Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI INTERVIEW: US Mfg Price Increases Have Peaked - ISM Chief

- MNI BRIEF: US Treasury Reduces Q3 Borrowing Estimate to $673B

- FED WALLER: HE COULD BE READY TO MAKE TAPER ANNOUNCEMENT BY SEPT, Bbg

- FED WALLER SAYS HE FAVORS `GOING EARLY AND GOING FAST' ON TAPER, Bbg

- BIDEN CALLS ON STATES TO BAN EVICTIONS FOR AT LEAST TWO MONTHS, Bbg

US

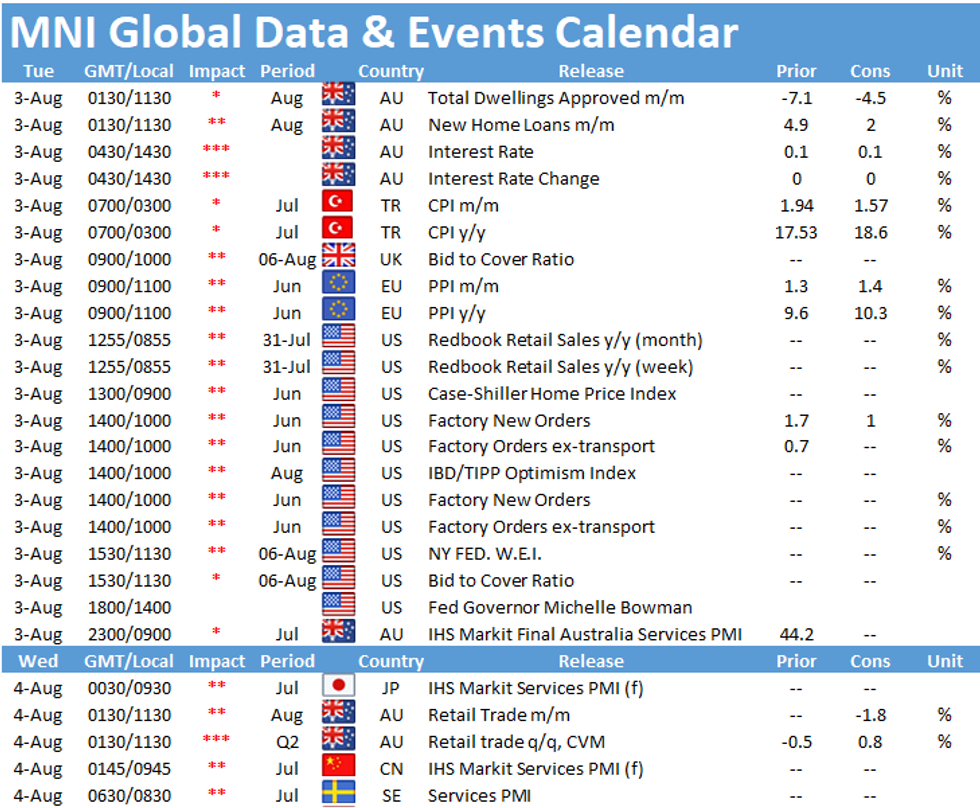

US: U.S. manufacturing price gains likely peaked in June, the Institute for Supply Management chair Tim Fiore told MNI Monday, and the prices index will fall into the 70s in the months ahead as supply and demand move closer to equilibrium.

- "I have been comfortable for sure calling this transitory," he said, joining the core of the Federal Reserve in seeing recent price surges as temporary. "I'm encouraged by the fact of the amount of people reporting price increases dropped in the month of July."

- The Institute for Supply Management's price index dropped 6.4 points to 85.7 in July, still the 14th consecutive month of expansion. The survey showed 73.8% of firms reporting higher prices, down from 84.8% in June, while 23.8% saw no change and 2.4% registered declining prices. For more, see MNI Policy main wire at 1355ET.

- The third-quarter estimate assumes an end-of-September cash balance of USD750 billion, the Treasury said in a statement, and estimates assume enactment of a debt limit suspension or increase. The Treasury said it issued USD319 billion in net debt in the second quarter and expects to borrow USD703 billion in the October to December quarter, assuming an end-of-December cash balance of USD800 billion.

OVERNIGHT DATA

- US FINAL JUL MFG PMI 63.4 (63.1 FLASH, 62.1 JUN)

- ISM Jul Manufacturing PMI Slipped To 59.5 vs Jun 60.6

- US ISM NEW ORDERS INDEX 64.9 JUL VS 66.0 JUN

- US ISM EMPLOYMENT INDEX 52.9 JUL VS 49.9 JUN

- US ISM PRODUCTION INDEX 58.4 JUL VS 60.8 JUN

- US ISM SUPPLIER DELIVERY INDEX 72.5 JUL VS 75.1 JUN

- US ISM INVENTORIES INDEX 48.9 JUL VS 51.5 JUN

- The ISM Mfg PMI dropped 1.1pt in Jul to 59.5, hitting the lowest level since Jan and coming in weaker than market forecasts (BBG: 60.7).

- Jul's downtick was led by an decrease of Supplier Deliveries (-2.6pt), Production (-2.4pt), Inventories (-2.2pt) and New Orders (-1.1pt), while Production (+3.0pt) posted the only gain among the main sub-indicators.

- Inventories shifted back to contraction territory following two months of expansion.

- Production saw the first increase in three months, while New Orders and Supplier Deliveries posted the second successive declines.

- Among the other categories, Imports saw the largest decline, down 7.3pt to 53.7, marking a three-month low.

- Meanwhile, Prices fell 6.4pt to 85.7 in Jul, its lowest level since Mar and Customer's inventory dropped 5.8pt to 25.0.

- While Order Backlogs ticked up 0.5pt to 65.0, Exports declined 0.5pt to 55.7 in July.

- US JUN CONSTRUCT SPENDING +0.1%

- US JUN PRIVATE CONSTRUCT SPENDING +0.4%

- US JUN PUBLIC CONSTRUCT SPENDING -1.2%

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 3.26 points (-0.01%) at 34930.07

- S&P E-Mini Future up 1.75 points (0.04%) at 4391.25

- Nasdaq up 54.8 points (0.4%) at 14730.4

- US 10-Yr yield is down 5 bps at 1.1723%

- US Sep 10Y are up 17.5/32 at 135-0

- EURUSD up 0.0001 (0.01%) at 1.1872

- USDJPY down 0.44 (-0.4%) at 109.28

- WTI Crude Oil (front-month) down $2.74 (-3.71%) at $71.23

- Gold is up $0.66 (0.04%) at $1814.61

- EuroStoxx 50 up 27.32 points (0.67%) at 4116.62

- FTSE 100 up 49.42 points (0.7%) at 7081.72

- German DAX up 24.34 points (0.16%) at 15568.73

- French CAC 40 up 63.14 points (0.95%) at 6675.9

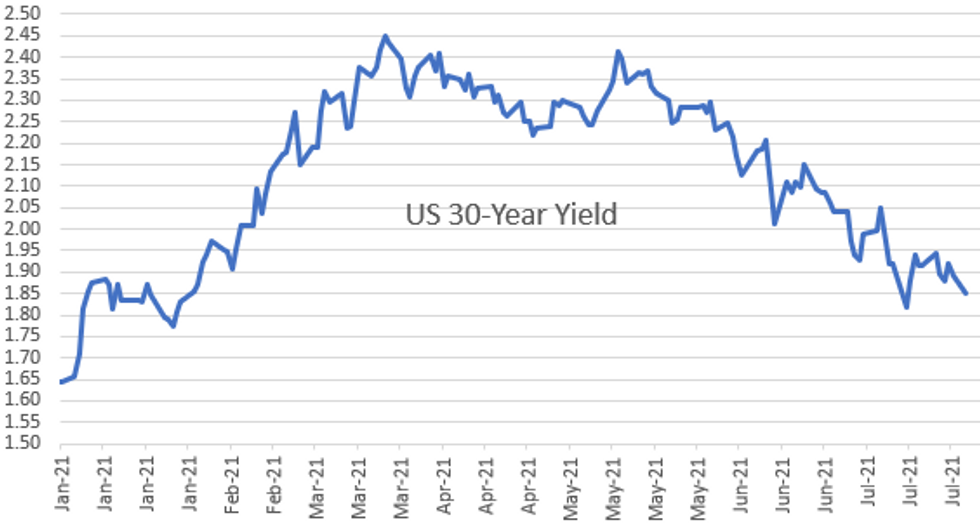

US TSY SUMMARY: Yields Slip on Early Geopolitical Angst

Tsy yields kicked off August weaker, 10-day lows by midday Monday before retracing appr a third of the move in quiet second half trade.- Tsys opened bid, trading steadily higher into noon amid unwinds of late Fri sales. Desks also cited a pick-up in geopolitical risk on Iranian Press TV headlines that the country will "give a strong and crushing response to any measures against its interests and national security" (not unusual rhetoric from Iran and oil prices traded broadly weaker).

- Meanwhile: RUSSIA SAYS THE UNITED STATES HAS ASKED 24 OF ITS DIPLOMATS WHOSE U.S. VISAS ARE EXPIRING TO LEAVE THE COUNTRY BY SEPT. 3 - TASS. Whatever the reason, stocks traded weaker underscoring the first half risk-off tone on lighter volume.

- No market react to late hawkish comments from Fed Gov Waller interview on CNBC: "HE COULD BE READY TO MAKE TAPER ANNOUNCEMENT BY SEPT" while the Fed "COULD TAPER AT A FASTER PACE THAN LAST TIME".

- The 2-Yr yield is down 1bps at 0.1741%, 5-Yr is down 4bps at 0.6505%, 10-Yr is down 5bps at 1.1723%, and 30-Yr is down 4.1bps at 1.851%.

US TSY SUPPLY: Tsy Quarterly Refunding Estimates

With infrastructure spending bill, Tsy financing needs into 2022 still uncertain -- it's unlikely that the Tsy will make any changes to coupon auction sizes at this Wed's quarterly refunding announcement. Sell side opinions as to when vary:

- "Given Treasury's 'regular and predictable' approach to debt management", Goldman Sachs expects "major cuts" in coupon auction sizes to start this Nov'21. "With the budget deficit likely to decline by more than 50% in FY22, and Treasury projected to remain more than adequately financed from its calendar of coupon offerings in FY23 and beyond, we think this requires relatively large adjustments to auction sizes through mid-2022."

- GS projects "monthly 2-, 3-, and 5- year auction sizes dropping by $12bn between November 2021 and April 2022, and project 7-year auction sizes are cut by $18bn over the same period." GS estimates larger "cuts for the 7-year note and 20-year bond compared to other surrounding maturity points" that "will reduce gross issuance of coupons by $814bn in 2022 compared with 2021."

- UBS analysts agree that November is a likely time to annc coupon cuts, but due to the uncertainty over size of fiscal packages not to mention the spread of the Delta variant outlook, UBS expects the first auction cuts in May of 2022 (or perhaps Feb'22 at the earliest) "will be aggressive and will be more pronounced in the long end, particularly to the 20y."

| DATE | 2Y | 3Y | 5Y | 7Y | 10Y | 20Y | 30Y |

| May'22 | $57B | $55B | $59B | $60B | $37B | $22B | $25B |

US TSY FUTURES CLOSE

- 3M10Y -4.498, 113.165 (L: 110.185 / H: 119.06)

- 2Y10Y -3.522, 99.922 (L: 97.531 / H: 105.82)

- 2Y30Y -3.14, 167.298 (L: 165.721 / H: 173.284)

- 5Y30Y -0.767, 119.258 (L: 118.908 / H: 122.82)

- Current futures levels:

- Sep 2Y up 0.75/32 at 110-11.25 (L: 110-10.75 / H: 110-11.75)

- Sep 5Y up 7/32 at 124-21.25 (L: 124-15.25 / H: 124-24.75)

- Sep 10Y up 15.5/32 at 134-30 (L: 134-14.5 / H: 135-05)

- Sep 30Y up 1-7/32 at 165-30 (L: 164-14 / H: 166-14)

- Sep Ultra 30Y up 1-25/32 at 201-10 (L: 198-20 / H: 202-07)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.005 at 99.880

- Dec 21 steady at 99.825

- Mar 22 +0.010 at 99.855

- Jun 22 +0.010 at 99.815

- Red Pack (Sep 22-Jun 23) +0.015 to +0.040

- Green Pack (Sep 23-Jun 24) +0.050 to +0.060

- Blue Pack (Sep 24-Jun 25) +0.065 to +0.070

- Gold Pack (Sep 25-Jun 26) +0.070 to +0.080

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00262 at 0.07950% (-0.00325 total last wk)

- 1 Month -0.00087 to 0.08963% (+0.00438 total last wk)

- 3 Month +0.00600 to 0.12375% (-0.01113 total last wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month +0.00350 to 0.15663% (-0.00538 total last wk)

- 1 Year -0.00275 to 0.23238% (-0.00625 total last wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $61B

- Daily Overnight Bank Funding Rate: 0.06% volume: $215B

- Secured Overnight Financing Rate (SOFR): 0.05%, $903B

- Broad General Collateral Rate (BGCR): 0.05%, $368B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $343B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.199B accepted vs. $1.922B submission

- Next scheduled purchases

- Tue 8/03 1010-1030ET: Tsy 10Y-22.5Y, appr $1.425B

- Wed 8/04 1100-1120ET: Tsy 7Y-10Y, appr $3.225B

- Thu 8/05 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 8/06 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

FED: Reverse Repo Operations -- Record High, Over $1T

NY Fed reverse repo usage recedes to $921.317B from 70 counterparties vs. last Friday's new record high of $1.039.394B (compares to prior record high of $991.939B on June 30).

PIPELINE: $3.75B Credit Suisse Launched, 5Y FRN Dropped

- Date $MM Issuer (Priced *, Launch #)

- 08/02 $3.75B #Credit Suisse $1.4B 2Y +35, $600M 2Y FRN/SOFR+38, $1.75B 5Y +65

- 08/02 $2.5B #Honeywell Int $1B 5.5Y +45, $1.5B 10Y +60

- 08/02 $1.25B Charter Comm 12.5NC6.5 4.375%a

- 08/02 $2B Sirius XM Radio 5NC2, 10NC5

- 08/02 $620M #Rwanda 10Y 5.5%

- Later in week

- 08/03 $Benchmark Bank of China 2Y FRN

EGBs-GILTS CASH CLOSE: Strong Rally As Growth Fears Re-Emerge

European FI enjoyed a very strong start to the week/month, with bull flattening in the UK and German curves, and periphery spreads flattening.

- A fairly subdued morning with modest weakness gave way to increasing strength as the session went on, with Italy and Spain PMIs disappointing, and later, the US Manufacturing ISM pointing to inflation and activity slowing.

- As we entered the cash close, gains in FI were accelerating, as equities began to pare substantial gains made earlier in the session. No particular trigger seen, but potentially geopolitical (Iran rumblings) and general growth risks.

- Notably, German 30Y yields fell below 0% for the first time since February.

- A quiet slate Tuesday, Austria and the UK sell bonds.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.3bps at -0.775%, 5-Yr is down 1.3bps at -0.755%, 10-Yr is down 2.6bps at -0.487%, and 30-Yr is down 3.1bps at -0.011%.

- UK: The 2-Yr yield is down 2.6bps at 0.034%, 5-Yr is down 4.1bps at 0.225%, 10-Yr is down 4.4bps at 0.521%, and 30-Yr is down 3.6bps at 0.958%.

- Italian BTP spread down 2.4bps at 105.8bps / Spanish down 0.9bps at 72bps

FOREX: Broad JPY Strength As Equities Give Up Gains

- The Japanese Yen firmed to start the week as US equity indices gave back earlier gains and risk sentiment soured, evident by the large move lower in crude futures.

- The European session had been characterised by a slightly softer greenback. USDJPY (-0.42%) extended this weakness, resting just 20 pips shy of the July lows of 109.07.

- The Canadian dollar traded heavily with the oil move, however G10FX lacked any momentum in a lacklustre Monday session. CADJPY had the most notable swing, retreating 0.7%.

- Despite the souring sentiment, potentially fuelled by an uptick in geopolitical risk stemming from headlines concerning Iran and Russia, there were significant moves higher for some emerging market currencies. USDTRY and USDZAR both receded over 1% while the Brazilian Real advanced 1.35%, retracing a good portion of Friday's move lower.

- Additionally, the Australian Dollar was resilient, rising 0.3% to $0.7365. This comes ahead of the RBA rate decision/statement due overnight where markets will likely see the RBA reneging on its previously outlined tapering move before it goes into play.

- The trend outlook is unchanged and bearish for AUDUSD. This follows the recent breach of a channel base drawn from the Feb 25 high, signalling potential for 0.7235 next, a 1.236 projection of the Feb 25 - Apr 1 - May 10 price swing. On the upside, initial resistance is at 0.7429, Jul 19 high.

- Spanish unemployment due tomorrow before US factory orders. Then Fed Gov Bowman due to deliver opening remarks at a webinar hosted by the Board of Governors of the Federal Reserve System.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.