Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI POLICY: US Household Inflation Expectations Hit 7 Yr High

- US: CDC: Fully Vaccinated People Can Meet With Unvaccinated In Small Groups

- FUTURE CDC GUIDANCE COULD INCLUDE TRAVEL FOR VACCINATED PEOPLE, Bbg

- MNI BRIEF: BOE Must Tackle Swollen Balance Sheet Issue

- MNI SOURCES: ECB To Fend Off Yield Pressure; PEPP Debate Looms

US

US: U.S. household inflation expectations reached the highest in almost seven years in February, a New York Federal Reserve survey showed Monday.

- The median inflation outlook for the next year increased by 0.1 percentage point from January to 3.1%, the highest reading since July 2014. The median three-year outlook for inflation was unchanged from the prior month at 3.0%, holding at an almost three-year high. For more see MNI Policy main wire at 1103ET.

US: CDC: Fully Vaccinated People Can Meet With Unvaccinated In Small Groups

NBC News tweets: "CDC releases guidance on safe activities after Covid-19 vaccination, including guidance that fully vaccinated grandparents can visit safely with unvaccinated grandchildren. People who are fully vaccinated against Covid may safely gather with small groups from other households without wearing masks or physical distancing, even if those people have not yet had their shots, CDC says. In public or around others who are vulnerable to Covid-19 complications, mitigation measures such as wearing masks and maintaining physical distance should remain status quo, CDC says."

- The US is the first country globally to issue separate guidance for those vaccinated against COVID-19, with the enabling of those who are vaccinated to meet in groups with others even if they are not vaccinated a significant step.

- CDC advice stands in stark contrast to other Western states doing well with vaccine rollout. In the UK today, PM Boris Johnson asserted that despite a strong vaccine rollout and declining cases the easing of restrictions would not be brought forwards, and everyone would have to abide by the same guidelines whether vaccinated or not.

US TSYS: Tsy Sec Yellen on MSNBC, Bloomberg Headlines:

- YELLEN: STIMULUS BILL WILL HELP HUNDREDS OF MILLIONS OF PEOPLE

- YELLEN: ECONOMY COULD GET BACK TO PRE-PANDEMIC JOBS NEXT YEAR

- YELLEN: WE HAVE A K-SHAPED RECOVERY HAPPENING NOW

- YELLEN: WE'RE GOING TO TURN TO BUILD BACK BETTER PLAN NEXT

- YELLEN: DON'T EXPECT UNDESIRABLE LEVELS OF INFLATION

- YELLEN: IF RECOVERY IS INFLATIONARY, THERE ARE TOOLS FOR THAT

US TSYS: Quicktake: Cross-Market Opinion On Rate Sale

TD Securities strategists opined on the disorderly global sell-off in rates over the last few weeks, "with some countries outpacing" the sell-off in US rates. "While much of the move was due to the global nature of the economic optimism regarding the end of COVID, there was also an element of positioning."

- That said, TD believes the rise in yields "is overdone in the front end across most markets. We are long 5y Treasuries and received 1y1y in EUR and 1y1y in CAD. We also received 2y1y in the UK versus the US."

- We look for US rates to continue to be pressured higher amid heavy issuance and a Fed unwilling to push back against the move. If US rates keep rising, we expect AU and GE yields to outperform. We are also long 10y UK against Bunds and long AU 10y against the US. On the other hand, bonds in CA and UK should be the most vulnerable to a further rise in US rates.

Societe Generale strategists anticipate 10Y yield will reach 2.0% by year end (1.592% currently after topping 1.6238% last Friday) citing "Fiscal support, improving fundamentals, easy financial conditions and an accommodative Fed support."

- While higher yields and steeper curves should prevail, the pace of the sell-off is likely to moderate in 2H.

- Although the Fed reaction to higher yields has been muted thus far, policy response to a continued sell-off remains a key risk to our call for higher yields. The Fed will likely tolerate higher yields if fundamentals continue to improve and financial conditions remain accommodative.

EUROPE

UK: With the Bank of England's balance sheet set to swell to GBP1 trillion and with the central bank having failed to reduce it all between the end of the financial crisis and the onset of the Covid shock, it must now address the issue, Governor Andrew Bailey said Monday.

- His remarks, at a Resolution Foundation event, underscore why he is keen to press ahead with the review of tightening policy, with Bailey expressing sympathy for the case for early unwind of quantitative easing in order to give policymakers room to act if another crisis hits. "We do have to take very seriously what room we have for maneuver on the central bank balance sheet and how we respond to the next crisis," he said.

- Recent remarks by Executive Board members Philip Lane, Isabel Schnabel, Luis de Guindos and Fabio Panetta have made it more likely central bank governors will look favourably on deploying the EUR1.85 trillion Pandemic Emergency Purchase Programme more rapidly, one central bank official said, though adding to the overall envelope is not on the table.

OVERNIGHT DATA

US JAN WHOLESALE INV 1.3%; SALES 4.9%- FED EXTENDSPAYCHECK PROTECTION PROGRAM FACILITY THRU JUNE

- FED ANNOUNCES CLOSURE OF THREE 13(3) FACILITIES AS SCHEDULED MARCH 31

- FED TO CLOSE COMMERCIAL PAPER, MONEY MARKET, PRIMARY DEALER FACILITIES

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 492.68 points (1.56%) at 31994.95

- S&P E-Mini Future up 10 points (0.26%) at 3849

- Nasdaq down 201.3 points (-1.6%) at 12720.18

- US 10-Yr yield is up 2.6 bps at 1.5924%

- US Jun 10Y are down 15/32 at 131-28

- EURUSD down 0.0057 (-0.48%) at 1.1858

- USDJPY up 0.56 (0.52%) at 108.87

- WTI Crude Oil (front-month) down $1.28 (-1.94%) at $64.80

- Gold is down $15.57 (-0.92%) at $1685.17

European bourses closing levels:

- EuroStoxx 50 up 93.7 points (2.55%) at 3763.24

- FTSE 100 up 88.61 points (1.34%) at 6719.13

- German DAX up 460.22 points (3.31%) at 14380.91

- French CAC 40 up 120.34 points (2.08%) at 5902.99

US TSY SUMMARY: Not Easy Being a (Stock) Bear

Rates opened and held weaker levels throughout the session, inside range day with small variations in the first half: Tsy and equities bounced after Appaloosa's David Tepper said it's "difficult to be bearish on stocks" during a CNBC interview. S&Ps reversed gains after Tsy close to mildly weaker, NDX extended losses (-260.0) while Dow Indu's held strong gains +428.0).- No react to second tier data: Jan Wholesale inventories 1.3%; Sales 4.9%. Federal Reserve in media blackout through the March 17 FOMC annc. That said, Fed annc:

- EXTENDS PAYCHECK PROTECTION PROGRAM FACILITY THRU JUNE; CLOSURE OF THREE 13(3) FACILITIES AS SCHEDULED MARCH 31; CLOSE COMM PAPER, MONEY MARKET, PRIMARY DEALER FACILITIES.

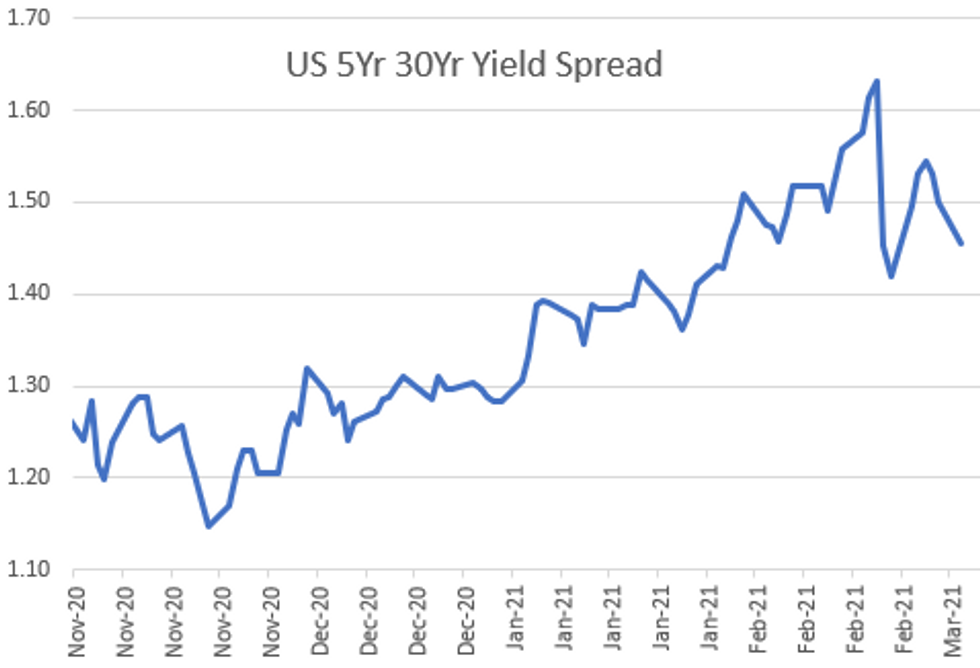

- Yield curves hold mixed levels, spds vs. long end flatter: 5s30s near session lows late: 145.483, -4.344. 30YY near steady (2.3059% +.0085) despite the drop in Bond futures, 10s30s curve underperforming for couple reasons, sources citing a rise in inflation premium and SLR exemption is set to expire March 31 with no signs yet of extension.

- Large Eurodollar spread volumes: +65,000 Red Mar/Red Jun spds, 0.040-0.050. Modest long put unwinds while core positions remain long rate hike insurance covering latter half 2022 to 2023. Several put spd over call spd skew plays in 1Y midcurves bought on day.

- The 2-Yr yield is up 2.4bps at 0.1607%, 5-Yr is up 5bps at 0.8487%, 10-Yr is up 2.6bps at 1.5924%, and 30-Yr is up 0.5bps at 2.3028%.

US TSY FUTURES CLOSE: Late 10s30s Ultra Bond Steepener Did Some Damage

Large, uneven steepener Block:

- +3,500 UXYM1 145-19, buy through 145-18 post-time offer at 1556:48

- -5,410 WNM1 at 185-02, well through the 158-11 post-time bid

- Jun 2Y down 2/32 at 110-11.125 (L: 110-11 / H: 110-13)

- Jun 5Y down 12.25/32 at 123-18.75 (L: 123-17.75 / H: 123-27.75)

- Jun 10Y down 16.5/32 at 131-26.5 (L: 131-24.5 / H: 132-05)

- Jun 30Y down 20/32 at 156-19 (L: 156-08 / H: 157-04)

- Jun Ultra 30Y down 45/32 at 185-2 (L: 184-23 / H: 186-18)

US EURODOLLAR FUTURES CLOSE: Weaker, At/Near Lows

Futures trade weaker across the strip, at/near session lows on heavy volumes, large calendar spds on day (+65,000 Red Mar/Red Jun spds, 0.040-0.050). Lead quarterly ended up softer after showing little react to 3M LIBOR set: -0.00288 to 0.18250% (-0.00300 total last wk).

- Mar 21 -0.0025 at 99.875

- Jun 21 -0.005 at 99.835

- Sep 21 -0.010 at 99.815

- Dec 21 -0.010 at 99.765

- Red Pack (Mar 22-Dec 22) -0.03 to -0.015

- Green Pack (Mar 23-Dec 23) -0.07 to -0.035

- Blue Pack (Mar 24-Dec 24) -0.085 to -0.08

- Gold Pack (Mar 25-Dec 25) -0.09 to -0.08

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00000 at 0.07763% (-0.00637 total last wk)

- 1 Month +0.00275 to 0.10600% (-0.01525 total last wk)

- 3 Month -0.00288 to 0.18250% (-0.00300 total last wk) (Just above Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00037 to 0.19625% (-0.00712 total last wk)

- 1 Year +0.00250 to 0.28025% (-0.00600 total last wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $69B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $210B

- Secured Overnight Financing Rate (SOFR): 0.02%, $933B

- Broad General Collateral Rate (BGCR): 0.01%, $364B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $339B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.201B accepted vs. $4.211B submission

- Next scheduled purchase:

- Tue 3/9 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Wed 3/10 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- hu 3/11 1500 Next scheduled release schedule

PIPELINE: Debt Roundup: $21.5B To Price Monday

- Date $MM Issuer (Priced *, Launch #)

- 03/08 $5.5B #Bank of America $2.5B 6NC5 +80, $2B 11NC10 +105, $1B 31NC30 +115

- 03/08 $3.5B #Anthem $500M 2Y +30, $750M 5Y +70, $1B 10Y +100, $1.25B 30Y +130

- 03/08 $3B #Teledyne $300M 2Y +50, $450M 3NC1 +65, $450M 5Y +75, $700M 7Y +100, $1.1B 10Y +120

- 03/08 $2.5B *One Gas $1B 2NC.5 +70, $800M 2NC.5 FRN L+61, $700M 3NC.5 +80

- 03/08 $2.4B #Pacific Gas & Electric $1.5B 2NC.5 +120, $450M 10Y +167, $450M 20Y +200

- 03/08 $2B *Santander UK $1.4B 4NC3 +75, $600M 11NC10 +130

- 03/08 $1.1B #CenterPoint Energy $400M 10Y +80, $700M 30Y +105

- 03/08 $1B #AmFam Holdings $500M 10Y +120, $500M 30Y +150

- 03/08 $500M *Southwestern Electric 5Y +80

- 03/08 $5B American Airlines $2.5B 5NC, $2.5B 8NC investor calls

- 03/08 $Benchmark Sasol investor calls re: 5Y, 10Y

- 03/08 $Benchmark Deutsche Bank investor calls

FOREX: JPY Sags as Equities Rip to New All Time Highs

- The JPY was among the poorest performers in G10 Monday, with USD/JPY extending the recent sequence of higher highs to ten consecutive sessions. The move coincided with further upside in US equities, with the recovery rally now boosting the Dow Jones Industrial Average through the late February highs to record levels.

- The buoyant risk sentiment correlated with a stronger dollar, as the USD Index extended the recent bull run.

- EUR traded weaker, with the expected uptick in PEPP purchases failing to materialise in last week's bond holdings data. This will likely continue to be a market focus headed into this Thursday's ECB meeting.

- Focus Tuesday turns to German trade balance data for January and final Q4 GDP readings for the Eurozone. RBA Governor Lowe is also due to speak.

EGBs-GILTS CASH CLOSE: ECB Week Begins With Bund Weakness

A strong performance by European equities saw Bunds weaken, though Gilts were a little stronger on the session Monday.

- Bund yields moved to session highs alongside MNI's Exclusive on ECB policy ("hawks and doves within the Governing Council are biding their time ahead of a bigger battle over the long-term future of its monetary toolkit") published late afternoon.

- Periphery spreads were lower on the session; Greece (10Y -4.1bps/Bunds) outperformed. This despite 'disappointing' ECB net asset purchase data which saw a small downtick in PEPP buys.

- BoE's Bailey added little new in his appearance today.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 1bps at -0.68%, 5-Yr is up 2.1bps at -0.594%, 10-Yr is up 2.5bps at -0.277%, and 30-Yr is up 1.6bps at 0.225%.

- UK: The 2-Yr yield is down 0.2bps at 0.098%, 5-Yr is down 0.8bps at 0.358%, 10-Yr is down 0.2bps at 0.754%, and 30-Yr is down 0.2bps at 1.285%.

- Italian BTP spread down 2.3bps at 103.3bps/ Spanish spread down 1.9bps at 67.6bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.