futures ahead of tomorrow's key CPI data. Salient trade is Dec'23 SOFR put condor hedging two 25bp rate hikes by year end, while a second account hedged a less hawkish year-end view with Dec'23 SOFR 94.00/94.12/94.25 put flys. On the flipside, Green Dec'23 call spd looking for rate cuts to price into late 2025 futures.

- SOFR Options:

- +35,000 SFRZ3 94.00/94.12/94.25 put flys, 1.25

- 4,000 OQN3 95.68/95.81/96.00 call flys

- -10,000 OQZ3 95.0/95.12 put spds,2.75 ref 95.94

- +3,500 SFRH4 94.00/95.50 strangles, 34.0-34.5

- 3,000 SFRV3 95.37/96.37 call spds vs. 3QV3 97.25 calls

- +10,000 SFRU3 94.75/95.00/95/25 call flys, 1.25

- 4,800 SFRU3 95.00 calls ref 94.59

- 1,000 SFRQ3 94.56/94.68/94.81 put flys

- +32,700 SFRZ3 93.50/93.75/94.00/94.50 broken put condors ref 94.665 to -.65

- 1,000 SFRQ3 94.37/94.43/94.50 put flys ref 94.59

- 3,000 SFRN3 94.37/94.50/94.62 put flys ref 94.585

- +8,000 2QZ3 98.00/98.50 call spds, 2.0 ref 96.44 to -.425

- 2,000 SFRH4 95.37/95.62/95.87/96.12 call condors ref 94.915

- Treasury Options:

- 5,000 TYQ3 111.25/112/112.25 broken call flys ref 111-06

- 11,000 FVU3 95.00 puts, .5 ref 106-20.5

- 1,500 USU3 125/128/131 call flys

- over 6,400 TYQ3 112.75 calls, 11 ref 111-13 to -12.5

- over 6,100 TYQ3 110.5/111.25 put spds vs. TYQ3 112.25 calls ref 111-15

- 3,000 TYQ3 109 puts, 4 ref 111-15

- 2,000 TYU3 108.5/109.5 put spds, 14 ref 111-13.5

- 2,000 TYU3 109.5/110.5 put spds, 20 ref 111-12

- 2,300 TYQ3 112 calls, 23 ref 111-10

- 1,000 TYU3 108.5 puts ref 111-09.5

- 1,000TYQ3 113 calls ref 111-08

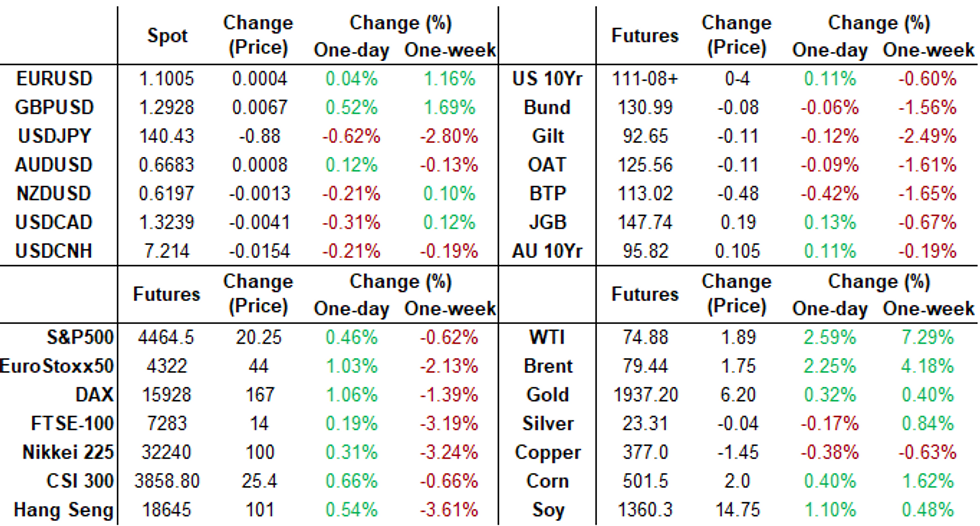

EGBs-GILTS CASH CLOSE: Weakness Resumes Post-UK Jobs, Pre-US CPI

Core European curves bear flattened Tuesday, with Gilts underperforming Bunds following May's UK labour market data.

- The UK jobs report was initially interpreted as mixed, with Gilts initially weakening on higher-than-expected wage numbers, then reversing higher on the higher unemployment rate signalling labour market slack.

- By session's end though Gilts had weakened with BoE hike pricing firming, as analysts focused on potential for further 50bp hikes on the robust wage data.

- Movements in Bunds followed suit, with global core FI weakening in the latter half of the session amid anticipation over Wednesday's US CPI print.

- BTPs underperformed on the periphery, with 10Y spreads to Germany closing at the widest level in over a month. GGBs steadied out after weakening sharply Monday on the announcement of the 15Y syndication held today.

- Wednesday has a busy docket with the release of the BoE's financial stability report and Spanish final CPI in the morning, with the main focus being US CPI in the afternoon.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.7bps at 3.316%, 5-Yr is up 1.2bps at 2.769%, 10-Yr is up 0.9bps at 2.649%, and 30-Yr is up 1.4bps at 2.66%.

- UK: The 2-Yr yield is up 5.6bps at 5.426%, 5-Yr is up 4.2bps at 4.886%, 10-Yr is up 2.3bps at 4.663%, and 30-Yr is up 2bps at 4.697%.

- Italian BTP spread up 2.3bps at 176.9bps / Spanish up 1.2bps at 106.7bps

EGB Options: More Call Structure Interest Seen Tuesday

Tuesday's Europe rates / bond options flow included:

- SFIQ3 94.25/94.50 1x1.5 call spread paper paid 3.5 on 4K

- RXU3 135.50/136.50/137.50/138.50 call condor paper pays 7 on 3K.

- RXU3 134/135/136 call fly paper paid 7 on 7.4K

FOREX: NZD Underperforms Ahead of RBNZ, USDJPY Extends Losing Streak

- The softer USD backdrop has persisted into a fourth session, with the USD Index edging to the lowest levels since mid-may. The pullback after nonfarm payrolls has extended and the DXY has printed as low 101.67, narrowing the gap with the next major support of 101.03. The New Zealand dollar screens as the weakest in G10, interesting given the RBNZ decision is due overnight. New Zealand’s central bank is likely to remain on hold for the first time since August 2021.

- USD/JPY typifies the soft USD theme, with the pair lower for a fourth consecutive session and attention firmly on support at the 50-day EMA that intersects around current levels at 140.34. A clear break of this average would strengthen bearish conditions, opening 139.85, the Jun 16 low and 139.18, the 38.2% retracement of the Mar 24 - Jun 30 bull leg.

- AUD and EUR are also among the poorest performers in G10, with AUD/JPY a stand out cross at these levels: AUD/JPY is now on a five session losing streak, with the 50-dma the next level to watch at 93.439.

- NOK tops the G10 FX table once more on Tuesday, extending Monday’s move following the higher-than-expected CPI for June and notable acceleration for core measures. USD/NOK has declined around 1.2% and has significantly narrowed the gap with the April lows of 10.2451.

- A busy Wednesday is headlined by US inflation data as well as RBNZ and BOC rate decisions. There may also be comments from both RBA Governor Lowe and BOE Governor Bailey.

FX: Expiries for Jul12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0775(E547mln), $1.0780-00(E2.6bln), $1.0900(E599mln), $1.0935-55(E1.1bln), $1.0985-00(E1.3bln)

- EUR/JPY: Y156.00(E891mln)

- USD/CNY: Cny7.2300($816mln)

Late Equity Roundup: Shrugging Off Data Event Risk

- Stocks are close to revisiting midday highs in late trade, DJIA is currently up 230.55 points (0.68%) at 34175.19, S&P E-Mini Future up 16.75 points (0.38%) at 4460.75, Nasdaq up 30.4 points (0.2%) at 13716.25.

- Leading gainers: Energy sector continues to lead Tuesday's gainers on the back of strong crude prices (WTI +1.90 at 74.89). Equipment and Servicer shares leading w/ Haliburton + 4.5%, Schlumberger +4.3% and Baker Hughes +2.50%.

- Meanwhile Financials sector outpaces Industrials in the second half with banks outperforming: Key +3.65%, USB +3.5%, Comerica +3.25% and Citizens Financial Grp +3.15%.

- Of note, Communication Services sector remained strong, buoyed by shares of Activision +10.1% as courts allow Microsoft acquisition to go forward -- barring FTC injunction. Other leading gainers: Electronic Arts +5.05%, Paramount Global +3.60% and Omnicom Grp +3.35%.

- Laggers: Health Care, Information Technology and Consumer Staples underperformed, semiconductor shares weighing on IT: Applied Materials -4.5%, KLA Corp -3.1%, Advanced Micro Devices -3.0%.

- The technical/bull theme in S&P E-minis bull theme remains intact. Attention is on the first support 4415.05, the 20-day EMA. Clearance of this level would strengthen a bearish threat and expose 4368.50, the Jun 26 low and a key support. The bull trigger is at 4498.00, the Jun 16 high. A clear breach of this level would confirm a resumption of the uptrend and open 4532.08, a Fibonacci projection.

E-MINI S&P TECHS: (U3) Watching Support At The 20-Day EMA

- RES 4: 4562.88 Bull channel top drawn from the Mar 13 low

- RES 3: 4556.71 2.382 projection of the May 4 - 19 - 24 price swing

- RES 2: 4532.08 2.236 projection of the May 4 - 19 - 24 price swing

- RES 1: 4498.00 High Jun 30 and the bull trigger

- PRICE: 4460.75 @ 1530ET Jul 11

- SUP 1: 4415.05/4368.50 20-day EMA / Low Jun 26 and a key support

- SUP 2: 4330.86 50-day EMA

- SUP 3: 4321.67 Bull channel base drawn from the Mar 13 low

- SUP 4: 4269.50 Low Jun 2

A bull theme in S&P E-minis remains intact and the pullback last week appears to be a correction - for now. Attention is on the first support 4415.05, the 20-day EMA. Clearance of this level would strengthen a bearish threat and expose 4368.50, the Jun 26 low and a key support. The bull trigger is at 4498.00, the Jun 16 high. A clear breach of this level would confirm a resumption of the uptrend and open 4532.08, a Fibonacci projection.

COMMODITIES: Crude Sees Further Gains With WTI Attention Turning To A Key Resistance

- Crude prices found further strengths in today’s session, rising to the highest level since 2 May and breaking through resistance, supported by signs of lower Russian exports and the potential for further China policy support measures for the country’s property sector.

- Russian seaborne crude exports are showing signs of a decline with exports falling just over 1mbpd WoW as of 9 July. Russian Urals crude prices rose to $57.70/bbl as of Friday, just below the G7 price cap.

- Saudi Aramco plans to supply full nominated volumes of crude in August to North Asia, following the extended output cut and OSP hike. China requested once again less supply. Two major European refiners requested less volumes. The cut is starting to weigh on mediums and heavy sour barrels availability.

- WTI is +2.3% at $74.69, pushing through $74.15 (Jul 10 high) to open a key resistance at $75.70 (Jun 5 high).

- Brent is +2.0% at $79.26. Yesterday’s piercing of $78.47 (Jun 5 high) has opened further gains, clearing $78.77 (Jul 10 high) to next focus on $79.94 (6.18% retrace of Apr 12 – May 4 downleg).

- Gold is +0.3% at $1931.27 with the USD under mild pressure today. It’s off a high of $1938.35 that moved closer to, but didn’t trouble, resistance at $1944.3 (50-day EMA). The trend direction signals remain bearish though, with support at $1893.1 (Jun 29 low).

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/07/2023 | 0200/1400 | *** |  | NZ | RBNZ official cash rate decision |

| 12/07/2023 | 0600/0700 |  | UK | BOE FPC Summary and Record | |

| 12/07/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 12/07/2023 | 0800/0900 | | UK | Financial Stability Report press conference | |

| 12/07/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 12/07/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/07/2023 | 1230/0830 | *** | | US | CPI |

| 12/07/2023 | 1230/0830 | | US | Richmond Fed's Tom Barkin | |

| 12/07/2023 | 1345/0945 | | US | Minneapolis Fed's Neel Kashkari | |

| 12/07/2023 | 1345/1545 |  | EU | ECB Lane panels at NBER conference. | |

| 12/07/2023 | 1400/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 12/07/2023 | 1400/1000 | | CA | Bank of Canada Monetary Policy Report | |

| 12/07/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 12/07/2023 | 1500/1100 | | CA | Bank of Canada Governor press conference | |

| 12/07/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/07/2023 | 1700/1300 | | US | Atlanta Fed's Raphael Bostic | |

| 12/07/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 12/07/2023 | 1800/1400 | | US | Fed Beige Book | |

| 12/07/2023 | 2000/1600 | | US | Cleveland Fed's Loretta Mester |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.