Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI ISM Service Survey Builds On Initial NFP Fade

- MNI WHITE HOUSE: OMB Director-'Not Optimistic' On Deal To Avert Partial Shutdown

- MNI MIDEAST: Hezbollah Head Again Warns Of Escalation But Holds Back From War

- MNI US-CHINA: AXIOS: Biden Admin To Keep Trump-Era 301 Tariffs In Place

- ECONOMIC COUNCIL DIR BRAINARD: SUPPLY CHAIN PRESSURES DROPPED TO PRE-PANDEMIC LEVELS, CNBC

- BRAINARD: WAGES GREW OVER 2023 AS CORE INFLATION CAME DOWN, CNBC

- BRAINARD: JOBS REPORT SHOWS A 'VERY HEALTHY ECONOMIC PICTURE', CNBC

- MNI: BAKER HUGHES US RIG COUNT 621; OIL RIGS 501; GAS RIGS 118

Key Links:MNI DATA: December NFP Beat Again Offset By Downward Revisions / MNI US DATA: Worst ISM Services Employment Since Jul 2020 Consistent With Recession / MNI US DATA: Relationship Between ISM Employment and Payrolls Called Further Into Question / MNI INTERVIEW: ISM Chief Sees Bumpy Start To 2024 For Services / MNI GLOBAL WEEK AHEAD - US CPI Highlights Agenda

Markets Roundup: Tsys Weaker After Noisy Dec NFP, Weak ISM Discounted

- Treasury futures holding weaker after the bell, near the middle of a wide session range following this mornings headline NFP data. Mar'24 10Y futures -11 at 111-20.5 vs. 111-06.5 low; curves steeper: 3M10Y +6.503 at -133.760, 2Y10Y +4.017 at -34.770.

- Deemed "noisy", the higher than expected jobs gain was tempered by down revisions for the two prior releases (Dec jobs gain of 216k vs. 175k est, prior down-revised to 173k from 199k).

- Coupled with lower than expected ISM services data (50.6 vs. 52.5 est), ISM Services Employment (43.3 vs. 51.0 est) and Services New Orders (52.8 vs. 56.1 est) underlying rates gapped higher (10Y yield fell to 3.9513% low from 4.0971% high). Support gradually evaporated through midday with underlying futures holding weaker into the close with 10Y yield at 4.0476% (+.0489%).

- The vast U.S. services sector is set to sustain modest growth in coming months despite a surprisingly poor end to last year, with possible Federal Reserve rate cuts helping to stimulate demand later in the year, Institute for Supply Management chair Anthony Nieves told MNI Friday.

- Traders tentative as they await next week's CPI and PPI inflation measures on Thursday and Friday respectively.

FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00447 to 5.33924 (-0.01448/wk)

- 3M -0.00005 to 5.32926 (-0.00214/wk)

- 6M +0.01476 to 5.19284 (+0.02036/wk)

- 12M +0.03521 to 4.85450 (+0.08352/wk)

- Secured Overnight Financing Rate (SOFR): 5.32% (-0.07), volume: $1.930T

- Broad General Collateral Rate (BGCR): 5.31% (-0.02), volume: $681B

- Tri-Party General Collateral Rate (TGCR): 5.31% (-0.02), volume: $672B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $86B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $245B

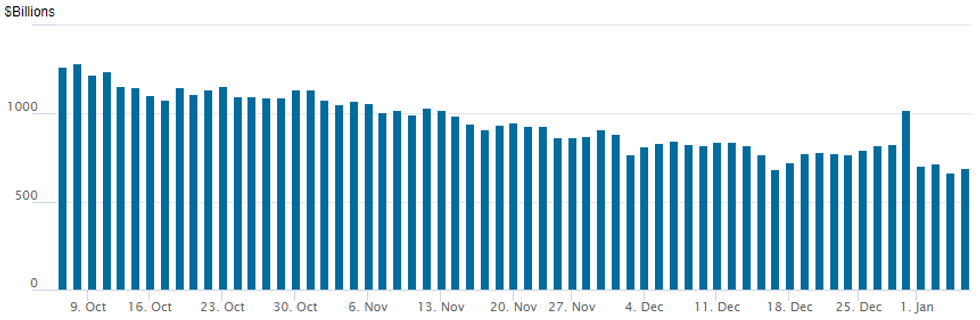

FED REVERSE REPO OPERATION: Rebound

NY Federal Reserve/MNI

- RRP usage rebounds to $694.478B vs. $664.899B yesterday -- the lowest level since mid-June 2021, compares to last Friday's move over $1T: $1,018.483B.

- The number of counterparties rebounds to 83 vs. 78 yesterday, the lowest since April 2022.

SOFR/TREASURY OPTION SUMMARY

FI options saw mixed trade on net amid heavier volumes following this morning's headline employment data for December. Deemed "noisy", the higher than expected jobs gain was tempered by down revisions for the two prior releases, that coupled with lower than expected ISM services data saw underlying rates gap higher (10Y yield fell to 3.9513% low from 4.0971% high). Support gradually evaporated through midday with underlying futures holding weaker into the close. That set the stage for varied option trades listed below where bullish rate cut hedging appeared to lead. Larger put structures reported were largely unwinds or curve related. Traders remained tentative as they await next week's CPI and PPI inflation measures on Thursday and Friday respectively.- SOFR Options:

- +10,000 SFRJ4 95.50/95.62/95.75/95.87 call condors, 1.5 vs. 95.35/0.10%

- over 12,000 SFRH4 95.00 calls, 8.0 last ref 94.94

- Block, 5,000 SFRJ4 94.87/95.06 put spreads 4.0 ref 95.355

- Update -25,000 SFRH5 95.50/96.50 put spds vs. SFRH5 96.50/97.50 call spds, 70.0 net cr/iron fly

- over 18,000 SFRH4 94.62 puts, .5

- 4,200 SFRM4 92.75 puts, cab

- +25,000 SFRM4 95.43/95.68/95.93/96.18 call condors, 4.5

- +40,000 SFRM4/SFRZ4 94.62/94.75 put spd spd, 0.0/Jun over, flattener

- Block/total +15,000 SFRM4 93.50/94.00/94.50 put flys, 1.0

- 7,600 SFRH4 94.00/94.37 put spds, ref 95.91

- Block, 10,000 SFRM4 93.50/94.00/94.50 put flys, 1.0 vs. 95.285/0.05%

- 5,800 SFRG4 94.87/95.00 call spds vs. SFRH4 94.93/95.06 call spds

- 2,500 0QF4 96.37/96.50/96.56 broken call flys ref 96.31

- 1,500 SFRH4 94.75/94.81 2x1 put spds ref 94.905

- 1,500 0QH4 96.06/96.31/96.43 put trees ref 96.315

- 2,000 SFRJ4 94.56/94.68 put spds ref 95.30

- 2,000 SFRJ4 95.37/95.62/96.00/96.25 call condors ref 95.30

- 3,000 SFRH4 95.87/96.00 call spds vs. 2QH4 97.12 calls

- Treasury Options:

- over 10,000 TYH4 111.5 calls, 120

- appr 30,000 wk2 10Y 110.25 puts, 3

- -24,000 TYH4 109 puts, 14 ref 112-06.5, total volume over 37k

- +17,000 FVH4 109/110/111 call flys, 6.5 ref 107-26.5 to -25.75

- over 20,500 TYG4 111.5 puts, 48-49

- over 30,000 TYG4 110 puts mostly 15 ref 111-22.5

- 4,000 FVH4 107.25/107.5/107.75 put flys, ref 107-28

- over 7,500 TYG4 109.5/110/111/111.5 put condors ref 111-20.5

- Block, 5,000 TUH4 101.87/102.25/102.5/102.75 broken put condors, 1 net ref 102-18.5

- 2,500 TYH4 108/109/110.5 put trees ref 111-25.5

- 6,000 TYH4 109/110 put spds, 13 ref 111-26

- 1,700 TYG4 112/TYH4 111.5 call diagonal spds ref 111-28.5

- over 5,400 wk1 FV 107.75 puts, 7 last ref 108-01.75

- 3,000 TYG4 110/111 put spds vs. TYG4 113/114 call spds, 1 net/put spd over ref 111-30.5 to -29.5

EGBs-GILTS CASH CLOSE: Weaker, But Off Worst Levels

European core FI closed Friday weaker but well off the session's worst levels, as US data dictated price action.

- At the outset of Friday's session, Gilts and Bunds resumed their recent negative price action.

- Eurozone Dec flash inflation came in line with expectations, both coming into the week and after Thursday's French and German data (our Eurozone Inflation Insight is here). That translated into a muted market reaction, setting the stage for US data to drive price action for the rest of the day.

- A surprisingly high payrolls gain in December's US employment report initially spurred a global rates sell-off in early afternoon.

- But that would prove the low point for the day: the move fully reversed and then some as the underlying details appeared softer. A very weak ISM Services report in mid-afternoon accelerated the rally.

- Gilts underperformed Bunds, with the belly proving the weakest point on both curves for yet another session. Periphery EGB spreads widened slightly though were briefly tighter in the immediate aftermath of the US ISM data.

- Next week starts with EU (and potential EFSF) supply on Monday, along with German factory orders. and eurozone retail sales/confidence surveys.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.5bps at 2.568%, 5-Yr is up 3.8bps at 2.102%, 10-Yr is up 3.2bps at 2.156%, and 30-Yr is up 2.6bps at 2.376%.

- UK: The 2-Yr yield is up 4.6bps at 4.242%, 5-Yr is up 6.9bps at 3.756%, 10-Yr is up 6bps at 3.787%, and 30-Yr is up 3.4bps at 4.396%.

- Italian BTP spread up 0.4bps at 169.5bps / Greek up 3.5bps at 116.8bps

EGB Options: Limited German Trade To Close Otherwise Busy Week

Friday's Europe rates/bond options flow included:

- DUG4 105.90p, bought for 10 in 10k

- OEH4 119.50/120.50cs, bought for 22 in 7k

FOREX Significant Greenback Swings Amid Nuanced US Data

- Expectations for heightened volatility surrounding the releases of both US employment and ISM Services data were fully justified, with some significant two-way flows for the greenback on Friday. Despite the USD index remaining close to unchanged on the session, the DXY exhibited an impressive 1.2% intra-day range.

- Broad greenback strength was seen as the with AHE and headline NFP dynamics biased markets in that direction. However, delving deeper into the figures significantly took the shine off the report, prompting a sharp reversal. This ensuing turnaround was then exacerbated by a lower-than-expected ISM Services Index and a particularly weak employment component.

- The price action is perhaps best emphasised by movements in USDJPY, whose sensitivity to major US data was amplified once more. The pair continued to take advantage of a change in sentiment in 2024 during the morning session, rising back above 145.00 where it consolidated before the data.

- Following the payrolls release, USDJPY traded as high as 145.97, an impressive 3.66% above the week’s lows. In the aftermath, however, the Japanese Yen recovered well and traded in lockstep with the reversal lower for US yields. Eventually, USDJPY hit a session low of 143.81 as short-term positioning was squeezed in the aftermath of the ISM Services figure. The pair rose around one big figure into the weekend close.

- In G10, GBP was a marginal relative outperformer on the session and EUR sentiment remained a touch bearish. The developments were well received by emerging market currencies, with the likes of MXN and BRL rising around 0.5% on Friday.

- German factory orders and Swiss inflation data kick things off next Monday, however, the focus on the docket will be Thursday’s release of US CPI.

Expiries for Jan08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1130-45(E943mln)

- USD/JPY: Y144.46-55($560mln)

- AUD/USD: $0.6620-40(A$1.1bln), $0.6725(A$633mln)

Late Equity Roundup: Modest Gains Led By Banks, Broadline Retailers

- Stocks are drifting mildly higher after scaling back midday gains, Financial and Consumer Discretionary sectors outperforming in late trade. Early two-tier recovery: stocks had opened weaker but bounced after "noisy" NFP and ISM data. At the moment: DJIA is 11.14 points (0.03%) at 37453.29, S&P E-Mini futures up 4.25 points (0.09%) at 4733.25, Nasdaq up 16.6 points (0.1%) at 14527.85.

- Leading gainers: Banks supported Financials for the second day running: Citizens Financial +3.19%, Comerica +3.11%, Fifth Third Bancorp +3.05%. Reminder, banks lead the next quarterly earnings cycle that starts next week Friday with BlackRock, Bank of America, Wells Fargo, JPMorgan, Citigroup and Bank of NY Mellon.

- Meanwhile, Consumer Discretionary stocks outpaced IT shares in the second half with broadline retailers outperforming: Bath & Body Work +3.61%, CarMax +1.81%, Pool Corp +1.63%.

- Laggers: Consumer Staples and Real Estate sectors continued to lag in the second half, household and personal products weighed on the former: Procter & Gamble -1.06%, Estee Lauder -0.87%, Church and Dwight -0.67%. Estate management shares weighing on the former: CBRE -0.51%, CoStar Group -0.17%,

COMMODITIES Supply Disruptions Head Crude Oil To Weekly Gains

- Crude markets are headed for the US close with 1-2% gains on the day for mixed gains over the holiday-shortened week with WTI outperforming with help from SPR purchase plans.

- Prices remain supported by escalations in the Middle East and supply disruptions from protests at Libya’s oil fields, where oil output has fallen to 981k b/d due to the outage at the Sharara oil field (Bloomberg citing Oil Minister Mohamed Oun).

- US combined oil and gas rig count fell by one on the week to 621 rigs, according to Baker Hughes. This is the second successive on week fall.

- WTI is +2.1% at $73.70 as it pushed closer to resistance at $74.98 (50-day EMA).

- Brent is +1.4% at $78.66 but still a little off a key short-term resistance level at $81.45 (Dec 26 high).

- Gold is +0.1% at $2045.1 after volatility tied to swings in the USD index after mixed data releases for US payrolls and ISM services, driving a daily range of $2024.58-2064.02. The low cleared support at $2040.2 (20-day EMA), with a more pronounced move lower potentially opening $1973.2 (Dec 13 low).

- Weekly moves: WTI +2.7%, Brent +0.3%, Gold -0.9%, US nat gas +12.8%, EU TTF nat gas +4.4%.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/01/2024 | 0700/0800 | ** |  | DE | Trade Balance |

| 08/01/2024 | 0700/0800 | ** | | DE | Manufacturing Orders |

| 08/01/2024 | 0730/0830 | *** |  | CH | CPI |

| 08/01/2024 | 0730/0830 | ** | | CH | Retail Sales |

| 08/01/2024 | 1000/1100 | ** |  | EU | Retail Sales |

| 08/01/2024 | 1630/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 08/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 08/01/2024 | 1730/1230 | | US | Atlanta Fed's Raphael Bostic | |

| 08/01/2024 | 2000/1500 | * | | US | Consumer Credit |

| 09/01/2024 | 2330/0830 | ** |  | JP | Tokyo CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok