Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI BOC: 'OUR 2% TARGET IS NOW IN SIGHT' BUT PROGRESS SLOW

- MNI BOC: REITERATES PREPARED TO HIKE RATES AGAIN IF NEEDED

- FORD FAST TRACKS PAY BOOST FOR 8,000 UAW EMPLOYEES, Bbg

- FDIC SAYS BANK PROFITS FELL SEQUENTIALLY, ROSE YEAR OVER YEAR, Bbg

- FDIC SAYS BANK DEPOSITS FELL FIVE CONSECUTIVE QUARTERS, Bbg

Key Links: MNI INTERVIEW: Reserve Scarcity Yet To Materialize - Fed Econ / MNI:BOC Balancing Risk Of Over-Tightening, CPI Target In Sight / US Treasury Auction Calendar / US$ Credit Supply Pipeline

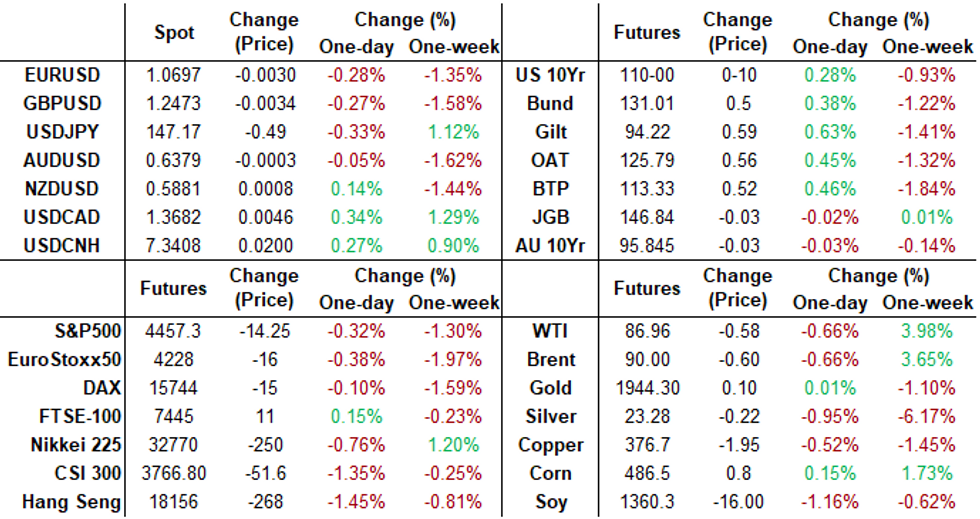

US TSY Rates Shrug Off Lower Than Expected Weekly Claims

- Treasury futures are drifting near late session highs after the bell, Dec'23 10Y futures currently at 109-31.5 (+9.5) are back near Wednesday's pre-ISM Services data highs. Curves bear steepening with long end rates lagging, 2Y10Y at -69.524 +4.755.

- Treasury futures had sold off after Initial Jobless Claims comes out lower than expected (216k, 234k est), Continuing Claims added to the healthier than expected data, falling to 1679k (cons 1719k) from a downward revised 1719k (initial 1725k). It falls back below the 2019 average, tying with mid-July levels having last been lower in January.

- Meanwhile, Unit Labor Costs higher than expected at 2.2% vs. 1.9% est, Nonfarm Productivity near in-line at 3.5% vs. 3.4% est.

- Market participation has been relatively thin, however, as evidenced by a rebound in German bunds this morning that carried over into US markets at midmorning.

- Fed speak resumes this afternoon, the StL Fed will hold a forum on the search for bank president at 1400ET. NY Fed Williams partaking in a Bbg moderated market discussion at 1530ET, Atl Fed Bostic economic outlook, livestreamed at 1545ET, Fed Gov Bowman on future of money at 1655ET.

- This evening, Atlanta Fed Bostic speaks about economic mobility at 1900ET, while Dallas Fed Logan discusses policy at Southern Methodist University (text, no Q&A) at 1905ET.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00249 to 5.32933 (+.00046/wk)

- 3M +0.01326 to 5.41099 (+0.00869/wk)

- 6M +0.02329 to 5.47601 (+0.02277/wk)

- 12M +0.04377 to 5.43272 (+0.06406/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $100B

- Daily Overnight Bank Funding Rate: 5.32% volume: $250B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.391T

- Broad General Collateral Rate (BGCR): 5.30%, $552B

- Tri-Party General Collateral Rate (TGCR): 5.29%, $543B

- (rate, volume levels reflect prior session)

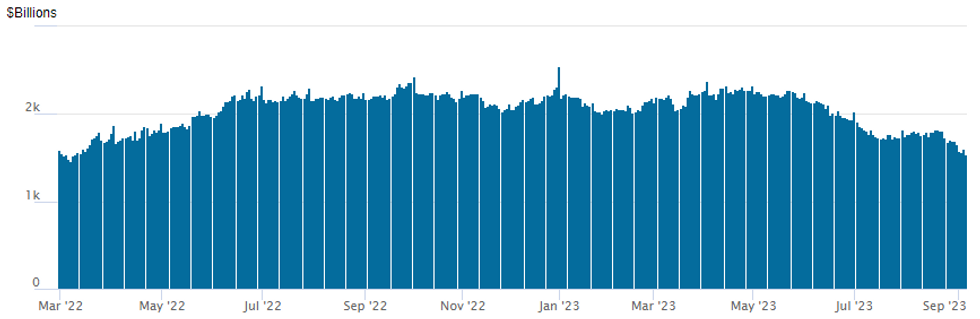

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

Repo operation falls to new low of $1,535.289B (last seen early March 2022) w/97 counterparties, compared to $1,606.244B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option trade remained mixed in late Thursday trade, largely repositioning and to a lesser degree squaring as underlying futures held modest gains. Rate hike projections through year end running steady: Sep 20 FOMC is 6.8% w/ implied rate change of +1.7bp to 5.347%. November cumulative of +12bp at 5.451, December cumulative of 11.3bp at 5.444%. Fed terminal at 5.45% in Nov'23.

- SOFR Options:

- Block, +4,350 0QX3 96.00/96.50 1x2 call spds, 12.5 ref 95.67

- 5,000 SFRX3 94.43/94.50/94.56/94.62 put condors ref 94.545

- Block, +20,000 SFRZ3 94.62/94.75/94.87 call flys, 2.0 net ref 94.545

- 4,000 0QZ3 95.87/96.75 call spds ref 95.635

- 2,600 0QU3 95.25/95.37/95.62 broken call trees ref 95.29

- 2,000 SFRZ3 95.25/96.25 call spds vs. 2QZ3 97.5/98.5 call spd

- 2,000 SFRX3 94.62 calls ref 94.55

- 2,000 0QV3 94.87/95.25/95.50 broken put flys vs. 0QV3 96.25 calls

- 2,000 0QV3 95.25 puts ref 95.63

- 1,500 SFRV3 94.68 calls, 3.0 ref 94.55

- Treasury Options:

- 2,500 FVX3 105.25 puts vs. FVX3 106.5/107.5 call spds, puts over ref 106-08.25

- 7,200 FVV3 106 calls, 33 ref 106-07.5

- 2,000 TYV3 108.75/110.75 call over risk reversals

- 3,000 USV3 123 calls, 10 ref 119-03

- -5,750 TYX3 108/112 call spds 159

- -6,500 TYX3 109 puts, 50 ref 109-25/0.40%

- 1,400 USV3/USX3 123 call spds, 39 Nov over

- 2,000 FVV3 104.5/105 2x1 put spds ref 106-05.5

- over 3,100 TYV3 109 puts, 22 ref 109-23

- appr +7,000 TYV3 109.25 puts, 24-25 ref 109-28 to -27

- 3,000 TYV3 111 calls, 15 ref 109-28

- 1,400 TYV3 108.25/109.25 2x1 put spds, 8 ref 109-21.5

EGBs-GILTS CASH CLOSE: Gilts Outperform Again With BoE Hikes Priced Out

Gilts outperform Bunds for a second consecutive session Thursday, with notable bull steepening in the UK curve as BoE hikes continued to be priced out.

- Following on from this week's BoE commentary which is seen relatively dovish, unexpectedly low BoE Decision Maker survey inflation expectations helped peak Bank Rate expectations dip nearly 10 basis points on the day, boosting the UK short-end.

- For the second consecutive session, European instruments weakened in afternoon trade alongside stronger-than-expected US data (jobless claims, unit labour costs), but the move didn't last.

- German yields fell in parallel fashion across most of the curve, with little change in ECB pricing.

- Periphery EGB spreads tightened modestly.

- Per the usual pre-meeting quiet period, no ECB speakers are scheduled between now and next Thursday's decision.

- After generally soft/dovish eurozone data Thursday (poor German industrial production and a downward revision to Q2 eurozone GDP), Friday brings final German inflation and multiple industrial production prints. No UK data of note.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.8bps at 3.084%, 5-Yr is down 4.4bps at 2.615%, 10-Yr is down 3.9bps at 2.614%, and 30-Yr is down 2.8bps at 2.745%.

- UK: The 2-Yr yield is down 10.2bps at 5.137%, 5-Yr is down 9.4bps at 4.716%, 10-Yr is down 7.9bps at 4.454%, and 30-Yr is down 7.8bps at 4.706%.

- Italian BTP spread down 2.2bps at 172.8bps / Spanish down 1.6bps at 103.5bps

EGB Options Mostly Upside In Rates; Schatz Profit Taking

Thursday's Europe rates / bond options flow included:

- ERU3 96.00 put bought for 0.75 in 9k, 40k on the day

- ERM4 98.00/50cs 1x2, bought the 2 for 1.25 in 3.5k

- ERX3 96.12/96.00ps 1x2, bought for 1.25 in 9k

- ERX3 96.12/96.25/96.37c fly 1x3x2, bought for 2 in 6k

- SFIV3 94.50/94.60/94.70c fly, bought for 1 in 5k

- SFIV3 94.60/94.70cs has bought for 1.5 in 14k total

- DUV3 105.30p now sold at 19 in 4.7k, was sold earlier at 20.5 in 5.1k that put was bought for 9 up to 13 previously.

FOREX USD Index Consolidates Gains, EURJPY Declines 0.60%

- The USD index has edged higher once more on Thursday, broadly consolidating the week’s solid advance and remaining in the medium-term uptrend drawn off the mid-July lows. Underperformance for major equity benchmarks has continued to underpin the resilient greenback.

- EURUSD has edged lower in sympathy, printing back below the 1.0700 handle for the first time since early June, narrowing the gap with 1.0635, the May 31 low and a key support. An additional headwind for the single currency may have been the weaker than expected revision of Q2 Eurozone GDP which came in at 0.1% Q/q, two tenths below the surveyed estimate.

- Of note, the Japanese Yen has outperformed modestly, with markets clearly still heeding the verbal intervention from both Matsuno and Kanda earlier in the week. Additionally, lower front-end yields in the US are easing the most recent downward pressure on the Yen.

- As such, EURJPY has fallen 0.6%, touching pullback lows of 157.36 in the process. The recent pullback is considered corrective, and the trend outlook remains bullish. Key support to watch is the 50-day EMA - at 156.72. A clear breach of this EMA would undermine the uptrend and highlight a possible short-term reversal.

- The Canadian dollar is one of the worst performers following the BOC decision yesterday and ahead of the August employment data on Friday with expectations for a further drift higher in the u/e rate but only a limited moderation in wage growth. An idiosyncratic pop higher in late trade to 1.3695 narrows in on cluster resistance at 1.3719 (1.0% 10-dma envelope) followed by 1.3722 (trendline resistance drawn from Oct 13, 2022 high).

FX Expiries for Sep08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0625-30(E530mln), $1.0700(E2.2bln), $1.0746-50(E1.3bln), $1.0795-15(E1.8bln), $1.0825-30(E1.5bln)

- USD/JPY: Y146.10-25($850mln), Y146.90-00($951mln)

- GBP/USD: $1.2500(Gbp1.2bln), $1.2569-80(Gbp621mln)

- AUD/USD: $0.6450(A$619mln), $0.6550(A$934mln), $0.6600(A$1.4bln)

- USD/CAD: C$1.3485-00($1.8bln), C$1.3600($700mln)

- USD/CNY: Cny7.3100($924mln)

Late Equity Roundup: Off Lows

- Stocks remain mixed, DJIA paring it's lead over weaker SPX and Nasdaq indexes in late trade. Currently, S&P E-Mini futures are down 16.25 points (-0.36%) at 4455, Nasdaq down 121.3 points (-0.9%) at 13750.63, DJIA up 44.79 points (0.13%) at 34487.58.

- Laggers: Information Technology, Materials and Industrials sectors continued to underperform. While a spotlight remained on Apple (down as much as 5% on the day, partly due to a expanding ban on IPhone use by China state officials), the tech firm was not the day's worst performer.

- That would be Seagate, down 10.3% in late trade after Barclays downgraded the company citing weaker hard drive demand. Other laggers included Skyworks Solutions and Qorvo both -7.5%, and Qualcomm -7.25%.

- Metals and mining shares weighed on Materials (FCX -2.45%) while airlines weighed on Industrials transportation subsector (AAL -2.5%, LUV -1.75%, UAL -1.35%).

- Leaders: Utilities, Real Estate and Health Care outperformed. Electric companies buoyed Utilities for the second day running: PG&E +2.5%, Constellation Energy +2.15%, Duke Energy +2.1% Specialized real estate investment trusts buoyed the Real Estate sector: American Tower +2.65%, SBA Communication +1.75%.

- Meanwhile, pharmaceutical and biotech shares supported Health Care: Eli Lilly +2.15%, Amgen +2.05%, Abbvie +2.0% in late trade.

E-MINI S&P TECHS: (U3) Pullback Extends

- RES 4: 4634.50 High Jul 27 and key resistance

- RES 3: 4593.50 High Aug 2

- RES 2: 4560.75 High Aug 4

- RES 1: 4547.75 High Sep 1

- PRICE: 4455.00 @ 1310 ET Sep 7

- SUP 1: 4433.50 Low Aug 29

- SUP 2: 4350.00 Low Aug 18 and a bear trigger

- SUP 3: 4344.28 38.2% retracement of the Mar 13 - Jul 27 bull cycle

- SUP 4: 4305.75 Low Jun 8

The E-mini S&P contract traded lower yesterday and remains softer today. Key resistance has been defined at 4547.75, Sep 1 high. A break is required to reinstate the recent bullish theme. Note that recent gains stalled at the area of resistance around the former bull channel base - drawn from the Mar 13 low. The line intersects at 4542.44. This is a bearish development and a continuation lower would expose key support at 4350.00, the Aug 18 low.

COMMODITIES Crude Lags Despite Surprisingly Large Inventory Draw

- Crude front month futures have eased back slightly today, ending a 9-day winning streak for WTI despite a larger than expected draw for US crude stocks in the EIA weekly petroleum summary (-6.31m vs -2.35m expected).

- The near term crude option put skews have continued to reduce after Saudi Arabia and Russia extended output cuts until the end of the year. The WTI downside skew is the least bearish since February. Both the second month Brent and WTI 25 delta call-put skews are back up to -2.25% compared to lows of around -4.7% in late August.

- JPMorgan analysts still don’t see oil prices breaching $100 in 2023, absent a major geopolitical event, due in large part to the demand outlook in 4Q despite the OPEC+ cut extension. Separately, RBC have Brent forecast to average 91$/bbl and WTI at $86.50/bbl in 4Q although $100/bbl could be within reach.

- Saudi Arabia is set to increase crude supplies to China in 2024 to meet demand at new refineries, sources told Platts at the APPEC conference in Singapore.

- WTI is -0.7% at $86.92, not testing support at $82.04 (20-day EMA) or resistance at $88.08 (yesterday high).

- Brent is -0.7% at $89.95 also not testing support at $85.97 (20-day EMA) not resistance at $91.15 (Sep 5 high).

- Gold is +0.2% at $1919.77 as the drag from a modestly stronger US dollar is offset by lower Treasury yields, holding above support at $1903.9 (Aug 25 low) whilst resistance remains at $1931.4 (50-day EMA).

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/09/2023 | 2300/1900 |  | US | Atlanta Fed's Raphael Bostic | |

| 07/09/2023 | 2305/1905 | | US | Dallas Fed's Lorie Logan | |

| 08/09/2023 | 0600/0800 | *** |  | DE | HICP (f) |

| 08/09/2023 | 0600/0800 | ** |  | SE | Private Sector Production |

| 08/09/2023 | 0645/0845 | * |  | FR | Industrial Production |

| 08/09/2023 | 0700/0900 | ** |  | ES | Industrial Production |

| 08/09/2023 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 08/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 08/09/2023 | 1300/0900 | | US | Fed Vice Chair Michael Barr | |

| 08/09/2023 | 1400/1000 | ** | | US | Wholesale Trade |

| 08/09/2023 | 1500/1100 | | US | San Francisco Fed's Mary Daly | |

| 08/09/2023 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.