Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- US, CHINA PREPARING TO RESTART MILITARY-TO-MILITARY COMMS, AXIOS

- FED CHAIRMAN POWELL DOES NOT COMMENT ON OUTLOOK FOR FED POLICY OR ECONOMY

- YEMEN SHIITE REBELS SAY US DRONE SHOT DOWN OVER WATER TERRITORY, Bbg

- G7 FOREIGN MINISTERS' STATEMENT: CONDEMN TERROR ATTACKS BY HAMAS AND OTHERS AGAINST ISRAEL, AND ONGOING MISSILE ATTACKS AGAINST ISRAEL, Rtrs

- G7 STATEMENT: EMPHASISE ISRAEL'S RIGHT TO DEFEND ITSELF AND ITS PEOPLE IN ACCORDANCE WITH INTERNATIONAL LAW, Rtrs

Key Links: MNI INTERVIEW: Fed Done Hiking, Eyes Long Hold-Ex-IMF Official / MNI: BOC Minutes Say Some Thought Another Hike Would Be Needed / US Treasury Auction Calendar

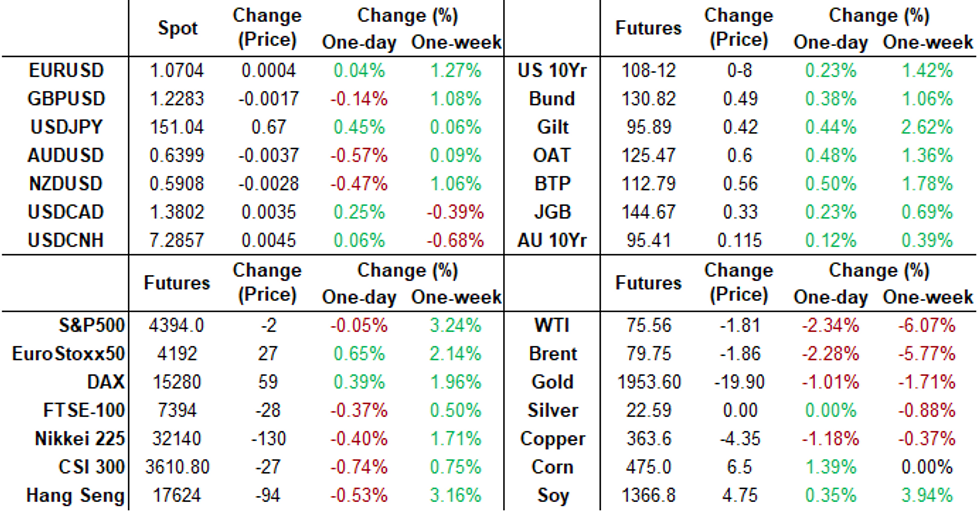

US TSYS Paring Gains, Curves Extend Flatter

- Decent volumes by the close (TYZ3>1.6M contracts) belied a rather muted session Wednesday, Treasury futures near late session highs after the bell, curves flatter with short end rates lagging all day: 3M10Y -5.677 at -92.909, 2Y10Y -6.788 at -42.313.

- Technicals: Dec'23 10Y tap 108-14.5 high +10.5, put focus on initial technical resistance at 108-25 (Nov 3 high). Breach of that level puts focus on 109-20 (Sep 19 high).

- Projected rate cut chance into early 2024 cooled: December holds at 2.4bp at 5.347%, January 2024 cumulative 4.4bp at 5.373%, while March 2024 pricing in -22.3% (-26.1% this morning) chance of a rate cut with cumulative at -1.2bp at 5.317%, May 2024 cumulative -12.5bp at 5.204%. Fed terminal at 5.375% in Feb'24.

- Cross asset summary: West Texas crude WTI -1.80 at 75.57, Gold -20.32 at 1949.13, US$ index DXY +0.037 at 105.579.

- Focus on Thursday Fed-speak. Initially, MNI Webcast hosts Richmond Fed Barkin at 1100ET as he discusses policy, economic outlook. Please register to attend: MNI Webcast.

- Meanwhile, Fed Chairman Powell will attend a moderated discussion at an IMF Conference at 1400ET.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00064 to 5.32133 (-0.00043/wk)

- 3M +0.00341 to 5.36908 (-0.01109/Wk)

- 6M +0.00385 to 5.39707 (-0.02882/wk)

- 12M +0.01328 to 5.27490 (-0.05100/Wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $104B

- Daily Overnight Bank Funding Rate: 5.32% volume: $244B

- Secured Overnight Financing Rate (SOFR): 5.32%, $1.546T

- Broad General Collateral Rate (BGCR): 5.30%, $590B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $576B

- (rate, volume levels reflect prior session)

FED REVERSE REPO OPERATION

The NY Fed Reverse Repo operation usage gains slightly: $1,024.451B w/98 counterparties vs. $1,008.685B in the prior session - the lowest level since August 2021. Today's usage compares to prior two year low of $1,054,986B from Nov 2.

SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option trade segued from better call volume overnight to mixed on net as put buyers and repositioners emerged in the second half. Curves extended flatter with short end rates lagging. Projected rate cut chance into early 2024 cooled: December holds at 2.4bp at 5.347%, January 2024 cumulative 4.4bp at 5.373%, while March 2024 pricing in -22.3% (-26.1% this morning) chance of a rate cut with cumulative at -1.2bp at 5.317%, May 2024 cumulative -12.5bp at 5.204%. Fed terminal at 5.375% in Feb'24.- SOFR Options:

- Block, 10,000 SFRH4 94.56 puts, 9.5 vs. 94.725/0.15%

- -4,000 SFRF4 94.62/94.75 strangles, 20.0

- +10,000 SFRH4 94.75/94.87 call spds, 2.75

- +4,000 0QZ3 95.50/95.75/96.00 call flys, 4.0 vs. 95.60/0.05%

- 2,500 0QZ3 95.43/95.75/96.12 call flys ref 95.56

- 2,000 0QZ3 95.00/95.25/95.50 put flys ref 95.55

- over 5,000 SFRH4 95.75 calls ref 94.725

- 1,200 SFRH4 94.75/95.75/97.00 broken call flys ref 94.725

- 1,000 SFRH4 94.75/95.00/95.25/95.50 call condors

- Treasury Options:

- over -43,000 wkly/Wed 10Y 110 puts 135-138

- over +46,000 wk2 10Y 110 puts, 137-141

- -5,000 wkly/Wed TU 102.12 puts, 40.5-41

- +5,000 wk2 TU 101.87 puts, 26

- -9,000 TYZ3 106/107 put spds, 8

- +6,000 FVZ3 104 puts, 3

- 5,000 wk2 TY 108.25/108.75 call spds, 5 ref 108-04

- 10,000 TYH4 108/111/114 call flys ref 108-10.5

- 2,000 FVZ3 102 puts, .5 ref 105-14

- 1,600 TYZ3 108.5/109.5/110 broken call flys ref 107-31

- 1,800 FVZ3 106/107/107.5 broken call flys, ref 105-13

EGBs-GILTS CASH CLOSE: Long End Impresses Again

The long ends of the UK and German curves rallied for the 2nd consecutive session Wednesday. Once again the 30Y segment was a standout, with yields at that tenor pushing to the lowest levels since September.

- While short-end/bellies were relatively inert, including weakness in Schatz and almost no change in Bobl - ECB and BoE hike prospects were little changed - 2Y and 5Y UK yields edged incrementally to fresh post-Jun lows.

- There were almost no macro catalysts of note during the session, with the highlight being a jump in 1Y consumer inflation expectations in the ECB's CES survey that brought core FI down from morning highs.

- Central bank speakers attempted to push back on recent rate cut talk, including ECB's Makhlouf ('far too early in my view' to discuss cuts) and Nagel (the 'last mile' may well be the hardest), as well as BoE's Bailey ('really too early to be talking about cutting rates'). but this had little discernable impact.

- Instead it was a continued march lower in oil prices, a pullback in equities, and a general resumption of the trend begun last week post-US Fed decision / jobs report that saw long-end European FI rally.

- Periphery spreads tightened, led by Italy, while PGBs lagged as political uncertainty continued to drag.

- Following on from the US 10Y Treasury auction after the cash close Wednesday, a limited docket awaits Thursday, with the ECB's economic bulletin and multiple speakers (Villeroy, Lane, Lagarde, BoE's Pill) ahead.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.1bps at 3.015%, 5-Yr is down 0.8bps at 2.569%, 10-Yr is down 4.1bps at 2.617%, and 30-Yr is down 8.1bps at 2.813%.

- UK: The 2-Yr yield is down 1.2bps at 4.62%, 5-Yr is down 0.2bps at 4.242%, 10-Yr is down 3bps at 4.24%, and 30-Yr is down 4.6bps at 4.691%.

- Italian BTP spread down 2.9bps at 186.3bps / Portuguese up 1.1bps at 74.5bps

EGB Options: Limited Rates Trade Wednesday

Wednesday's Europe rates/bond options flow included:

- ERF4 96.00/96.12/96.25c fly vs 95.875p, bought the put for 4 in 7.2k

- ERH4 96.25/96.12ps 1x2. Bought for 1.5 in 3k

FOREX EURJPY Rises 0.45%, Extending To Multi-Year Highs Above 161.00

- Early greenback strength saw the USD index rise around 0.35%, briefly reversing the entirety of the post-NFP sell-off. However, the move lower for US yields in a flattening move prompted some renewed dollar weakness which has seen the USD index slip into negative territory approaching the APAC crossover.

- However, further weakness for crude futures amid a bearish demand outlook has continued to weigh on the likes of AUD and NZD, the clear underperformers in G10 alongside the Japanese Yen.

- USDJPY has been steadily grinding higher over the course of the session, with the pair probing the 1.51 handle heading into late US trade. The trend needle in USDJPY continues to point north. Last week’s gains resulted in a breach of 150.78, the Oct 26 high. This confirmed a resumption of the uptrend and has opened 152.20, a Fibonacci projection. Moving average studies are in a bull-mode position, reflecting the market's positive sentiment. Indeed, a solid bounce for the Euro across US hours has seen EURJPY extend the long-standing uptrend, gaining momentum above 161.00 and continuing to eat in to the steep 2008 sell-off. 161.52, a Fibonacci projection, has been pierced today which paves the way for further strength to 162.00 and 162.80, the 1.00 projection of the Jul 28 - Aug 30 - Oct 3 price swing.

- EURUSD found support once more around 1.0660 on Wednesday. The low today was just 4-pips shy of pre-NFP levels at 1.0655, before the pair registered a not-insignificant recovery that brings the pair back above 1.0700. The current bullish condition in EURUSD remains intact and this week’s pullback is considered technically corrective.

- Commodity weakness provided a more notable decline for some emerging market currencies on Wednesday, with punchy moves for the likes of USDCLP (+1.90%) and USDCOP (+1.60%) and a 0.80% advance for USDZAR.

- Chinese CPI/PPI overnight marks the highlight for the APAC session where the market consensus is for headline CPI to dip back into negative territory. US Jobless claims and central bank speakers will dominate the rest of Thursday’s calendar.

FX Expiries for Nov09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600-20($2.0bln), $1.0700(E1.8bln)

- USD/JPY: Y150.00($2.8bln), Y151.00($1.1bln), Y152.00($515mln)

- EUR/JPY: Y156.00(E560mln)

- EUR/GBP: Gbp0.8745-50(E738mln)

- AUD/USD: $0.6450-60(A$2.0bln), $0.6500-10(A$1.0bln)

- USD/CNY: Cny7.2850($1.3bln), Cny7.3500($1.7bln)

Late Equity Roundup: Off Lows, IT, REITS Outperform

- Stocks have climbed off moderate midday lows, near the middle of a narrow session range after the bell. Currently, S&P E-Mini future are down 0.5 points (-0.01%) at 4395.75, Nasdaq up 5.7 points (0%) at 13646.43, DJIA down 77.01 points (-0.23%) at 34076.16.

- Initial technical support for Eminis is well below: 4157.75/4122.25 Low Nov 3 / Low Oct 27 and the bear trigger. initial technical resistance of 4407.75 (intraday high) is followed by 4430.50 (High Oct 12).

- Laggers: Electricity providers continued to weigh on Utilities: Pinnacle West -2.44%, NextEra -2.07%, PPL -2.05%. Meanwhile, oil and gas shares weighed on the Energy sector: APA -3.1%, Devon Energy -2.67%, Marathon Oil -2.55%.

- Leaders: Information Technology and Real Estate sectors continue to outperform, software names and chip stocks buoyed the IT sector for the second consecutive day: Nvidia +1.77%, Applied Materials +1.63%, Fortinet +2.67%, Oracle +2.44%. Meanwhile, residential and industrial real estate investment trusts (REITS) buoying the former: UDR +1.34%, Camden Property +1.27%, Prologis +0.82%.

- Note: Corporate earnings after the close: Twilio Inc, Duolingo Inc, Take-Two Interactive Software, Corteva, MGM Resorts, Lyft, AMC Entertainment, HubSpot, Enviva, AppLovin Corp, Viasat, Beyond Meat, Callaway Brands Corp, Marathon Digital Holdings.

E-MINI S&P TECHS: (Z3) Approaching Trendline Resistance

- RES 4: 4538.88 High Sep 20

- RES 3: 4442.25 Trendline resistance drawn from the Jul 27 high

- RES 2: 4430.50 High Oct 12

- RES 1: 4407.75 Intraday high

- PRICE: 4394.75 @ 1455 ET Nov 8

- SUP 1: 4257.75/4122.25 Low Nov 3 / Low Oct 27 and the bear trigger

- SUP 2: 4100.00 Round number support 4124.19

- SUP 3: 4090.35 1.764 proj of the Jul 27 - Aug 18 - Sep 1 price swing

- SUP 4: 4049.00 Low Mar 28

S&P e-minis traded higher last week and the contract maintains a firm short-term tone. The latest recovery still appears to be a correction, however, price has cleared the 20- and 50-day EMAs. The break of the 50-day average - a key short-term pivot level - has strengthened bullish conditions. Sights are on 4430.50, the Oct 12 high and 4442.25, trendline resistance drawn from the Jul 27 high. Key support and the bear trigger is at 4122.25, the Oct 27 low.

COMMODITIES WTI Slides To Mid-July Levels, Gold Through Latest Support

- Crude prices have seen another heavy decline today with Brent clearing $80/bbl and WTI seeing its lowest close since the middle of July after a bearish demand outlook weighs further on prices. A slightly stronger dollar and a possible further relaxation in Russia’s export ban of some products is adding further downside.

- API weekly oil stock data: Crude +11.9mbbl, Cushing +1.1mbbl, Gasoline -0.4mbbl, Distillate +1mbbl

- ARA crude inventories rose 175k bbl or 0.4% in the week ended Nov 3 to 49mn bbls according to Genscape.

- The US could reimpose energy sanctions on Venezuela if commitments towards free elections and the release of more political prisoners are not met by 30 November according to White House senior adviser Juan Gonzales.

- WTI is -2.75% at $75.24, pushing towards new support at $74.26 (61.8% retrace of the May 4 – Sep 28 bull run)

- Brent is -2.6% at $79.45, through $81.02 (Aug 24 low) and next eyeing $78.89 (61.8% retrace of May 4 – Sep 28 bull run).

- Gold is -1.0% at $1949.55 with much of its moving coming earlier in the session as the USD modestly extended previous notable strength before some additional downward pressure after the Israel Army said Gazans are able to move south in limited pauses and they can also leave north of the strip on Thursday. It has pushed through $1956.8 (Nov 7 low) to open $1936.6 (50-day EMA).

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/11/2023 | 0130/0930 | *** |  | CN | CPI |

| 09/11/2023 | 0130/0930 | *** | | CN | Producer Price Index |

| 09/11/2023 | 0810/0910 |  | EU | ECB's Lane remarks at ECB conference | |

| 09/11/2023 | 0830/0830 |  | UK | BOE's Pill speaks at ICAEW UK Regions Economic Summit | |

| 09/11/2023 | 1330/0830 | *** |  | US | Jobless Claims |

| 09/11/2023 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 09/11/2023 | 1430/0930 | | US | Fed's Raphael Bostic and Tom Barkin | |

| 09/11/2023 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 09/11/2023 | 1600/1100 | | US | MNI Webcast with Fed's Tom Barkin | |

| 09/11/2023 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 09/11/2023 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 09/11/2023 | 1645/1145 |  | CA | BOC Sr Deputy Rogers speech | |

| 09/11/2023 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 09/11/2023 | 1800/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 09/11/2023 | 1900/1400 | | US | Fed Chair Jerome Powell |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.