Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- MNI POLICY: Fed Loosens Main Street Loan Terms After Criticism

- MNI EXCLUSIVE: UK Draft Bill Not Block On EU State Aid Deal

- MNI EXCLUSIVE: No China GDP Target But Still Need 5-6% Growth

- MNI SOURCE: Breakthrough Seen On ESM Reform at 30 Nov. Meeting

- MNI BRIEF: Biden Would Seek Sizeable Stimulus Immediately-Aide

- MCCONNELL SAYS ANOTHER STIMULUS POSSIBLE IF GOP KEEPS SENATE, Bbg

- BELGIUM IMPOSES LOCKDOWN TO AVERT HEALTH-CARE SYSTEM COLLAPSE, Bbg

US

FED: The Federal Reserve on Friday expanded access to its Main Street Lending Program, following months of complaints from business owners and lawmakers that it was too restrictive. The minimum loan now will be $100,000, compared with $250,000 previously, and fees have been adjusted to encourage the provision of smaller loans. For more see 10/30 main wire at 1106ET.

US: Presidential contender Joe Biden if elected would immediately consult with Capitol Hill to achieve a "sizeable" stimulus immediately after inauguration on Jan. 20, Biden top policy advisor Stef Feldman said Friday.- A Biden administration would seek two separate stimulus packages with one aimed at "short-term relief" that could amount to $3T focused on small businesses and minorities, Feldman said. A second package aimed at "longer-term relief" would come later on and focus on infrastructure and green proposals, Feldman said, not ruling out that it could cost around USD1 trillion.

- Biden also would not wait to work with Capitol Hill to raise taxes on those making over $400,000 per year and seek to raise corporate taxes to 28% from the current 21% rate in order to completely pay for the "longer-term relief" proposal in full without deficit spending, Feldman said during an Axios event.

EUROPE

UK: Large chunks of the UK's draft Internal Market Bill (UKIM) could easily be amended or even shelved in order to facilitate a trade deal with the European Union, removing a potential stumbling block lawmakers and parliamentary experts told MNI. For more see 10/30 main wire at 1127ET.

EU: A compromise is being crafted which should bridge a north-south stand-off between member states which is blocking reform of the EU bail-out fund, improving the prospects of a breakthrough at the Nov. 30 meeting of euro zone finance ministers, a well-placed EU official has disclosed to MNI. For more see 10/30 main wire at 1209ET.

ASIA

CHINA: China still needs GDP growth of more than 5% a year from 2021 to 2025 to support employment and quality development, policy advisors in Beijing insist, despite the latest plenum of the Communist Party eschewing a specific growth rate for the next-five-year plan after the annual target was dropped this year amid Covid uncertainty.

OVERNIGHT DATA

US DATA: September Personal Income +0.9%; PCE +1.4%

- U.S. personal income climbed higher in September, rising by 0.9% following a sharp 2.5% decline in August, according to figures released Friday by the Bureau of Economic Analysis. Financial markets had expected personal income to rise by 0.4%.

- That increase mainly reflected increases in proprietors' income, compensation of employees, and rental income that was partially offset by a decline in government social benefits, the BEA said.

- Unemployment insurance benefits fell in September while other social benefits increased, according to the BEA. That was primarily due to the expiration of an added USD600 per week on top of regular state benefits.

- PCE grew by 1.4% in September after a 1.0% gain in August. That was driven by a USD109.9B increase in spending on goods, namely clothing, footwear, and new motor vehicles. A smaller increase in services spending mainly reflected increases in health care spending and recreation services like membership clubs, sports centers, and theaters.

- The PCE price index was up 0.2% in September following a 0.3% increase in August. Excluding food and energy, the core PCE price index was also up 0.2% in September, in line with market expectations.

- From a year earlier, the PCE price index was up 1.4%, while the core PCE price index was up 1.5%.

US DATA: MNI Chicago Business Barometer Eased in Sep

- MNI CHICAGO BUSINESS BAROMETER 61.1 OCT VS 62.4 SEP

- MNI CHICAGO BUSINESS BAROMETER: FOURTH CONSECUTIVE READING ABOVE 50-MARK

- MNI CHICAGO PRODUCTION SHOWED LARGEST M/M DECLINE

- MNI CHICAGO NEW ORDERS ONLY MAJOR CATEGORY TO SHOW A M/M RISE

- The Chicago Business Barometer edged lower by 1.3pt in Oct after Sep's sharp increase.

- Nevertheless, this marks the fourth consecutive reading in expansion territory after having registered below the 50-mark for a whole year.

- Among the five main indicators, New Orders (65.0) was the only category to show a small m/m uptick, while Production recorded the largest decline, slipping 5.9pt to 62.1.

- Order Backlogs dropped to 50.5, while Employment fell to 43.2, showing the sixteenth consecutive sub-50 reading.

- Employment is the only main category which registered below the 50-mark in Oct.

- Supplier Deliveries decreased 2.1pt to 65.3, showing a two-month low, while Inventories and Prices remained broadly unchanged at 47.7 and 64.6, respectively, both down only 0.1pt.

- The majority of respondents (45.8%) were unsure if working remotely could be a permanent option for their employees after the crisis, while 35.6% were not planning to make it a permanent option.

- Companies provided a mixed picture regarding the recovery with some firms noting a drop in demand, while others saw a stable level of orders and production or a gradual improvement in business activity.

MICHIGAN FINAL OCT. CONSUMER SENTIMENT AT 81.8; EST. 81.2

St. Louis Fed Real GDP Nowcast Model Sees U.S. Q3 GDP at 19.5%

- CANADA SEP INDUSTRIAL PRICES -0.1% MOM; EX-ENERGY +0.3%

- CANADA SEP RAW MATERIALS PRICES -2.2% MOM; EX-ENERGY +0.3%

- CANADA AUG GROSS DOMESTIC PRODUCT +1.2% MOM

- CANADA GOODS INDUSTRY GDP +0.5%, SERVICES +1.5%

- CANADA AUG BUDGET DEFICIT CAD21.9B VS. YEAR AGO CAD3.7B

- CANADA AUG BUDGET DEFICIT CAD21.9B VS. YEAR AGO CAD3.7B

- CANADA APR-AUG DEFICIT CAD170.5 BLN VS PRIOR CAD5.2 BLN

- CANADA FINANCE DEPT: DEFICIT CONSISTENT WITH JUL FISCAL UPDATE

- CANADA APR-AUG REVENUE -29% YOY, PROGRAM SPENDING +97%

- CANADA APR-AUG FINANCIAL REQUIREMENT CAD223B VS PRIOR CAD16B

- CANADA GOVT AUG CASH BALANCE CAD129B, +CAD85B FROM MARCH

MARKETS SNAPSHOT

- DJIA down 401.43 points (-1.51%) at 26659.11

- S&P E-Mini Future down 64.5 points (-1.95%) at 3272.75

- Nasdaq down 329.1 points (-2.9%) at 11185.59

- US 10-Yr yield is up 3.4 bps at 0.8568%

- US Dec 10Y are down 5.5/32 at 138-7.5

- EURUSD down 0.0029 (-0.25%) at 1.167

- USDJPY up 0.05 (0.05%) at 104.41

- WTI Crude Oil (front-month) down $0.59 (-1.63%) at $35.85

- Gold is up $12.44 (0.67%) at $1874.50

- European bourses closing levels:

- EuroStoxx 50 down 1.82 points (-0.06%) at 2955.45

- FTSE 100 down 4.48 points (-0.08%) at 5562.7

- German DAX down 41.59 points (-0.36%) at 11553.89

- French CAC 40 up 24.57 points (0.54%) at 4574.95

US TSY FUTURES: Late Volume Surge, Tsys Gap Lower Into Mnth-End

Tsy futures reversed early strength, ground lower soon after the open to trade weaker across the curve after the closing bell bell: extending session lows amid late month-end duration shedding and position squaring ahead next week's presidential election.

- Heavy volumes for an otherwise quiet end to the week, TYZ>2.2M. massive duration selling after the bell with 500k TYZ traded over 30 minute period from 138-09 to 138-03.5 (session low).

- Tsys were well bid after stronger than expected income (+0.9% vs. 0.4% exp) and spending (1.4% vs. +1.0% exp) data but inflation weaker than expected (1.5% vs. 1.7%). Not much of a react to MNI Chicago Business Barometer: 61.1 vs. 62.4 last month.

- Talk of risk-parity fund unwinds also made the rounds again as Tsys and equities sold off in tandem.

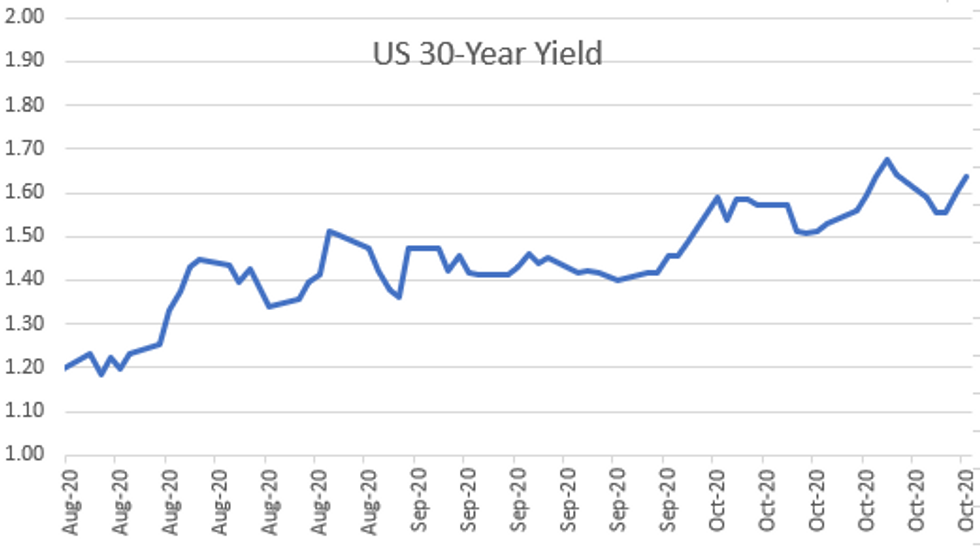

- The 2-Yr yield is up 0.6bps at 0.1525%, 5-Yr is up 1bps at 0.3796%, 10-Yr is up 3.9bps at 0.8619%, and 30-Yr is up 4.4bps at 1.6459%.

US TSY FUTURES CLOSE:

Trading weaker across the curve after the bell

- 3M10Y +4.399, 77.546 (L: 70.124 / H: 78.222)

- 2Y10Y +4.203, 71.254 (L: 65.444 / H: 71.734)

- 2Y30Y +4.554, 149.496 (L: 143.228 / H: 150.339)

- 5Y30Y +3.481, 126.502 (L: 122.409 / H: 127.384)

- Current futures levels:

- Dec 2Y steady at 110-13.5 (L: 110-13.25 / H: 110-13.75)

- Dec 5Y down 1.75/32 at 125-19 (L: 125-18.5 / H: 125-23)

- Dec 10Y down 8/32 at 138-5 (L: 138-03.5 / H: 138-19.5)

- Dec 30Y down 20/32 at 172-7 (L: 172-00 / H: 173-19)

- Dec Ultra 30Y down 1-3/32 at 214-14 (L: 213-31 / H: 217-09)

US EURODLR FUTURES CLOSE

Steady to modestly lower out the strip; lead quarterly EDZ0 unchanged since 3M LIBOR set' +0.00137 to 0.21575% (-0.00075/wk).

- Dec 20 steady at 99.760

- Mar 21 -0.005 at 99.790

- Jun 21 -0.005 at 99.80

- Sep 21 -0.005 at 99.80

- Red Pack (Dec 21-Sep 22) -0.01 to -0.005

- Green Pack (Dec 22-Sep 23) -0.015 to -0.01

- Blue Pack (Dec 23-Sep 24) -0.025 to -0.015

- Gold Pack (Dec 24-Sep 25) -0.04 to -0.025

US DOLLAR LIBOR: Latest settles

- O/N +0.00038 at 0.08138% (+0.00000/wk)

- 1 Month -0.00888 to 0.14025% (-0.01513/wk)

- 3 Month +0.00137 to 0.21575% (-0.00075/wk)

- 6 Month -0.00075 to 0.24213% (-0.00725/wk)

- 1 Year -0.00087 to 0.33013% (-0.00650/wk)

US TSYS: Short Term Rates

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $59B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $172B

- Secured Overnight Financing Rate (SOFR): 0.09%, $866B

- Broad General Collateral Rate (BGCR): 0.06%, $329B

- Tri-Party General Collateral Rate (TGCR): 0.06%, $306B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.201B accepted vs. $3.538B submission

- Next week's scheduled purchases:

- Mon 11/02 1100-1120ET: Tsy 20Y-30Y, appr $1.750B

- Tue 11/03 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Fri 11/06 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

PIPELINE: $111.65B Total High-Grade Issuance For October

- Date $MM Issuer (Priced *, Launch #)

- 11/?? $Benchmark Industrial Bank HK 3Y +145a

- 11/?? $Benchmark State Development & Inv 5Y +160a

- -

- $8.8B Priced Thursday; $111.65B/month

- 10/29 $4.9B *Boeing 4pt: $1B +3Y +180, $1.4B +5Y +240, $1.1B +7Y +265, $1.4B +10Y +280a (issued $25B via 7pt jumbo on April 30: $3B 3Y +425, +450: $3.5B 5Y, $2B 7Y, $4.5B 10Y and $5.5B 30Y, $3B 20Y +440, $3.5B 40Y +462.5)

- 10/29 $1.5B *Philip Morris $750M +5Y +58, $750M 10Y +103 (issued $2.25B on Apr 29: $750M each 3Y +100, 5Y +125 and 10Y +155)

- 10/29 $750M *Stanley Black & Decker 30Y +112.5

- 10/29 $650M *Baxter Int WNG 10Y +90

- 10/29 $500M *Swedish Export Credit Corporation (SEK) 2Y +5

- 10/29 $500M *IFFIm 3Y Red S vaccine bond +16

FOREX: DXY Caps Strongest Week in Six

EUR/GBP closed in on the lowest levels for nearly two months, with the cross narrowing the gap with the 200-dma at 0.8906 into the Friday close. Signs of further progress made between EU and UK negotiators are making the prospects for a deal before November 15th more likely, and helping GBP find support on dips.

- USD demand into the October month-end fix put most major pairs under pressure into the close, but this swiftly dissipated once the orders were absorbed.

- This was less evident in the EUR, however, which shrugged off strong French, Italian, German and Spanish GDP data, taking heed of Lagarde's communications at the ECB press conference Thursday that the bank are likely to 'recalibrate' policy in December. This helped the greenback secure the best weekly performance in six.

- It's difficult to play down the importance of numerous risk events in the coming week, with the Presidential election, FOMC rate decision and Nonfarm Payrolls report all to contend with. Rate decisions from the RBA, BoE and Norges Bank are also due.

EGBs-GILTS CASH CLOSE: Gilts Bear Steepen, BTP Spreads Widen

The last trading day of October saw Gilt yields rise in a bear steepening motion, with Bunds mixed and Italian spreads widening sharply. The latter contrasted with the rest of the periphery, which saw tightening spreads.

- Little reaction to this morning's above-expected GDP figures across the board, with more attention on the December delivery of action from Thursday's dovish ECB meeting, and of course the negative economic impact of lockdowns across Europe.

- Focus next week will be on the BoE and FOMC meetings, not to mention the US election.

- Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is up 1.5bps at -0.794%, 5-Yr is up 1.2bps at -0.82%, 10-Yr is up 0.9bps at -0.627%, and 30-Yr is up 0.6bps at -0.218%

- UK: The 2-Yr yield is up 2.5bps at -0.032%, 5-Yr is up 2.9bps at -0.038%, 10-Yr is up 4.1bps at 0.262%, and 30-Yr is up 6.4bps at 0.831%.

- Italian BTP spread up 5.9bps at 138.7bps

- Spanish bond spread down 0.7bps at 76.2bps

- Portuguese PGB spread down 0.8bps at 73.2bps

- Greek bond spread down 1.3bps at 157.6bps

UP TODAY

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.