Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

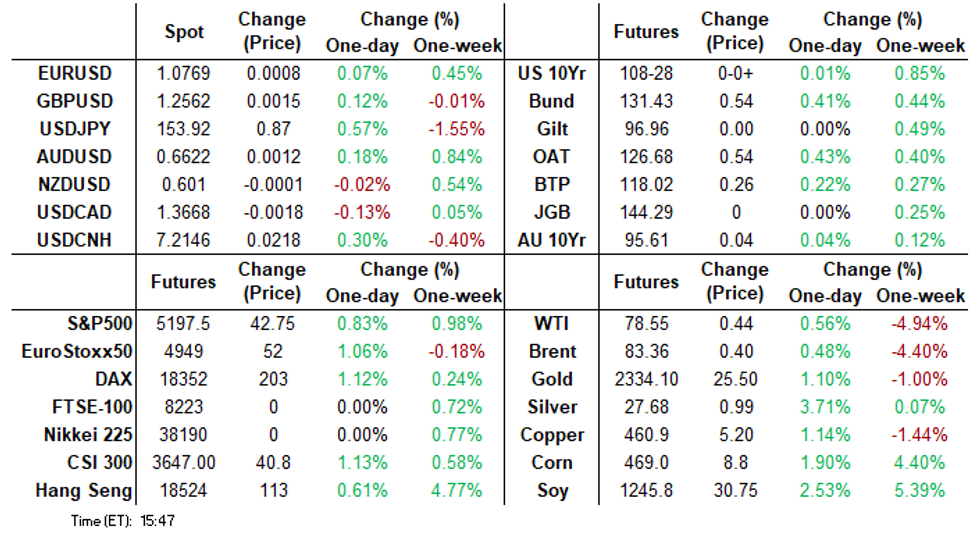

- Treasuries held to narrow range Monday, curves flatter with the long end outperforming.

- Projected rate cuts for year end receded slightly as short end rates underperformed.

- U.S. banks generally tightened lending standards for commercial and industrial loans, SLOOS report.

US TSYS Projected Rate Cut Pricing Already Starting to Recede

- Treasuries look to finish Monday's session steady to mixed, curves flatter with early session support in the short end evaporating as the session carried on. Quiet start to the week, lower volumes with Japan and London out for Spring holiday.

- Projected rate cut pricing looks steady to mildly cooler vs. this morning's levels: June 2024 steady at -10% w/ cumulative rate cut -2.5bp at 5.298%, July'24 at -24% w/ cumulative at -8.5bp at 5.238%, Sep'24 cumulative -20.7bp (-22.8bp earlier), Nov'24 cumulative -30.3bp (-32.8bp earlier). Dec'24 cumulative currently -43.7bp (-47.7bp earlier).

- Very little in the way of data all week, aside from today's Fed's Sr Loan Officer Opinion Survey on Bank Lending Practices, Initial and Continuing Jobless Claims report Thursday, UofM sentiment this Friday.

- SLOOS survey: U.S. banks generally tightened lending standards for commercial and industrial loans in the first quarter and also reported weaker demand, citing a less favorable or more uncertain economic outlook, less tolerance for risk, and worsening of industry-specific problems,

- Markets will be listening for Fed speakers, MN Fed Kashkari attends a fireside chat at the Milken Inst (text TBA, Q&A) Tuesday at 1130ET.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00111 to 5.32130 (+0.00668 total last wk)

- 3M -0.00635 to 5.32120 (-0.00195 total last wk)

- 6M -0.02445 to 5.28248 (-0.00729 total last wk)

- 12M -0.07156 to 5.13716 (-0.03508 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.863T

- Broad General Collateral Rate (BGCR): 5.30% (-0.01), volume: $706B

- Tri-Party General Collateral Rate (TGCR): 5.30% (-0.01), volume: $695B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $82B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $265B

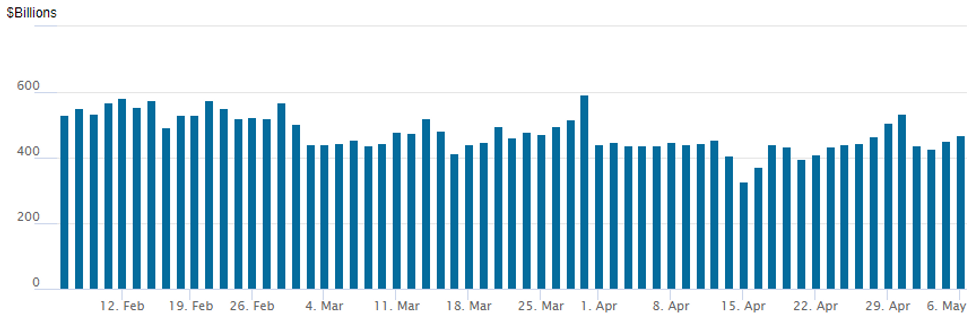

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage rises to $468.970B vs. $450.168B last Friday. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

- Meanwhile, the latest number of counterparties slips to 67 from 70 prior.

SOFR/TEASURY OPTION SUMMARY

Continued two-way SOFR and Treasury options reported Monday, short end rates weaker as projected rate cut pricing looks steady to mildly cooler vs. this morning's levels: June 2024 steady at -10% w/ cumulative rate cut -2.5bp at 5.298%, July'24 at -24% w/ cumulative at -8.5bp at 5.238%, Sep'24 cumulative -20.7bp (-22.8bp earlier), Nov'24 cumulative -30.3bp (-32.8bp earlier). Dec'24 cumulative currently -43.7bp (-47.7bp earlier).

- SOFR Options:

- +5,000 SFRM4 96.00/96.31 call spds, 0.25 ref 94.72

- -10,000 SFRZ4 94.75 puts, 8.5 vs

- +5,000 0QZ4 95.37 puts, 21 vs. 95.89/0.30%

- +10,000 SFRH5 96.25/97.75 call spds 13.5 vs. 95.395/0.18%

- Block, 7,000 SFRZ5 93.75/94.25/94.75 put flys, 5.0 ref 95.915

- 1,500 0QK4 95.56/95.75 call spds ref 95.645

- Blocks, 8,000 SFRZ4 94.37/94.62/94.87 put flys, 5.5

- 4,500 SFRM4 95.75/96.18call spds

- 2,000 0QZ4 96.37/97.00 call spds bs. 3QZ4 96.50/97.00 call spds

- 2,200 SFRM4 95.62/96.18 call spds ref 94.725

- 1,900 SFRQ4 95.12 calls ref 94.905

- Block, 2,900 SFRZ5 90.00/94.00 put spds, 10.5 ref 95.88

- Block, 2,500 SFRZ4 94.43/94.68 put spds, 3.0 ref 95.15

- Treasury Options:

- +15,000 TYN4 107.5 puts, 28 ref 109-02

- 9,900 TYU4 113.5 calls, 20 ref 109-04.5 to -03

- Block, 10,000 TYU4 114 calls, 17 ref 109-04.5

- 1,400 TYM4 108/110 call spds, 59 ref 108-31

- 1,300 FVM4 104.75 puts ref 105-21.5

EGBS: Higher on the day, despite moving off the highs in the afternoon

- There have been little in the way of major talking points for EGBs today, but we have still seen an 89 tick range for Bund futures, which breached Friday's intraday high of 131.57 to trade as high as 131.63 before paring some of these gains as North America came online, and Bund futures drifted lower with USTs to currently be trading around 131.30 at the time of writing.

- This range on futures saw 10-year Bund yields at one point 5.6bp below Friday's closing levels, before retracing around half of the early move to see 10-year Bund yields around 2.7bp lower going into the cash close. There has also been a flattening of the German curve with 2s10s around 1.6bp flatter on the day.

- Spreads across Europe have widened a little today - with French spreads only 0.4bp wider, most other semi-cores and peripheral spreads around 0.7-0.9bp wider on the day, with the exception of Spain where spreads are 1.4bp wider on the day at the time of writing.

- There have been no real major themes driving markets with some mixed-to-slightly positive Eurozone services PMIs this morning having no real market impact.

- Bund futures are up 0.43 today at 131.32 with 10y Bund yields down -2.7bp at 2.467% and Schatz yields down -1.1bp at 2.909%.

- BTP futures are up 0.31 today at 118.07 with 10y yields down -1.5bp at 3.794% and 2y yields down -0.3bp at 3.400%.

- OAT futures are up 0.40 today at 126.54 with 10y yields down -2.2bp at 2.950% and 2y yields down -1.0bp at 2.986%.

FOREX Weaker JPY The Main Feature of Holiday Thinned Monday Trade

- The market focus remained firmly on the Japanese Yen Monday, as holiday thinned trade prompted a fairly subdued session for G10 currencies.

- USDJPY rallied from a 152.78 low on the open to session highs of 154.01 ahead of the European open. Slightly lower core yields prompted a brief reversal to 153.42 as US trade began, however, USDJPY’s upside bias then took over for the remainder of the session, leaving the pair over half a percent stronger on the day.

- The pair has extended its post-NFP bounce, rallying well off the 50-dma - a key support tested Friday at 151.99, closely matching the multi-decade pivot level around 151.91-95, which garnered much attention earlier this year.

- The limited adjustment for US yields has kept the USD index unchanged Monday, with a higher USDJPY offset by a stronger AUD, EUR and GBP against the greenback, all benefitting from the buoyant price action for major equity indices.

- The firmer AUD comes before the RBA overnight, widely expected to leave rates at 4.35% at its May decision. AUDUSD traded firmly higher Friday and in the process breached resistance at 0.6587, the Apr 29 high. The break of this hurdle cancels a recent bearish threat and highlights a resumption of the bull leg that started Apr 19. This initially opens 0.6668, the Mar 8 high.

- Late headlines on Hamas potentially agreeing to a cease-fire placed downward pressure on USDILS, trading from around 3.74 to 3.70. The pair currently trades around 3.7150 as Israel are said to be studying the update proposal.

Late Equities Roundup: Extending Highs: IT & Energy Sectors Still LEading

- Stocks continue to extend late session highs, semiconductor stocks taking the lead in late trade. S&P Eminis are trading through technical resistance of 5192.16 (61.8% retracement of the Apr 1 - 19 bear leg) to 5199.50 -- April 15 highs, currently trades up 40.25 points (0.78%) at 5195.25, DJIA is up 158.35 points (0.41%) at 38835.29, Nasdaq up 140 points (0.9%) at 16295.83.

- Leading gainers: Information Technology and Energy sectors continue to outperform in late trade where chip stocks continued to buoy the IT sector: Micron +4.39%, Nvidia +3.36%, Monolithic Power +3.03%. Oil and gas shares supported the Energy sector as crude prices held modest gains (WTI +0.29 at 78.40): APA Corp +1.93%, Marathon Oil +1.69%, Diamondback Energy +1.54%.

- Laggers: Consumer Staples and Real Estate sectors continued to underperform in late trade, personal products shares weighed on Staples: carry-over selling for Estee Lauder -2.12%, Kenvue -0.96%, Kimberly-Clark -0.57%. Meanwhile, investment trusts weighed on the latter, particularly specialized and industrial REITS: Digital Realty -1.99%, Crown Castle -1.98%, American Tower -2.11%.

- Salient earnings announcement expected after today's close: Spirit Airlines, Tyson Foods, JELD-WEN, Realty Income, Williams Cos, Primerica, Simon Property Goodyear Tire, Vertex, Microchip Technology. Early Tuesday: Rockwell Automation, Duke Energy.

E-MINI S&P TECHS: (M4) Has Traded Through The 20-Day EMA

- RES 4: 5333.50 High Apr 1 and the bull trigger

- RES 3: 5285.00 High Apr 10

- RES 2: 5246.18 76.4% retracement of the Apr 1 - 19 bear leg

- RES 1: 5199.50 Intra day high May 6

- PRICE: 5195.00 @ 1450 ET May 6

- SUP 1: 5036.25/4963.50 Low May 2 / 19 and the bear trigger

- SUP 2: 4907.57 50.0% retracement of the Oct 27 ‘23 - Apr 1 bull leg

- SUP 3: 4863.75 Low Jan 19

- SUP 4: 4799.50 Low Jan 17

The short-term trend condition in S&P E-Minis remains bearish and recent gains appear to be a correction. A resumption of the bear leg would open 4907.57, a Fibonacci retracement. The contract has traded through resistance at the 20-day EMA, at 5124.14. A clear breach and a continuation higher would instead signal a possible reversal and expose key resistance at 5333.50, Apr 1 high. Initial resistance is 5192.16, a Fibonacci retracement.

COMMODITIES

- WTI Crude Oil (front-month) up $0.45 (0.58%) at $78.57

- Gold is up $22.21 (0.96%) at $2323.90

TUESADAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/05/2024 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 07/05/2024 | 0030/1030 | *** |  | AU | Retail trade quarterly |

| 07/05/2024 | 0430/1430 | *** | | AU | RBA Rate Decision |

| 07/05/2024 | 0545/0745 | ** |  | CH | Unemployment |

| 07/05/2024 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 07/05/2024 | 0600/0800 | ** | | DE | Trade Balance |

| 07/05/2024 | 0645/0845 | * |  | FR | Foreign Trade |

| 07/05/2024 | 0730/0930 | ** |  | EU | S&P Global Final Eurozone Construction PMI |

| 07/05/2024 | 0830/0930 | ** | | UK | S&P Global/CIPS Construction PMI |

| 07/05/2024 | 0900/1100 | ** | | EU | Retail Sales |

| 07/05/2024 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 07/05/2024 | 1400/1000 | * |  | CA | Ivey PMI |

| 07/05/2024 | 1530/1130 | | US | Minneapolis Fed's Neel Kashkari | |

| 07/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 07/05/2024 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 07/05/2024 | 1900/1500 | * | | US | Consumer Credit |

| 07/05/2024 | 1930/1530 | | CA | BOC Sr Deputy Rogers at House Public Accounts committee (no text) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.