Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: GOOLSBEE STILL UNDECIDED ON NEED FOR HIKE AT NEXT MEETING .. FOMC RATE PROJECTION FOR MODEST HIKES IS REASONABLE

- MNI: SENATE BANKING COMMITTEE TO VOTE ON FED NOMINEES JULY 12

- BIDEN: U.S. JOBS REPORT SHOWS 'BIDENOMICS IN ACTION,' CONTINUED GROWTH, Bbg

- POLAND: GLAPINSKI: NO DISCUSSION OF RATE CUTS IN JULY MPC MEETING, Bbg

- CHINA MULLS MORE LOCAL BOND SALES TO HELP PAY RISKY HIDDEN DEBT, Bbg

- U.S. Oil Boom Blunts OPEC's Pricing Power, WSJ

Key Links:MNI INTERVIEW: Resilient Jobs Mean Fed Can Tighten More-Kamin / MNI BRIEF: Fed’s Goolsbee-More Moderate Rate Increases To Come / MNI BRIEF: US Jobs Lowest In 2-1/2 Years, Jobless Rate Dips / MNI GLOBAL WEEK AHEAD: US Inflation Data In Focus

US TSYS Curves Remain Steeper As Bonds Trim Gains Late

- Treasury futures trade mixed after the bell, bonds trimming gains late (USU3 -3 at 116-05 vs. 116-21.5 high) while curves hold steeper but off session highs (2s10s +7.403 at -88.587 vs. -86.662 high). Generally quiet second half.

- Treasury futures gapped higher after smaller than expected at June jobs gain of 209k (cons 230K) and the key initial takeaway is the -110k two-month revision (-33k for May (so still v strong at 306k) and -77k for April).

- Futures had reversed support/traded lower post-data w/ attention on strong labor market, AHE firm at +.4, workweek extended to 34.3 hours should keep the FED on track to hike at the next FOMC meeting on July 26 (92% priced in).

- Weakness was short lived as Treasury futures bounced off session lows, see-sawing back near post-Jobs data highs at the moment as focus turned back to moderating jobs gains (and down-revisions to the two prior releases) ahead of next Wednesday's CPI (MoM 0.3% est vs. 0.1% prior; YoY 3.1% vs. 4.1% prior).

- Projected rate hike(s) receded through year end again: September cumulative of +28.6bp (30.5 high) at 5.360%, November cumulative at 34bp (37.3 high) at 5.415%, December cumulative 29.3bp (34.4 high) at 5.368%. Fed terminal at 5.42% in Nov'23.

- The Federal Reserve may need to tighten monetary policy a little bit further this year but has already done most of the work in raising interest rates to control inflation, Chicago Fed President Austan Goolsbee said Friday. "There are some more moderate increases to come. I'm still undecided" on July, he told CNBC in an interview.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.01222 to 5.17701 (+.03623/wk)

- 3M +0.01757 to 5.29847 (+.03011/wk)

- 6M +0.03354 to 5.41500 (+.03354/wk)

- 12M +0.07632 to 5.45445 (+.05763/wk)

- Daily Effective Fed Funds Rate: 5.08% volume: $119B

- Daily Overnight Bank Funding Rate: 5.07% volume: $269B

- Secured Overnight Financing Rate (SOFR): 5.06%, $1.573T

- Broad General Collateral Rate (BGCR): 5.04%, $583B

- Tri-Party General Collateral Rate (TGCR): 5.04%, $577B

- (rate, volume levels reflect prior session)

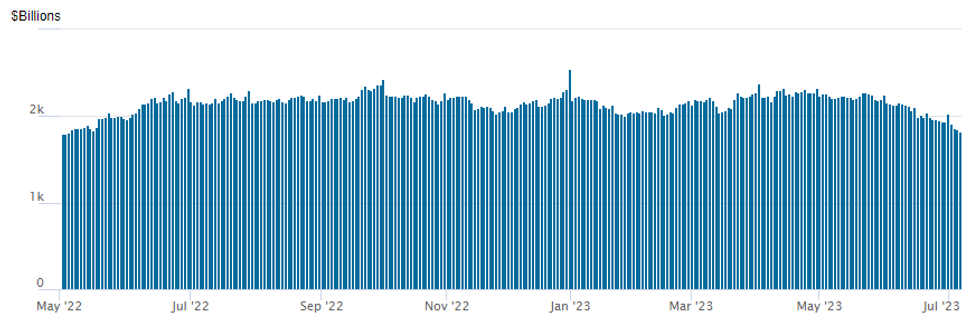

FED REVERSE REPO OPERATION: Continued Decline

NY Federal Reserve/MNI

The deluge in Treasury Bill issuance post debt ceiling postponement continues to sap NY Fed reverse repo usage. Latest operation shows $1,822.303B, lowest since early May'22, w/ 99 counterparties, compared to $1,854.256B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury options leaned toward better put trade on net Friday, carry-over from the overnight session. Upside call structure trade did see a pick-up in buying from late morning on as the underlying futures climbed back near post-jobs data highs. Translation: option accounts favored downside puts as expectations of a 25bp rate hike on July 26 remained high (over 91%). Moderating jobs data that spurred the rebound in rates triggered the pick-up in call buying as further rate hike pricing by year end receded.

- SOFR Options:

- 6,500 SFRU3 99.37/99.75 put spds ref 94.58

- 5,275 SFRZ3 94.56/95.00/95.50 broken call flys

- Block, 10,000 SFRZ3 98.50/97.50 call spds, 1.25 on splits vs. 94.64

- Block/screen, 16,500 SFRU3 94.00/94.50 put spds 7.5-7.25 vs 94.58/0.38%

- 1,000 SFRN3 94.56/94.62/94.68 call flys ref 94.57

- 1,000 OQN3 95.50/96.00 put spds vs. 2QN3 96.56 puts

- 4,000 SFRU3 94.25/94.37/94.50 put flys ref 94.58

- 2,000 SFRV3 94.25/94.50 2x1 put spds 3.5 ref 94.58

- 2,000 SFRZ3 94.18/94.50/94.81 put flys ref 94.575

- 1,000 2QU3 96.75/97.00 call spds ref 96.16

- Treasury Options:

- 3,000 TYQ 113 calls, 3 over TYQ 108.5/109 put spds ref 110-22

- 2,500 FVU3 106/107/107.5/108.5 call condors ref 106-10.75

- 4,500 TYU3107/107.5/111.5 broken put trees, 103 net ref 110-22

- Update, over 16,000 TYU3 111 puts, 143-127 ref 110-19.5 to -23

- over 6,000 TYQ3 112.5/113.5 call spds, 3 ref 110-19

- 5,000 TYU3 111 puts, 143 ref 110-19.5

- 5,000 TYQ3 109.75 puts, 23 ref 110-19

- 2,800 TYU3 113 calls, 28 ref 110-16.5

- over 3,000 TYQ3 109/110 put spds ref 110-18 to -21

- -6,000 USU3 116/118/120/122 put condors, 25 ref 123-27

- +2,500 TYU3 112.5/114.5/115.5 1x3x2 broken call flys ref 110-15, 12

- 1,000 FVQ3 105/105.5/106 put flys ref 106-01.5

- 2,000 TYQ3 112/112.5 call spds, 6 ref 110-16.5

- 6,500 TYQ3 109 puts, 13-14 ref 110-22 to -17.5

- 1,000 FVU3 103.5/105 put spds ref 106-05

- 2,750 FVQ 104.75 puts ref 106-04.75

- 1,000 FVQ3 107.75/108.75 call spds ref 106-03.75

FOREX Greenback Sinks as NFP Falls Short of Heightened Expectations

- The June payrolls report disappointed those that had upped their expectations after a blowout ADP report just one day prior. Headline payrolls added 209k jobs across June, the lowest in over three years, and a solid revision lower for the May release also dampened the strength of the report.

- While the unemployment rate fell, markets marked down the pricing of the Fed tightening cycle this year, There continues to be circa 21-22bp priced for the Jul 26 decision, with the cumulative +35bp of hikes to a terminal of 5.43% in November trimmed slightly. Cuts into 2024 widened on the day, building to 55bps to Jun'24 and 125bp to Dec'24.

- This, allied with a pullback in the longer-end worked against the USD, which slipped against all others in G10.

- The USD Index made a convicing break through the 50-dma, hitting the lowest levels since late June to narrow the gap with key support at the mid-June low of 101.921. The JPY was one of the primary beneficiaries, pressuring USD/JPY to erase the entirety of the rally posted since Jun23.

- NOK performed well, rising against most others on the back of a bounce in risk as well as a rebound in the oil price. Moves in the NOK shrugged off near-term weakness evident in poor industrial production figures for May, turning focus to next week's CPI.

- US inflation takes primacy in the coming week, with markets expecting M/M headline and core to be propped up to 0.3%, but for Y/Y to post another sequential slowdown to 3.1% and 5.0% for headline and core respectively.

FX Expiries for Jul10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0800(E856mln), $1.0845-65(E752mln), $1.0920(E1.1bln), $1.0975-80(E1.3bln), $1.1000(E676mln)

- USD/JPY: Y140.00($876mln), Y143.00($1.0bln)

- GBP/USD: $1.2765-70(Gbp584mln)

- AUD/USD: $0.6685(A$895mln), $0.6700-20(A$576mln)

- USD/CNY: Cny7.2600($566mln)

Equities Roundup: Energy Sector Shares Lead Rally

- Off post-data lows, stocks are trading at/near recent session highs, risk appetite slightly improved as focus turns back to moderating jobs gains (and down-revisions to the two prior releases) ahead of next Wednesday's CPI (MoM 0.3% est vs. 0.1% prior; YoY 3.1% vs. 4.1% prior).

- Currently, DJIA is up 103.29 points (0.3%) at 34025.82, S&P E-Mini Future up 27.5 points (0.62%) at 4474.5, Nasdaq up 116 points (0.8%) at 13794.89.

- Leading gainers: Energy, Materials and Industrials sector shares are outperforming. Oil companies trading strong as prospect of tighter global supplies outweighed concerns about higher interest rates that could dampen global growth and energy demand. Schlumberger +7.5%, Haliburton +6.9%, Marathon Petroleum +4.87%, APA +4.75%. Materials and Industrials made similar gains as crude and Gold prices rebounded (WTI +1.38 at 73.18), Gold +16.0 at 1926.90.

- Laggers: Health Care, Consumer Staples and Utilities sectors underperformed. Pharmaceuticals and biotech shares traded weaker in the second half, Biogen -2.6%, Merck -2.2%, Lilly -1.8%.

- The technical/bull theme in S&P E-minis bull theme remains intact and the pullback this week appears to be a correction - for now. Attention is on the first support 4409.66, the 20-day EMA. Clearance of this level would expose 4368.50, the Jun 26 low and a key support.

- On Monday, the contract pierced key resistance and the bull trigger at 4493.75, the Jun 16 high. A clear breach of this level would confirm a resumption of the uptrend opening 4532.08, a Fibonacci projection.

E-MINI S&P TECHS: (U3) Pullback Considered Corrective

- RES 4: 4556.71 2.382 projection of the May 4 - 19 - 24 price swing

- RES 3: 4552.12 Bull channel top drawn from the Mar 13 low

- RES 2: 4532.08 2.236 projection of the May 4 - 19 - 24 price swing

- RES 1: 4498.00 High Jun 30

- PRICE: 4466.50 @ 1235 ET Jul 7

- SUP 1: 4409.66/4368.50 20-day EMA / Low Jun 26 and a key support

- SUP 2: 4321.67 50-day EMA

- SUP 3: 4310.90 Bull channel base drawn from the Mar 13 low

- SUP 4: 4269.50 Low Jun 2

A bull theme in S&P E-minis remains intact and the pullback this week appears to be a correction - for now. Attention is on the first support 4409.66, the 20-day EMA. Clearance of this level would expose 4368.50, the Jun 26 low and a key support. On Monday, the contract pierced key resistance and the bull trigger at 4493.75, the Jun 16 high. A clear breach of this level would confirm a resumption of the uptrend opening 4532.08, a Fibonacci projection.

COMMODITIES: Brent Nears Bull Trigger And Gold Pushes Higher With USD Tailwind

- Crude oil prices have rebounded to test recent highs and technical resistance with support from a weaker US dollar after the payrolls report and tighter supply concerns.

- Latest on supply: Pipeline damages on Iraq-Turkey export pipeline to the port of Ceyhan are likely the cause for the continued halt in flows, Iraq’s oil minister said. Kazakhstan’s crude production has been recovering after a power outage earlier this week constrained supply.

- WTI is +2.6% at $73.65, clearing $72.72 (Jun 21 high) and eyeing key resistance at $75.70 (Jun 5 high).

- Brent is +2.3% at $78.25, clearing $77.25 and setting its sights on the bull trigger at $78.47 (Jun 5 high).

- Gold is +0.8% at $1926.05, boosted by the aforementioned weaker USD. An earlier high of $1934.71 easily cleared resistance at $1929.1 (20-day EMA) before pulling back, but nevertheless opens $1945.9 (50-day EMA).

- Weekly moves: WTI +5.5%, Brent +4.5%, Gold +0.4%, US nat gas -4.7%, EU TTF nat gas -9.8%

MONDAY/TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/07/2023 | 0730/0830 |  | UK | BOE Bailey Panels Rencontres Economiques | |

| 10/07/2023 | 0130/0930 | *** |  | CN | CPI |

| 10/07/2023 | 0130/0930 | *** | | CN | Producer Price Index |

| 10/07/2023 | 0600/0800 | * |  | NO | CPI Norway |

| 10/07/2023 | - | *** | | CN | Money Supply |

| 10/07/2023 | - | *** | | CN | New Loans |

| 10/07/2023 | - | *** | | CN | Social Financing |

| 10/07/2023 | 1230/0830 | * |  | CA | Building Permits |

| 10/07/2023 | 1400/1000 | ** |  | US | Wholesale Trade |

| 10/07/2023 | 1400/1000 | | US | Fed Vice Chair Michael Barr | |

| 10/07/2023 | 1500/1100 | ** | | US | NY Fed survey of consumer expectations |

| 10/07/2023 | 1500/1100 | | US | Cleveland Fed's Loretta Mester | |

| 10/07/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 10/07/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 10/07/2023 | 1600/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 10/07/2023 | 1900/1500 | * | | US | Consumer Credit |

| 10/07/2023 | 1900/2000 | | UK | BOE Bailey Speech at Financial & Professional Services Dinner |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.