Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI MIDEAST: Biden Could Meet MBS On G20 Sidelines-Axios

- MNI US-CHINA: Politico: Commerce Sec Raimondo To Travel To China This Week

- MNI US: House Freedom Caucus Outlines Conditions For Supporting Govt Funding Stopgap

- The Fed Should Carefully Aim for a Higher Inflation Target, Op-Ed, WSJ

- MICRON: DEVELOPMENT OF MEMORY MANUFACTURING FAB IN BOISE, IDAHO, Bbg

- German Economy to Stagnate Again in 3Q, Bundesbank Says, DJ

cropfilter_vintageloyaltyshopping_cartdelete

Markets Roundup: Bonds Near Lows

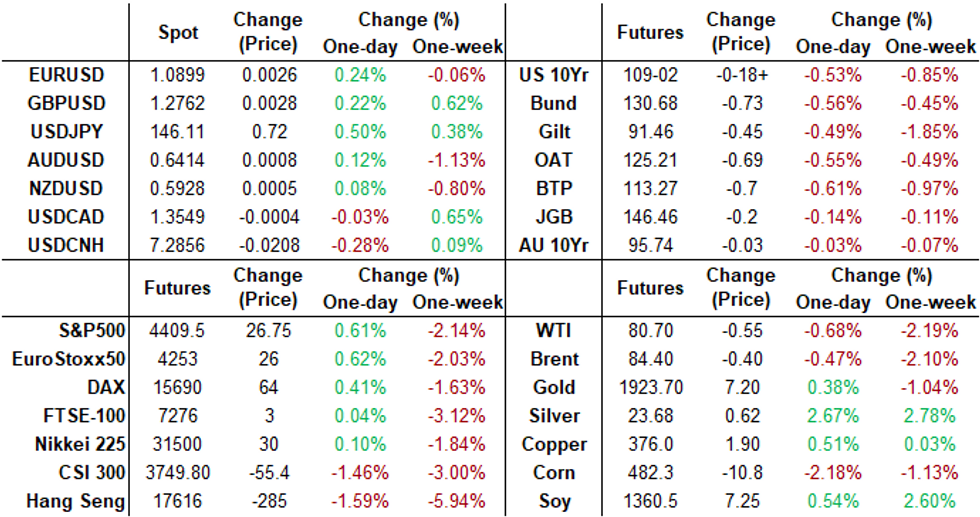

- Treasury futures remain weaker but off lows after extending new cycle lows in late morning trade. Sep'23 10Y futures slipped below round number technical support of 109-00 (-20.5) to new contract low of 108-31 briefly, yield climbing to the highest level since late 2007 at 4.3518%.

- There were no obvious headline, data or Block/cross driver for the curve steepening sell-off (3M10Y +8.273 at -110.785, 2Y10Y +3.629 at -65.590).

- ncoming high-grade supply and pre-auction hedging was only a factor in the short end to 3s. Some desks posited that Fed Chairman Powell will present a hawkish or "stay the course" to address inflation at the KC Fed's annual economic symposium in Jackson Hole, WY that kicks off Thursday evening and runs through Saturday.

- Technicals in play: The trend direction in Treasuries remains down and the contract has started the week on a bearish note, breaking to a fresh cycle low. The break confirms a resumption of the downtrend and maintains the bearish price sequence of lower lows and lower highs.

- Last week’s break of support at 109.24, the Aug 4 low, also confirmed a resumption of the bear cycle. The focus is on 108.19+, a Fibonacci projection. Firm resistance is 110-21+, the 20-day EMA.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00351 to 5.31778 (+.00377 total last wk)

- 3M -0.00583 to 5.37734 (+0.01860 total last wk)

- 6M -0.01552 to 5.42902 (+0.02946 total last wk)

- 12M -0.02767 to 5.35571 (+0.07756 total last wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $100B

- Daily Overnight Bank Funding Rate: 5.32% volume: $257B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.314T

- Broad General Collateral Rate (BGCR): 5.27%, $549B

- Tri-Party General Collateral Rate (TGCR): 5.27%, $541B

- (rate, volume levels reflect prior session)

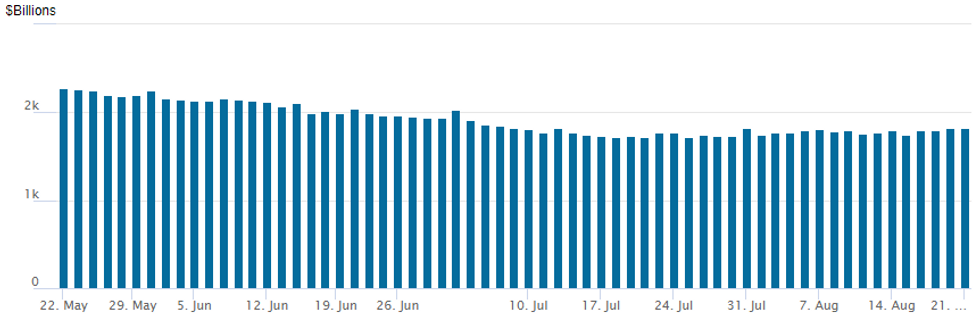

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

Repo operation climbs to $1,824.788B w/96 counterparties, compared to $1,819.201B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMMARY

Better SOFR call structure trade carried over from overnight through the NY session. Treasury options saw a late pick-up in call trade from mixed in the first half. Underlying futures remain weaker, but off contract lows (TYU3 109-04.5 vs. 108-31low). Rate hike projections through year end gained some traction on the move in futures, Sep 20 FOMC is 12% w/ implied rate change of +3bp to 5.359%. November cumulative of +11.1bp at 5.44, December cumulative of 9.6bp at 5.425%. Fed terminal at 5.44% in Nov'23.

- SOFR Options:

- Block/screen, over 10,600 SFRX3 94.56/94.62/94.68/94.81 broken call condors, 1.5 ref 94.61 to -.60

- 1,750 SFRZ3 94.75/94.87 call spds vs. SFRZ3 94.12/94.25 put spds

- 2,000 SFRZ3 95.00 calls, ref 94.605

- 2,500 SFRX3 94.37 puts ref 94.60

- 2,000 SFRX3 94.62/94.87/95.37 broken call flys ref 94.615

- 2,000 SFRV3 94.56/94.75/95.06 broken call flys ref 94.615

- Treasury Options:

- over 19,000 TYU3 110 calls, 7 ref 109-03 to -04, total volume over 43k

- 13,000 TYV3 113.5/TYX3 115 call spds

- Block, 8,000 TYX3 114.5/116 call spds 2 over TYV3 113/114 call spds

- 3,250 TYV3 109.5 puts, 56 ref 109-27.5, 7,725 total from 52 low

- 2,600 FVU3 106 calls, 12.5 last

- 5,300 TYV3 108 puts, 25

- 4,700 TYU3 110 calls, 12 last

- 4,500 TYU3 108.5 puts, 7 last

EGBs-GILTS CASH CLOSE: Bear Steepening Resumes

Core European FI weakened Monday higher ahead of event risk later in the week.

- Yields extended higher throughout most of the session on relatively low volumes, with curves steepening.

- 10Y Bund and Gilt yields neared last week's highs, but unlike their US counterparts which hit 2007 levels, did not quite break higher.

- Given the bear steepening move, though, it appears that the higher-for-longer-trade seen for most of last week has resumed.

- An overnight risk-off move following a smaller-than-expected lending rate cut by China saw limited follow-through in Europe. With sparse data (German PPI was more deflationary than expected but triggered little reaction) and no speakers, attention was kept on global flash PMIs and Powell and Lagarde speeches at Jackson Hole later this week.

- Periphery spreads tightened modestly, led by BTPs.

- This week's thin issuance schedule (Belgium sold OLOs today) continues Tuesday with Gilt Linkers and possible EFSF syndication.

- Tuesday we also get UK public finance and Eurozone current account data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 5.7bps at 3.116%, 5-Yr is up 7.9bps at 2.705%, 10-Yr is up 8.1bps at 2.703%, and 30-Yr is up 6.9bps at 2.8%.

- UK: The 2-Yr yield is up 4.1bps at 5.236%, 5-Yr is up 6bps at 4.75%, 10-Yr is up 5.4bps at 4.729%, and 30-Yr is up 5.1bps at 4.925%.

- Italian BTP spread down 1.3bps at 169.4bps / Spanish down 0.7bps at 104.8bps

EGB Options Downside In Favour In Light Monday Trade

Monday's Europe rates / bond options flow included:

- RXV3 125p, bought for 12 and 13 in 5k

- ERV3 96.25/96.125/96.00p ladder, bought for 2.5 in 6.5k

- ERH4 95.50/95.00ps 1x2, bought the 1 for 2 in 7k

FOREX USD Scales Back Yield-Driven Appreciation, But USDJPY Remains In Focus

- The USD index has ultimately reversed a large part of its rise seen through the first half of the US session in moves attributed to a marching higher in US yields, with the 10Y real touching fresh highs since 2009 to push the nominal yield to its highest since 2007 with a clearance of 4.35%. An only small paring of these FI losses has seen a surprisingly large paring in the DXY for -0.1% on the day, coinciding with a second half recovery in US equities.

- Higher yields have however underpinned the bounce for USDJPY. It may be off a session high of 146.404 but still trades at 146.13 (+0.5%), firmly re-establishing itself above the 146 handle.

- Last week's price action resulted in a break of 145.07, the Jun 30 high, which confirmed a resumption of the uptrend. Moving average studies are in a bull mode condition, highlighting current positive sentiment. The initial target on the topside will be 146.56, last week's high and a resistance that dates back to November last year. Above here, the focus will shift to 147.49, a Fibonacci projection.

- Reports continue to speculate over potential BOJ intervention, however, there has no been escalation of the usual rhetoric from MOF officials. Indeed, JPMorgan stated that Japan's threshold for currency market intervention on the yen is likely to be around 150 per dollar. Analysts noted that the fundamental conditions in the Japanese economy had been improving since the last time the MoF intervened to lift the yen in September and October last year.

Late Equity Roundup: IT Shares Holding Gains

- Stocks indexes are trading mostly higher in second half trade. IT sector, buoyed by semiconductor stocks continued to lead gainers Monday. At the moment S&P E-Mini futures are up 22.75 points (0.52%) at 4405, Nasdaq up 182.8 points (1.4%) at 13472.29. Dow weaker after posting early gains, down 61.47 points (-0.18%) at 34438.34.

- Leading gainers: Information Technology, Consumer Discretionary and Communication Services sectors are outperforming in late trade. Chip stocks buoying IT and outperforming software/hardware makers. Leaders include Palo Alto Networks +15.33%, Nvidia +6.35%, Broadcom +4.5%, Applied Materials +3.45%.

- Autos continue to lead Consumer Discretionary with Tesla bouncing +6.0% after trading weaker last Friday, parts maker Aptiv +0.5%. Media and entertainment shares buoyed Communication Services: Meta +2.15%, Google +0.6%, Netflix +0.25%.

- Laggers: Real Estate, Energy and Utilities underperforming, retail and residential Real Estate Investment Trust shares weighing on the former: SBA -2.4%, Essex Properties -2.0%, Invitation Homes -1.95%. O&G equipment and servicer names weighed on the Energy sector with Schlumberger -1.35%, Halliburton -1.25%, Baker Hughes -1.05%.

E-MINI S&P TECHS: (U3) Southbound

- RES 4: 4634.50 High Jul 27 and the bull trigger

- RES 3: 4593.50/4634.50 High Aug 2 / Jul 27

- RES 2: 4560.75 High Aug 4

- RES 1: 4455.92/4484.09 50- and 20-day EMA values

- PRICE: 4405.50 @ 14:25 ET Aug 21

- SUP 1: 4344.28 38.2% retracement of the Mar 13 - Jul 27 bull cycle

- SUP 2: 4305.75 Low Jun 8

- SUP 3: 4254.62 50.0% retracement of the Mar 13 - Jul 27 bull cycle

- SUP 4: 4216.00 Low May 31

A bearish theme in the E-mini S&P contract remains intact and Friday’s sell-off reinforces this theme. Last week’s extension lower resulted in a break of the 50-day EMA and the contract breached channel support drawn from the Mar 13 low. 4368.50, the Jun 26 low, was breached Friday and attention turns to 4344.28, a Fibonacci retracement. Initial firm resistance to watch is at the 50-day EMA - at 4455.92.

COMMODITIES Crude Reverses Gains Despite Dollar Reprieve

- Crude oil has given up earlier gains, with a sharp move lower since the end of the London session into the WTI settle despite a bounce in the S&P e-mini and the USD paring earlier appreciation.

- The market continues to weigh crosscurrents from OPEC+ output cuts and soft economic growth particularly in China.

- Crude in floating storage and stationary for at least seven days fell by 7% on the week to 111.96m bbl as of Aug. 18, according to Vortexa.

- The US oil rig count data showed a ninth decline in ten weeks according to the Baker Hughes data. The US crude oil rig count is now down to the lowest since March 2022 at 520. On the flip side, Kazakhstan’s daily oil production rose to 234.3k mt as of Aug. 20, surpassing the levels prior to electricity supply disruptions.

- WTI (CLV3) is -0.7% at $80.09, pulling back from a high of $81.75 that remained below the bull trigger at $84.16 (Aug 10 high).

- Brent (COV3) is -0.4% at $84.43, off the session high of $85.86 but not testing support at $82.36 (Aug 3 low).

- Gold is +0.3% at $1894.42 as the pullback in the USD index breathes some life into the yellow metal having touched lows of $1884.89 overnight and again faded to $1885.36 mid-session. Support is seen at that overnight $1884.9 whilst resistance is seen at $1920.7.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/08/2023 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 22/08/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 22/08/2023 | 0800/1000 | ** |  | EU | EZ Current Account |

| 22/08/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 22/08/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 22/08/2023 | - | * |  | FR | Retail Sales |

| 22/08/2023 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 22/08/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 22/08/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/08/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 22/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 22/08/2023 | 1830/1430 | | US | Chicago Fed's Austan Goolsbee | |

| 23/08/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.