Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: Prudent For Fed To Hike Another 50-100BP - Reis

- MNI BRIEF: Daly Says Fed Has Work Left, Undecided On Hike

- Initial Jobless Claims Climb With Outsized Ohio Impact

- MNI US CPI: Further Moderation In Core Goods Ex Used Cars

US

FED: The Federal Reserve could soon decide to cease interest rate hikes and keep them elevated for a prolonged period but it would probably be better for policymakers to raise them further to make sure they quash inflation in a timely manner, Ricardo Reis, an academic consultant to the Federal Reserve Bank of Richmond, told MNI.

- Reis said more hikes would ensure the central bank keeps expectations anchored in the face of an inflation outlook that is improving gradually but still leaves underlying price pressures well above the Fed’s 2% target, a situation which threatens policymakers’ credibility.

- It would also allow rate cuts sooner than a policy that maintains the fed funds rate in the current 5.25%-5.5% range for a prolonged period in order to achieve passive tightening as inflation falls further. For more see MNI Policy main wire at 1125ET.

FED: San Francisco Fed President Mary Daly said Thursday that while inflation and job growth are coming down as expected, more work remains to balance the economy and she wants more evidence before deciding about whether to raise interest rates further.

- “Inflation is coming down, but it’s still too high,” she told Yahoo! Finance. The CPI report out today is consistent with the gradual slowdown predicted by the Fed, she said. She made a similar point about recent job reports, saying that while hiring is slowing monthly gains around 200,000 are double what's considered sustainable.

- "I see slowing in the economy, but not there yet, and that’s what my contacts across the district tell me," Daly said. “Yes the economy is slowing down, it’s less frenzied, but boy it’s still hard to find workers.”

- The Fed has "more work to do," Daly said, adding she hasn't decided yet on whether to support another rate hike next month or how she will fill out her economic forecast. Officials are still figuring out if policy is "sufficiently restrictive," she said. She also suggested the Fed could keep rates at their peak for longer and doesn't see conversations about potential cuts until next year.

US TSYS Yields Higher Despite Dip in Core CPI, PPI Up Next

- Treasury futures finishing near late session lows after initially gapping to session highs (TYU3 tapped 111-29) following this morning's July CPI: core MoM 0.16% vs. 0.2% est. Core goods deflation accelerated to -0.33% M/M from -0.05% M/M.

- The drag from used vehicles was at the low end of expectations seen beforehand, at -1.34% M/M vs analysts averaging circa -2% (ranging from -1.3% to -3.2%) after -0.45% M/M. There should be further declines in the pipeline. However, more notable from the goods side was core goods ex used vehicles printing -0.18% M/M after two 0.00% M/M readings.

- Initial jobless claims disappointed as they surprisingly increased to 248k (cons 230k) after an unrevised 227k, for its largest weekly increase since early June.

- Fed pricing comes off post-CPI session lows but only just with SF Fed’s Daly (’24 voter) noting the Fed still has more work to do and that the CPI data was largely as expected and that it doesn’t say ‘victory is ours’ on inflation.

- Daly added the Fed is yet to determine whether to raise and how long to hold rates, with Daly being data dependent and it premature to decide on another hike. There is a lot more info coming in before the September meeting and before year-end.

- Delayed reaction, Treasury futures traded weaker after $23B 30Y auction (912810TT5) tailed with 4.189% high yield vs. 4.175% WI; 2.42x bid-to-cover vs. 2.43x in the prior month.

OVERNIGHT DATA

US JUL CPI 0.2%, CORE 0.2%; CPI Y/Y 3.2%, CORE Y/Y 4.7%

US JUL ENERGY PRICES 0.1%

US JUL OWNERS' EQUIVALENT RENT PRICES 0.5%

US JUL CPI UNROUNDED M/M 0.167%, CORE 0.160%

- Core goods deflation accelerated to -0.33% M/M from -0.05% M/M.

- The drag from used vehicles was at the low end of expectations seen beforehand, at -1.34% M/M vs analysts averaging circa -2% (ranging from -1.3% to -3.2%) after -0.45% M/M. There should be further declines in the pipeline.

- However, more notable from the goods side was core goods ex used vehicles printing -0.18% M/M after two 0.00% M/M readings. It's technically its first month of deflation since Feb’21 as it continues to reflect the significant moderation in supply chain pressures.

- One driver for the latest tick lower is apparel prices -0.03% M/M after 0.31% M/M, its first (very small) decline since Oct’22.

CPI Unrounded - Jul'23

Unrounded % M/M (SA): Headline 0.167%; Core: 0.160% (from 0.158%)

Unrounded % Y/Y (NSA): Headline 3.178%; Core: 4.653% (from 4.829%)

US JOBLESS CLAIMS +21K TO 248K IN AUG 05 WK

US PREV JOBLESS CLAIMS REVISED TO 227K IN JUL 29 WK

US CONTINUING CLAIMS -0.008M to 1.684M IN JUL 29 WK

- Landing along with CPI, initial jobless claims disappointed as they surprisingly increased to 248k (cons 230k) after an unrevised 227k, for its largest weekly increase since early June.

- We focus on the four-week average to smooth some of the noise, and this only increased 3k to 231k for still down from a recent high nudging almost 260k in mid-June.

- That aside, the latest non-seasonally adjusted data registered a 20k increase to 226k with one standout increase coming from Ohio (+5.3k to 24k) as it remains particularly high relative to non-pandemic years compared to some more notable states.

- Continuing claims meanwhile provided a partial offset as they fell to 1684k (cons 1707k) from a downward revised 1692k (cons 1700k), back below the 2019 average in recent weeks but with what looks like a still favorable seasonal adjustment process considering the levels of NSA claims remains above that of pre-pandemic years.

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 25.08 points (0.07%) at 35144.18

- S&P E-Mini Future down 3 points (-0.07%) at 4482.25

- Nasdaq up 11.8 points (0.1%) at 13732.11

- US 10-Yr yield is up 8.8 bps at 4.0958%

- US Sep 10-Yr futures are down 19.5/32 at 110-25

- EURUSD up 0.0007 (0.06%) at 1.0981

- USDJPY up 1.04 (0.72%) at 144.77

- WTI Crude Oil (front-month) down $1.63 (-1.93%) at $82.77

- Gold is down $1.04 (-0.05%) at $1913.41

- EuroStoxx 50 up 66.71 points (1.55%) at 4384.04

- FTSE 100 up 31.3 points (0.41%) at 7618.6

- German DAX up 143.94 points (0.91%) at 15996.52

- French CAC 40 up 111.58 points (1.52%) at 7433.62

US TREASURY FUTURES CLOSE

- 3M10Y +10.014, -134.14 (L: -151.899 / H: -134.14)

- 2Y10Y +6.052, -73.955 (L: -82.235 / H: -73.081)

- 2Y30Y +6.14, -58.067 (L: -64.108 / H: -56.768)

- 5Y30Y +0.749, 3.883 (L: 0.97 / H: 9.296)

- Current futures levels:

- Sep 2-Yr futures down 2/32 at 101-18.75 (L: 101-18.25 / H: 101-25.5)

- Sep 5-Yr futures down 11.25/32 at 106-21.5 (L: 106-20.25 / H: 107-12.25)

- Sep 10-Yr futures down 20/32 at 110-24.5 (L: 110-23.5 / H: 111-29)

- Sep 30-Yr futures down 1-10/32 at 121-14 (L: 121-14 / H: 123-22)

- Sep Ultra futures down 1-24/32 at 127-4 (L: 127-04 / H: 130-07)

US 10Y FUTURE TECHS: (U3) Sold on Rallies

- RES 4: 113-08 High Jul 18 and a bull trigger

- RES 3: 112-31 High Jul 20

- RES 2: 112-12+ 50-day EMA

- RES 1: 111-29/112-07 High Aug 10 / Jul 27

- PRICE: 110-25 @ 1550 ET Aug 10

- SUP 1: 110-23/109-24 Low Aug 7 / 4 and the bear trigger

- SUP 2: 109-14 Low Nov 8 2022 (cont)

- SUP 3: 109-10+ Low Nov 4 2022 (cont)

- SUP 4: 108-26+ Low Oct 21 2022 (cont) and a major support

The intraday rally in Treasuries was sold into the London close - a bearish development despite the show above the 20-day EMA. This keeps the trend condition bearish, however, a bullish corrective cycle remains in play and the contract has recovered from its recent lows. A clear break of the 20-day EMA is needed to signal any scope for a stronger corrective recovery, but the bear trigger remains defined at 109-24, Aug 4 low.

SOFR FUTURES CLOSE

- Sep 23 +0.010 at 94.610

- Dec 23 -0.005 at 94.640

- Mar 24 -0.020 at 94.880

- Jun 24 -0.035 at 95.235

- Red Pack (Sep 24-Jun 25) -0.085 to -0.055

- Green Pack (Sep 25-Jun 26) -0.11 to -0.095

- Blue Pack (Sep 26-Jun 27) -0.125 to -0.115

- Gold Pack (Sep 27-Jun 28) -0.125 to -0.12

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00001 to 5.31247 (-.00777/wk)

- 3M +0.00237 to 5.36915 (-0.00143/wk)

- 6M +0.00043 to 5.42140 (-0.01279/wk)

- 12M +0.00342 to 5.31174 (-0.05061/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $111B

- Daily Overnight Bank Funding Rate: 5.31% volume: $282B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.322T

- Broad General Collateral Rate (BGCR): 5.27%, $561B

- Tri-Party General Collateral Rate (TGCR): 5.27%, $551B

- (rate, volume levels reflect prior session)

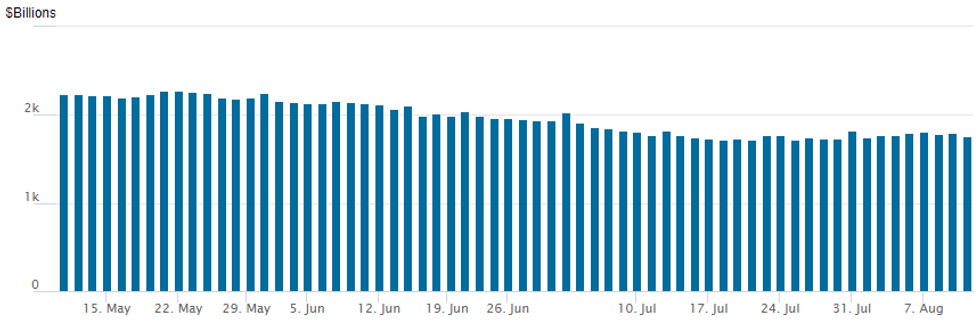

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

The latest operation recedes to $1,759.897B, w/103 counterparties, compared to $1,796.519B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: $3B Celanese US Holdings Launched

Desks still expect ONEOK 5pt to launch this afternoon- Date $MM Issuer (Priced *, Launch #)

- 08/10 $3B #Celanese US Holdings $1B 5Y +215, $1B 7Y +240, $1B 10Y +260

- 08/10 $Benchmark ONEOK 3Y +140a, 5Y +175a, 7Y +195a, 10Y +210a, 30Y +265a

EGBs-GILTS CASH CLOSE: Bunds Underperform Again

Bunds underperformed Gilts for a 2nd consecutive session Thursday, with European yields moving higher after the much-anticipated US CPI reading for July came in on the soft side of expectations.

- A typically quiet pre-US inflation report morning included a yield jump at the open on a broader risk-on move. But yields began sagging in the afternoon, amid a US-led bid.

- Shortly after the CPI release was digested, yields began resolving in an upward direction, with the move exacerbated by erstwhile Federal Reserve dove Daly noting after the data that the central bank had more work to do.

- The German curve bear steepened modestly on the day. The UK curve twist steepened as BoE hike expectations continued to fade, with the long-end trading more in tune with global core FI counterparts.

- Periphery spreads tightened, mirroring a risk-on rise in European equities.

- Final CPIs for the Netherlands, Portugal and Italy brought no major surprises.

- Friday's schedule brings UK GDP, and French and Spanish final July inflation.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.2bps at 2.984%, 5-Yr is up 3.4bps at 2.545%, 10-Yr is up 3.1bps at 2.528%, and 30-Yr is up 3.5bps at 2.625%.

- UK: The 2-Yr yield is down 2.1bps at 4.905%, 5-Yr is down 2.2bps at 4.39%, 10-Yr is down 0.1bps at 4.364%, and 30-Yr is up 1.3bps at 4.575%.

- Italian BTP spread down 3.2bps at 161.8bps / Greek down 2.2bps at 130.6bps

FOREX: USD Stages Impressive Recovery Following Inflation Release

- A moderately lower headline print for US CPI in July had the initial effect of a weaker greenback, however, as some stronger detail emerged from the data, the USD index staged an impressive recovery, bouncing to session highs in late US trade.

- The USD index stands in very minor positive territory after being down as much 0.70% in the immediate aftermath of the release.

- The most notable laggard in the second half of the session has been the Japanese Yen, registering as one of the weakest currencies across G10 on Thursday. Despite the sharp move down in USDJPY to 143.30 after the US inflation data, the recovery has been consistent and substantial throughout US trade, showing little regard for the turn lower for major equity benchmarks.

- An uptrend in USDJPY remains intact and the pair continues to narrow the gap with key medium term pivot resistance at 145.07, the June 30 high, which also represents the key bull trigger. A break of 145.07 would confirm a resumption of the trend and first target 145.69 before 146.38, both Fibonacci projection levels.

- More moderate declines have been seen for the likes of GBP, NZD and CAD, however both the Euro and AUD remain just about in positive territory after their initial boost throughout European trade amid a more benign risk backdrop.

- Emerging market currencies have proved more resilient amid the turnaround for equities and the likes of ZAR, HUF, CLP, COP remain firmly higher on the session, posting between 0.85-1.85% advances.

- UK growth data will highlight Friday’s European docket before US producer prices data for July and Preliminary U Mich sentiment and inflation expectations round off the week’s economic data calendar.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/08/2023 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 11/08/2023 | 0600/0700 | ** | | UK | Index of Services |

| 11/08/2023 | 0600/0700 | *** | | UK | Index of Production |

| 11/08/2023 | 0600/0700 | ** | | UK | Trade Balance |

| 11/08/2023 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 11/08/2023 | 0600/0700 | *** | | UK | GDP First Estimate |

| 11/08/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 11/08/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 11/08/2023 | - | *** |  | CN | Money Supply |

| 11/08/2023 | - | *** | | CN | New Loans |

| 11/08/2023 | - | *** | | CN | Social Financing |

| 11/08/2023 | 1230/0830 | *** |  | US | PPI |

| 11/08/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 11/08/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.