Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Treasury Rules Need To Keep Up With Tech, Trades - Liang

- MNI STATE OF PLAY: BOE Hikes 50bps And Launches Gilt Sales

- MNI Fed Review - Sept 2022: Slightly Restrictive And Very Real

US

FED: Reduced Treasury liquidity since the beginning of the year has served as a daily reminder that regulators need to be vigilant in monitoring market risks and continue to explore ways to enhance Treasury market resilience, Treasury Under Secretary for Domestic Finance Nellie Liang said Thursday.

- In a speech to SIFMA providing a progress report on enhancing the resilience of the Treasury market, Liang said regulators are not attempting to eliminate volatility or completely insulate the market from periods of stress but rather increase the market's ability to absorb shocks.

- "To ensure the Treasury market continues to fulfill these vital purposes, the official sector needs to seek continual improvements that strengthen the Treasury market in order to keep pace with changing technology and trading patterns," she said in prepared remarks. Liang pointed to various efforts to improving data quality and availability and examining effects of leverage and fund liquidity risk management.

FED REVIEW: The FOMC continued to ratchet up its inflation-fighting message at the September meeting, adding more specific rate-setting contours to Chair Powell’s Jackson Hole speech via a hawkish Dot Plot.

- Markets repriced accordingly, and several sell-side analysts raised their Fed hiking outlooks following the meeting. Another 75bp hike in November, with 50bp in December is now the baseline outlook, with a peak 2023 rate above 4.5%.

- Powell's comments on what constituted "restrictive policy" both underlined that the Fed had a "ways to go" on rates versus the current "very lowest level of what might be restrictive", and suggested that the real rates outlook will be increasingly key in assessing how “restrictive” the Fed sees policy.

EUROPE

BOE: The Bank of England’s Monetary Policy Committee split three ways as it lifted its policy rate by 50 basis points to 2.25% at its September meeting while unanimously backing the launch of its gilt sales programme even as a government package aimed at mitigating the jump in energy costs is set to ramp up public borrowing.

- The meeting’s minutes showed that five of the nine-member MPC, including Governor Andrew Bailey, who votes last, opted for 50bps, while three wanted 75bps and one only 25bps. The likelihood is now that the next meeting in November will also see opinions divided over whether to hike by an additional 50 or 75 bps.

- Any speculation that the Bank might delay launching, or significantly scale back, its gilt sales programme because of the looming increase in government borrowing turned out to be misjudged, with all nine MPC members backing the decision to start the gilt sales programme outlined in August. For more see MNI Policy main wire at 1002ET.

US TSYS: Market Roundup, Holding Near Lows Through Second Half

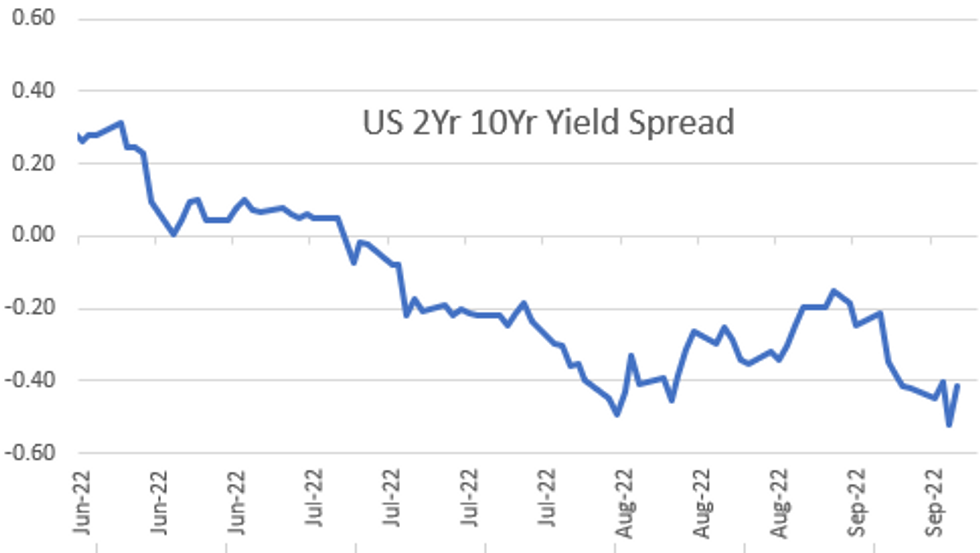

Tsys broadly weaker after the close - holding narrow range through the second half - near first half lows where ylds hit new 15Y highs (2YY 4.1587% after topping 4.0% in aftermath of Wed's 75bp FOMC rate hike; 5YY 3.9399%, 10YY 3.7118%). 2s10s bear steepened to -41.164 high compared to -57.943 low overnight.

- Heavy volumes (TYZ2>2M after the bell) included buy-stops, several rounds of technical selling (TYZ2 slipped below 112-25+ Low Jun 11 2009), curve flattener unwinds/profit taking in the aftermath of Wed's post-FOMC flattening. Modest deal-tied flow and pre-auction short sets ahead final leg of wk's Tsy supply ($15B 10Y TIPS R/O) contributed to moves.

- Brief delayed reaction to BoE rate hike with long end Gilts under heavy pressure, Tsys followed suit while Tsys extending session lows (30YY taps 3.5241% high) following latest weekly claims of 213k vs. 217k est, prior revised to 208k.

- What really turned up the heat on long end selling were unconfirmed rumors of Japan FinMin selling Tsys to support FX intervention (after similar occurred after after PBoC intervened in 2015, one desk said). Some desks questioned the logic of selling Tsys while yield curve control is still occurring.

- Nevertheless, MOF intervention was confirmed selling US$ as well as Tsys to lesser degree -- What exacerbated the sell-off were speculative and fast$ accts selling bonds in anticipation of more intervention, trading desks said.

- Currently, 2-Yr yield is up 7bps at 4.118%, 5-Yr is up 15.2bps at 3.9183%, 10-Yr is up 17bps at 3.6999%, and 30-Yr is up 13.4bps at 3.6366%.

OVERNIGHT DATA

- US JOBLESS CLAIMS +5K TO 213K IN SEP 17 WK

- US PREV JOBLESS CLAIMS REVISED TO 208K IN SEP 10 WK

- US CONTINUING CLAIMS -0.022M to 1.379M IN SEP 10 WK

- US Q2 CURRENT ACCOUNT GAP -$251.1

- US Q1 CURRENT ACCOUNT REVISED TO -$282.5

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 22.47 points (-0.07%) at 30163.82

- S&P E-Mini Future down 24.5 points (-0.64%) at 3781.75

- Nasdaq down 144.4 points (-1.3%) at 11075.44

- US 10-Yr yield is up 17 bps at 3.6999%

- US Dec 10Y are down 46.5/32 at 112-25

- EURUSD down 0.0002 (-0.02%) at 0.9835

- USDJPY down 1.64 (-1.14%) at 142.43

- Gold is down $2.48 (-0.15%) at $1671.51

- EuroStoxx 50 down 64.73 points (-1.85%) at 3427.14

- FTSE 100 down 78.12 points (-1.08%) at 7159.52

- German DAX down 235.52 points (-1.84%) at 12531.63

- French CAC 40 down 112.83 points (-1.87%) at 5918.5

US TSY FUTURES CLOSE

- 3M10Y +21.608, 44.93 (L: 19.61 / H: 45.304)

- 2Y10Y +10.032, -42.25 (L: -57.943 / H: -41.164)

- 2Y30Y +6.35, -48.686 (L: -63.464 / H: -46.919)

- 5Y30Y -2.053, -28.62 (L: -33.827 / H: -25.521)

- Current futures levels:

- Dec 2Y down 10.125/32 at 102-25.625 (L: 102-24.125 / H: 102-31.625)

- Dec 5Y down 30.75/32 at 107-28.75 (L: 107-25 / H: 108-19)

- Dec 10Y down 1-15/32 at 112-24.5 (L: 112-21.5 / H: 114-00)

- Dec 30Y down 2-03/32 at 128-07 (L: 128-01 / H: 131-00)

- Dec Ultra 30Y down 3-03/32 at 140-03 (L: 139-23 / H: 144-12)

US EURODOLLAR FUTURES CLOSE

- Dec 22 -0.050 at 95.305

- Mar 23 -0.140 at 95.110

- Jun 23 -0.160 at 95.135

- Sep 23 -0.175 at 95.285

- Red Pack (Dec 23-Sep 24) -0.185 to -0.17

- Green Pack (Dec 24-Sep 25) -0.21 to -0.18

- Blue Pack (Dec 25-Sep 26) -0.21 to -0.21

- Gold Pack (Dec 26-Sep 27) -0.205 to -0.18

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.75200 to 3.07171% (+0.75614/wk)

- 1M +0.02500 to 3.08400% (+0.07014/wk)

- 3M +0.03757 to 3.64143% (+0.07614/wk) * / **

- 6M +0.05871 to 4.18271% (+0.05942/wk)

- 12M +0.11714 to 4.79957% (+0.12743/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.64143% on 9/22/22

- Daily Effective Fed Funds Rate: 2.33% volume: $99B

- Daily Overnight Bank Funding Rate: 2.32% volume: $300B

- Secured Overnight Financing Rate (SOFR): 2.26%, $951B

- Broad General Collateral Rate (BGCR): 2.25%, $393B

- Tri-Party General Collateral Rate (TGCR): 2.25%, $374B

- (rate, volume levels reflect prior session)

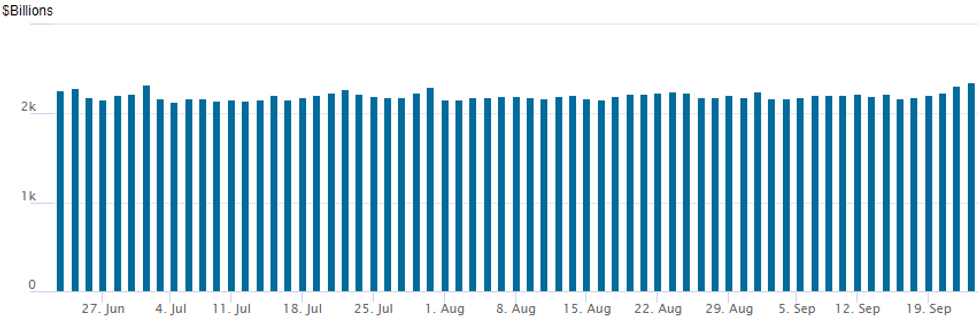

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usages climbs to new record high of $2,359.227B w/ 102 counterparties vs. $2,315.900B prior session. Compares to prior record high of $2,329.743B from Thursday June 30.

PIPELINE: $2.75B Citigroup 4NC3 Launched

- Date $MM Issuer (Priced *, Launch #)

- 09/22 $2.75B #Citigroup 4NC3 +148

- 09/22 $900M #WEC Energy $500M 3Y +90, $400M 5Y +128

- 09/22 $Benchmark JBIC 5Y Green bond investor call

- 09/22 $2B Royal Caribbean 6.25NC2.5 investor call

EGBs-GILTS CASH CLOSE: Gilts Underperform In Disorderly Session

Global core bond yields rose further Thursday, in increasingly disorderly fashion.

- The hawkish Fed guidance late Wednesday continued to reverberate, with volatility exacerbated by big swings in multiple currencies early Thursday including the Swiss franc and the Japanese yen - the latter of which saw official intervention in support for the first time since 1998.

- Despite a 50bp vs 75bp hike by the BoE, Gilts underperformed, with yields rising in double-digits across the curve following the Bank following through with Gilt sales starting in October.

- Additionally, Friday sees an updated UK fiscal statement, with some government measures seen driving Gilt weakness.

- Bund yields broke through the 2014 highs; futures saw breaks of support across the board.

- Against that backdrop, and despite a risk-off atmosphere, periphery spreads found opportunity to tighten.

- In addition to the UK fiscal announcement, we get preliminary PMI data Friday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 8.7bps at 1.846%, 5-Yr is up 9.7bps at 1.936%, 10-Yr is up 7.2bps at 1.965%, and 30-Yr is up 3.2bps at 1.87%.

- UK: The 2-Yr yield is up 13.8bps at 3.528%, 5-Yr is up 18.3bps at 3.563%, 10-Yr is up 18.4bps at 3.495%, and 30-Yr is up 18.6bps at 3.775%.

- Italian BTP spread down 3.8bps at 220.4bps / Greek down 3.4bps at 253.5bps

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/09/2022 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 23/09/2022 | 0715/0915 | ** |  | FR | IHS Markit Services PMI (p) |

| 23/09/2022 | 0715/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 23/09/2022 | 0730/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 23/09/2022 | 0730/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 23/09/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 23/09/2022 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 23/09/2022 | 0800/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 23/09/2022 | 0830/0930 | *** | | UK | IHS Markit Manufacturing PMI (flash) |

| 23/09/2022 | 0830/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 23/09/2022 | 0830/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 23/09/2022 | 1000/1100 | ** | | UK | CBI Distributive Trades |

| 23/09/2022 | 1230/0830 | ** |  | CA | Retail Trade |

| 23/09/2022 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (flash) |

| 23/09/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 23/09/2022 | 1800/1400 | | US | Fed Listens Event |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.