Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI FED BRIEF: Williams Is Confident Fed Getting Inflation Back To 2%

- MNI US: SCOTUS Partially Backs Trump On Immunity

- MNI US DATA: US PMI Sees Slowest Selling Price Increases In YTD

- MNI US Data: A Small Miss For ISM Mfg, Prices Paid Continue Reversal

US

FED BRIEF (MNI): Williams Is Confident Fed Getting Inflation Back To 2%

Federal Reserve Bank of New York President John Williams said he continues to believe prices are moderating and on a path back to the levels targeted by the central bank, according to video remarks released Monday. "I'm confident that we at the Fed are on a path to achieving our 2% inflation goal on a sustained basis," said Williams, in a Bank for International Settlements panel.

- William's remarks came Sunday and were released in a video by the BIS Monday. The panel discussion among global policymakers focused on central bank frameworks and principles. Williams said: "We didn't see these events coming -- the war, the pandemic -- but the frameworks and the foundations we put in place beforehand were the things that actually served us incredibly well."

NEWS

US (MNI): SCOTUS Partially Backs Trump On Immunity:

The Supreme Court of the United States (SCOTUS) has issued a ruling stating that former President Donald Trump has absolute immunity for any criminal charges related to official acts when he was president, but no immunity from unofficial acts. Focus will now turn to which acts around the 2020 election are deemed to be in Trump's capacity as then-president, and which are deemed unofficial acts.

US (MNI): Biden Allies Seize On SCOTUS Immunity Ruling To Bolster Campaign

President Biden's campaign, and senior Democrats, have issued statements condemning the United States Supreme Court for ruling that former President Donald Trump should be granted partial immunity for offenses committed while in office.

(BBG) ECB’s Wunsch Would Need Convincing for More Than Two 2024 Cuts

European Central Bank Governing Council member Pierre Wunsch would need to be thoroughly convinced that inflation was headed back to the 2% target in order for him to back more than two reductions in interest rates this year.

SECURITY (MNI): Netanyahu: Israel Nearing End Phase Of Eliminating Hamas

Wires carrying comments from Israeli Prime Minister Benjamin Netanyahu stating that Israel is, "nearing the end of phase of eliminating Hamas military capabilities," and will "continue to destroy the remnants of Hamas military."

US Tsys Carry-Over Weakness Ahead Headline Jobs Data, Shortened Holiday Week

- Treasuries remained under pressure late Monday, US rate initially followed EGBs as French election risk premium is unwound.

- Futures marched lower since ISM mfg and prices paid miss, while MFG PMI was revised down fractionally in the final June release to leave a still modest increase to 51.6 (cons & prelim 51.7) after 51.3 in May.

- Other factors at play include carry-over month end positioning since Tsys reversed early support last Friday. Curve flattener unwound, while rate cut pricing cools.

- Sep'24 10Y futures neared key support of 109-00+ (Jun 10 low), trading 109-05 (-26.5) vs. 109-02.5 low. 10Y yield taps 4.4991% high (+.1031), curves steeper: 2s10s +6.634 at -29.312 (May 3 levels).

- Rather subdued trade despite the heavier volumes (TYU4>1.96M), focus on central bank conference in Sintra tomorrow, Fed Chair Powell, Lagarde and Campos Neto speaking at appr 0900ET.

- Light data tomorrow picks up Wednesday with ADP private employment numbers, ISM services, and weekly claims as markets are closed for 4th of July holiday Thursday. Friday headline data risk: June employment data.

OVERNIGHT DATA

US DATA (MNI): A Small Miss For ISM Mfg, Prices Paid Continue Reversal

The ISM manufacturing was modestly softer than expected in June at 48.5 (cons 49.1) for little change from 48.7 in May. Prices paid offered the most notable miss, falling to 52.1 (cons 55.9) after 57.0 for technically its lowest since December. This series has seen some large swings recently, jumping from 52.5 in Feb to 60.9 over two months, only to then fully reverse the climb over the next two months.

- Employment also disappointed at 49.3 (cons 50.0) after 51.1, rolling back into contraction territory after a single month above 50 after a 5.2pt increase from the 45.9 in Feb.

- New orders were the only main metric that surprised positively compared to expectations, although at 49.3 (cons 49.0) after 45.4 it’s similar to the rebound that was expected. It’s nevertheless a third sub-50 month after what proved two short-lived months above 50 in Q1.

- However, with inventories falling further to 45.4, the new orders to inventories measure increased to +3.9 for its highest since February which bodes a little better for future activity.

- Wednesday’s ISM services for June will be watched more closely after its surprise jump to 53.8 in March.

US DATA (MNI): US PMI Sees Slowest Selling Price Increases In YTD

The manufacturing PMI was revised down fractionally in the final June release to leave a still modest increase to 51.6 (cons & prelim 51.7) after 51.3 in May.

- From the S&P Global press release (full here): “The most positive aspect of the latest survey was the fastest increase in employment since September 2022.”

- "Although input costs continued to rise sharply, the rate of inflation eased in June, while selling prices increased at the slowest pace in the year-to-date."

- “Where charges were raised, this reflected the passing on of higher input costs to clients. On the other hand, some firms lowered selling prices as part of efforts to remain competitive”

- “Business confidence has consequently fallen to the lowest for 19 months, suggesting the manufacturing sector is bracing itself for further tough times in the coming months.”

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA up 27.83 points (0.07%) at 39147.51

- S&P E-Mini Future up 6.25 points (0.11%) at 5528

- Nasdaq up 111.2 points (0.6%) at 17844.51

- US 10-Yr yield is up 8.3 bps at 4.4791%

- US Sep 10-Yr futures are down 26/32 at 109-5.5

- EURUSD up 0.0024 (0.22%) at 1.0737

- USDJPY up 0.61 (0.38%) at 161.49

- WTI Crude Oil (front-month) up $2.03 (2.49%) at $83.55

- Gold is up $3.04 (0.13%) at $2329.91

- European bourses closing levels:

- EuroStoxx 50 up 35.97 points (0.74%) at 4929.99

- FTSE 100 up 2.64 points (0.03%) at 8166.76

- German DAX up 55.21 points (0.3%) at 18290.66

- French CAC 40 up 81.73 points (1.09%) at 7561.13

US TREASURY FUTURES CLOSE

- 3M10Y +7.866, -88.538 (L: -99.665 / H: -87.346)

- 2Y10Y +7.05, -28.896 (L: -35.312 / H: -28.896)

- 2Y30Y +7.232, -12.495 (L: -19.31 / H: -12.398)

- 5Y30Y +2.477, 20.476 (L: 17.498 / H: 20.689)

- Current futures levels:

- Sep 2-Yr futures down 3.375/32 at 102-0.125 (L: 101-30.875 / H: 102-03)

- Sep 5-Yr futures down 14.75/32 at 106-3.75 (L: 106-01.75 / H: 106-14.75)

- Sep 10-Yr futures down 26/32 at 109-5.5 (L: 109-02.5 / H: 109-24)

- Sep 30-Yr futures down 2-07/32 at 116-03 (L: 115-30 / H: 117-18)

- Sep Ultra futures down 2-31/32 at 122-12 (L: 122-05 / H: 124-08)

US 10YR FUTURE TECHS: (U4) Retracement Mode

- RES 4: 111-31 1.382 proj of the Apr 25 - May 16 - 29 price swing

- RES 3: 111-17+ 1.236 proj of the Apr 25 - May 16 - 29 price swing

- RES 2: 111-13 High Mar 25

- RES 1: 110-16/111-01 High Jun 28 / 14 and the bull trigger

- PRICE: 109-05 @ 16:44 BST Jul 1

- SUP 1: 109-03+/109-00+ Intraday low / Low Jun 10 and key support

- SUP 2: 108-27+ Low Jun 3

- SUP 3: 108-1+ Trendline drawn from the Apr low

- SUP 4: 107-31 Low May 29 and a key support

A bull cycle in Treasuries remains in play, with the pullback that started Jun 14, appearing to be corrective in nature. However, the contract has traded through the 50-day EMA - at 109.27. This signals scope for a deeper retracement and has opened 109-00+, the Jun 10 low. For bulls, a resumption of gains and a break of 111-01, the Jun 14 high, would resume the uptrend and open 111-17+, a Fibonacci projection. Initial resistance is 110-16, Friday’s high.

SOFR FUTURES CLOSE

- Sep 24 steady at 94.850

- Dec 24 -0.015 at 95.130

- Mar 25 -0.040 at 95.395

- Jun 25 -0.065 at 95.620

- Red Pack (Sep 25-Jun 26) -0.12 to -0.08

- Green Pack (Sep 26-Jun 27) -0.15 to -0.135

- Blue Pack (Sep 27-Jun 28) -0.16 to -0.155

- Gold Pack (Sep 28-Jun 29) -0.165 to -0.165

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00297 to 5.33420 (-0.00806 total last wk)

- 3M -0.00371 to 5.32089 (-0.01795 total last wk)

- 6M -0.00666 to 5.24805 (-0.02087 total last wk)

- 12M -0.01429 to 5.02575 (-0.01161 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.33% (-0.01), volume: $2.024T

- Broad General Collateral Rate (BGCR): 5.32% (+0.00), volume: $706B

- Tri-Party General Collateral Rate (TGCR): 5.32% (+0.00), volume: $682B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $67B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $157B

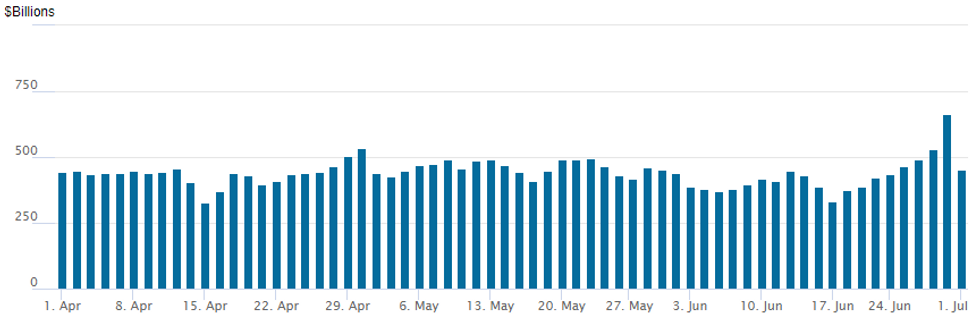

FED Reverse Repo Operation

NY Federal Reserve/MNI

RRP usage gaps below $500M to $451.783B vs. $664.570B last Friday when moth/quarter end usage pushed figure to highest level since January 10; number of counterparties falls back to 67 from 95 prior. Today's usage compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

PIPELINE

- Date $MM Issuer (Priced *, Launch #)

- 7/1 $3.5B BGK 10Y +140, 30Y +165

- 7/2 $Benchmark EIB 7Y SOFR+48 may issue Tuesday

EGBs-GILTS CASH CLOSE: Bunds Weaken As Political Risk Premium Dissipates

Core European instruments weakened sharply Monday, as political risk premia dissipated somewhat.

- OATs and periphery EGBs enjoyed some respite at the open after Sunday's French first-round elections went largely as expected, with the far-right RN winning the most seats but likely falling short of an absolute majority.

- German flash June inflation data was largely in line with expectations, with services CPI remaining relatively sticky but headline and overall core ticking lower.

- On the day, yields rose across all European curves, and closed near session highs.

- Both the German and UK curves bear steepened. 10Y OAT/Bund spreads fell 6bp to 74.1bp, the tightest level in over two weeks. Periphery EGB spreads tightened sharply, with BTP and GGBs narrowing over 7bp to Bunds.

- Tuesday's schedule includes the Eurozone-wide June flash HICP print (MNI sees modest downside risks to the 2.5% consensus headline expectation) and final PMIs, as well as ECB and other speakers at the Sintra forum.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 9.1bps at 2.924%, 5-Yr is up 10.6bps at 2.588%, 10-Yr is up 10.7bps at 2.607%, and 30-Yr is up 10.4bps at 2.795%.

- UK: The 2-Yr yield is down 2.3bps at 4.198%, 5-Yr is up 8.6bps at 4.11%, 10-Yr is up 10.9bps at 4.281%, and 30-Yr is up 11.6bps at 4.775%.

- Italian BTP spread down 7.4bps at 149.8bps / Greek down 7.8bps at 117.5bps

FOREX: Greenback Resilient to Softer US Data, JPY and CHF Pressured

- Higher core yields and the associated widening of yield differentials place specific pressure on the Japanese Yen and Swiss Franc on Monday. As such, USDJPY momentum has built above the 161 handle, briefly printing a new multi-decade high of 161.73. Elsewhere, EURCHF is seen as one of the best performing crosses to start the week, rising 0.72% back to 0.9700.

- In similar vein, and assisted by the initially firmer risk backdrop, AUD/JPY traded a higher high for a tenth consecutive session. Such a streak has only occurred a handful of times since the Global Financial Crisis and another higher high tomorrow would be the longest winning streak for the cross since 2011. Price has cleared 107.50 to touch the highest level since 2007 today.

- Softer-than expected US manufacturing data, and in particular the prices paid component, offered only very brief pressure on the greenback, before a strong reversal higher which persists as we approach the APAC crossover.

- This helped EURUSD a little lower across the session, which had previously been buoyed early Monday following the first-round results of the French election and a moderate reduction of political risk premium. Resistance at the 1.0777 (50-dma) has contained the rally well so far and trades around 1.0730 at typing.

- RBA minutes kick off the Tuesday calendar before Eurozone inflation will highlight the European session. Fed Chair Powell is due to participate in a panel discussion titled "Policy panel" at the ECB Forum on Central Banking, in Sintra. JOLTS job openings data highlights the data calendar in the US.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/07/2024 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 02/07/2024 | 0130/1130 |  | AU | RBA Minutes | |

| 02/07/2024 | 0730/0930 |  | EU | ECB's De Guindos chairing session on inflation | |

| 02/07/2024 | 0830/1030 | | EU | ECB's Elderson chairs session on biodiversity | |

| 02/07/2024 | 0900/1100 | *** | | EU | HICP (p) |

| 02/07/2024 | 0900/1100 | ** | | EU | Unemployment |

| 02/07/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 02/07/2024 | 1030/1230 | | EU | ECB's Schnabel chairing panel on Geopolitical shock and inflation | |

| 02/07/2024 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 02/07/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 02/07/2024 | 1330/1530 | | EU | ECB's Lagarde in policy panel at ECB forum | |

| 02/07/2024 | 1330/0930 | | US | Fed Chair Jerome Powell | |

| 02/07/2024 | 1400/1000 | *** | | US | JOLTS jobs opening level |

| 02/07/2024 | 1400/1000 | *** | | US | JOLTS quits Rate |

| 02/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.