Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: US CBO Projects November Budget Deficit Of $146B

- MNI BRIEF: McConnell Bends Liability 'Red Line' in Relief Talks

- EU'S VON DER LEYEN TO HOLD TALKS WITH JOHNSON TOMORROW EVENING, Bbg

- U.S. COVID-19 CASES SURPASS 15 MILLION: JOHNS HOPKINS DATA, Bbg

US

US: Senate Majority Leader Mitch McConnell proposed another slimmed-down relief package Tuesday, saying Congress should pass something this year while leaving state and local government aid and his own "red line" on firms' legal liability around Covid-19 to settle later.

- "We will be back at this after the first of the year" when the Biden administration will be asking for another relief package, McConnell said in a press conference, in reference to leaving out the most contentious issues for now. In past rounds of talks he insisted on a provision for liability.

- The Kentucky Republican advocated a package before year-end with items both political parties can agree on, including additional funding for the Paycheck Protection Program, vaccine delivery and assistance for health care workers. "We can't leave without doing a Covid bill," he said.

- Outlays for the month of November were USD365 billion, up roughly 11% from the same month last year, CBO estimates, and receipts totaled USD219 billion, down 3% percent compared to the same month last year.

- The federal budget deficit was USD430 billion for the first two months of fiscal year 2021, CBO projected: https://www.cbo.gov/system/files/2020-12/56886-MBR..., USD87 billion more than the deficit recorded during the same period last year.

OVERNIGHT DATA

US DATA: Q3 Final Nonfarm Productivity +4.6%; Unit Labor Costs -6.6%

- U.S. final nonfarm productivity rose 4.6% in Q3, a slight downward revision from the preliminary 4.9% increase reported last month, according to figures released Tuesday by the Bureau of Labor Statistics. Markets had expected final productivity to increase 4.8%. From a year earlier, nonfarm productivity was up 1.7%.

- Unit labor costs fell by 6.6% in Q3, up from last month's preliminary 8.9 decline and above expectations for an unrevised 8.9% decrease. Unit labor costs were up 1.9% from one year ago.

US REDBOOK: DEC STORE SALES -2.4% V NOV THROUGH DEC 05 WK

US REDBOOK: DEC STORE SALES +2.1% V YR AGO MO

US REDBOOK: STORE SALES +2.1% WK ENDED DEC 05 V YR AGO WK

US NFIB NOV SMALL BUSINESS INDEX 101.4

MARKETS SNAPSHOT

- DJIA up 104.61 points (0.35%) at 30167.38

- S&P E-Mini Future up 12.5 points (0.34%) at 3701.25

- Nasdaq up 62.8 points (0.5%) at 12582.3

- US 10-Yr yield is down 0.3 bps at 0.9195%

- US Mar 10Y are up 1.5/32 at 137-24.5

- EURUSD down 0.0001 (-0.01%) at 1.2103

- USDJPY up 0.11 (0.11%) at 104.17

- WTI Crude Oil (front-month) down $0.1 (-0.22%) at $45.62

- EuroStoxx 50 down 4.21 points (-0.12%) at 3530.08

- FTSE 100 up 3.43 points (0.05%) at 6555.39

- German DAX up 7.49 points (0.06%) at 13271

- French CAC 40 down 12.71 points (-0.23%) at 5573.38

US TSY SUMMARY: Weathering New Equity Highs

Tsys held higher levels after the close, Just off midmorning highs on a narrow overall range even as equities clawed to new all-time highs (ESZ0 3708.0).

- Equity bid belied a session that kicked off with a risk-off tone as a Covid relief package has still not been hammered out by Congress.

- Trading volumes were relatively subdued, two-way option position squaring ahead the year-end holidays.

- Little reaction to small tail in US Tsy $56B 3Y Note auction (91282CBA8) draws 0.211% high yield (0.250% last month) vs. 0.208% WI, on a bid/cover 2.28 vs. 2.40 previous. Indirects drew 49.25% vs. 38.89% prior, directs 15.87% vs. 14.28% prior, dealers w/ 34.88% vs. 46.83% prior.

- The 2-Yr yield is up 0.8bps at 0.1488%, 5-Yr is up 0.3bps at 0.3893%, 10-Yr is down 0.5bps at 0.9179%, and 30-Yr is down 1.3bps at 1.6662%.

US TSY FUTURES CLOSE: Long End notches Higher

Tsy futures traded higher for the most part after Tue's close, short end underperforming after 3Y auction tailed. Volumes thinning out (TYH<965k) on narrow ranges amid modest two-way positioning as the year-end holiday's near.

Latest levels:

- 3M10Y -0.153, 84.016 (L: 81.54 / H: 85.572)

- 2Y10Y -1.257, 76.546 (L: 75.061 / H: 79.259)

- 2Y30Y -2.004, 151.479 (L: 150.137 / H: 155.294)

- 5Y30Y -1.566, 127.627 (L: 126.788 / H: 130.196)

- Current futures levels:

- Mar 2Y -0.37/32 at 110-13.12 (L: 110-13 / H: 110-13.75)

- Mar 5Y +0.25/32 at 125-29 (L: 125-27.25 / H: 125-31.75)

- Mar 10Y +2/32 at 137-25 (L: 137-20 / H: 137-31.5)

- Mar 30Y +13/32 at 172-30 (L: 172-08 / H: 173-16)

- Mar Ultra 30Y +28/32 at 212-13 (L: 211-01 / H: 213-13)

US EURODLR FUTURES CLOSE: Strip Mirrors Tsy Yld Curve

Futures mixed levels throughout the session, narrow ranges with Blues-Golds outperforming. Lead quarterly held modest mildly weaker all session after 3M LIBOR settled -0.00038 to 0.23000% (+0.00412/wk).

- Dec 20 -0.002 at 99.755

- Mar 21 -0.005 at 99.795

- Jun 21 -0.005 at 99.80

- Sep 21 -0.010 at 99.790

- Red Pack (Dec 21-Sep 22) -0.01 to steady

- Green Pack (Dec 22-Sep 23) -0.01 to +0.005

- Blue Pack (Dec 23-Sep 24) +0.005 to +0.015

- Gold Pack (Dec 24-Sep 25) +0.015 to +0.025

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N -0.00038 at 0.08250% (-0.00075/wk)

- 1 Month +0.00300 to 0.14875% (-0.00330/wk)

- 3 Month -0.00038 to 0.23000% (+0.00412/wk)

- 6 Month +0.00025 to 0.25338% (-0.00237/wk)

- 1 Year -0.00100 to 0.33725% (+0.00050/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $57B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $154B

- Secured Overnight Financing Rate (SOFR): 0.08%, $951B

- Broad General Collateral Rate (BGCR): 0.07%, $360B

- Tri-Party General Collateral Rate (TGCR): 0.07%, $338B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.401B accepted vs. $5.777B submission

- Next scheduled purchases:

- Wed 12/09 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Thu 12/10 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Fri 12/11 1010-1030ET: Tsy 0Y-2.25Y, appr $12.825B

- Fri 12/11 Next forward schedule release at 1500ET

PIPELINE: $10.766B To Price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 12/08 $2.5B #Charles Schwab PerpNC10 4%

- 12/08 $2B #Charles Schwab $1.25B 5Y +53, $750M 10Y +75

- 12/08 $3B #Kingdom of Morocco $750M 7Y +175, $1B 12Y +200, $1.25B 30Y +4%

- 12/08 $1.5B #Occidental Petroleum $750M 5Y 5.5%, $1.25B 10Y 6.12%

- 12/08 $1.266B #Dominican Republic 2032 Tap 4.1%

- 12/08 $500M #CBOE 10Y +78

FOREX: Ebb & Flow of Brexit Still Dominating Force

The ebb and flow of Brexit news flow continues to dominate markets, with another sizeable GBP/USD trading range for spot. Front-end GBP implied vols continue to ratchet higher, indicating the market's caution over the outcome of the ongoing negotiations. The latest reports suggest that both sides are preparing documents and briefings ahead of the face-to-face meeting between EU's von der Leyen and UK's Johnson due to take place on an unspecified day later this week. GBP/USD fluctuated between 1.3290 and 1.3393.

- The greenback traded well, with the USD index inching higher despite a generally favourable equity backdrop. CHF was the strongest in G10, while SEK was the weakest.

- Focus Wednesday turns to Chinese inflation data for November and rate decisions from the Canadian and Brazilian central banks. Both institutions are seen keeping rates unchanged.

EGBs-GILTS CASH CLOSE: Bull Flattening As Brexit Intrigue Continues

Strong bull flattening in both the Bund and Gilt curves on Tuesday, though the UK outperformed as Brexit intrigue continued, with no macro drivers otherwise. Periphery spreads traded sideways.

- News that the EU and UK had reached an agreement on the outstanding issues in the Withdrawal Agreement was treated fairly equivocally, initially modestly bearish Gilts but that move faded.

- More attention on repeated reports that EU's Barnier saw odds of a deal as slim. Main focus is on PM Johnson's upcoming trip to Brussels, timing still TBD. Wednesday's calendar looks thin, with supply (UK and German auctions) the main area of interest.

- Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is down 1.4bps at -0.773%, 5-Yr is down 1.7bps at -0.794%, 10-Yr is down 2.5bps at -0.607%, and 30-Yr is down 2.9bps at -0.185%.

- UK: The 2-Yr yield is down 0.6bps at -0.081%, 5-Yr is down 1bps at -0.04%, 10-Yr is down 2.6bps at 0.257%, and 30-Yr is down 5.5bps at 0.799%.

- Italian BTP spread up 0.5bps at 119.7bps

- Spanish bond spread up 0.2bps at 63.6bps/Portuguese up 0.2bps at 60.1bps

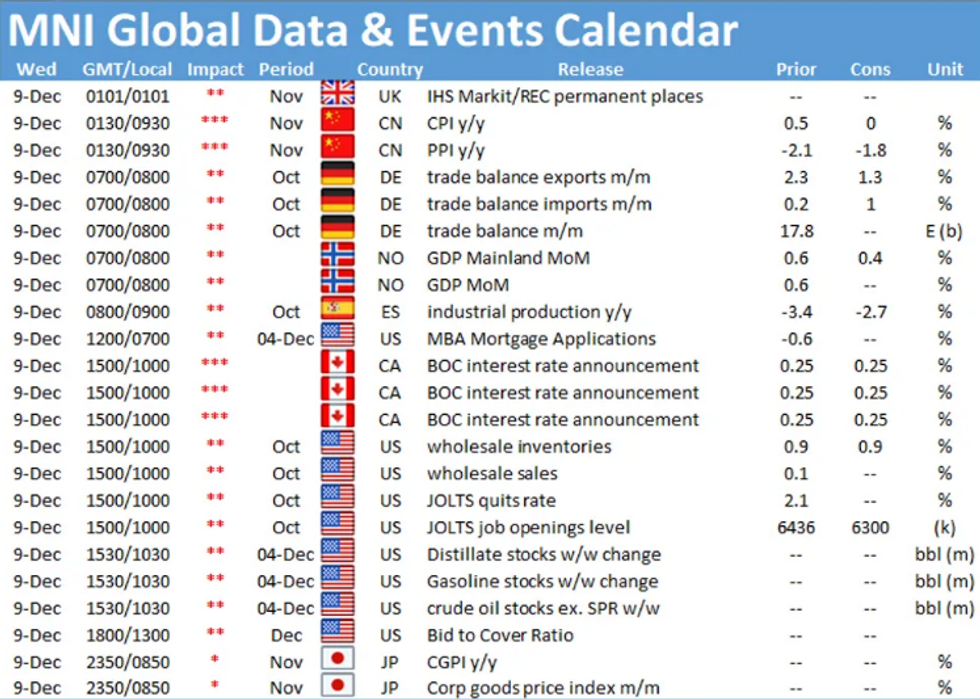

UP TODAY

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.