Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Domestic data from China for July came in weaker than expected across the board adding to evidence that the domestic economy is struggling to recover. As a result, key rates were also reduced today (1-yr MTF to 2.5% from 2.65%). Given slowing growth in domestic indicators, there is also the possibility of further policy measures.

- In Australia the Q2 wage price index rose less than expected at 0.8% q/q and 3.6% y/y after 0.8% and 3.7% in Q1. Thus wages remained consistent with the inflation target in Q2 and should mean that the RBA is on hold again at its September 5 meeting.

- The RBNZ is unanimously expected to keep rates at 5.5% at its August 16 meeting. This is a statement meeting and will include revised forecasts and the focus will be on the expected paths for inflation and the OCR. They are unlikely to be revised significantly with the first rate cut expected in H2 2024 when inflation returns to the band.

MARKETS

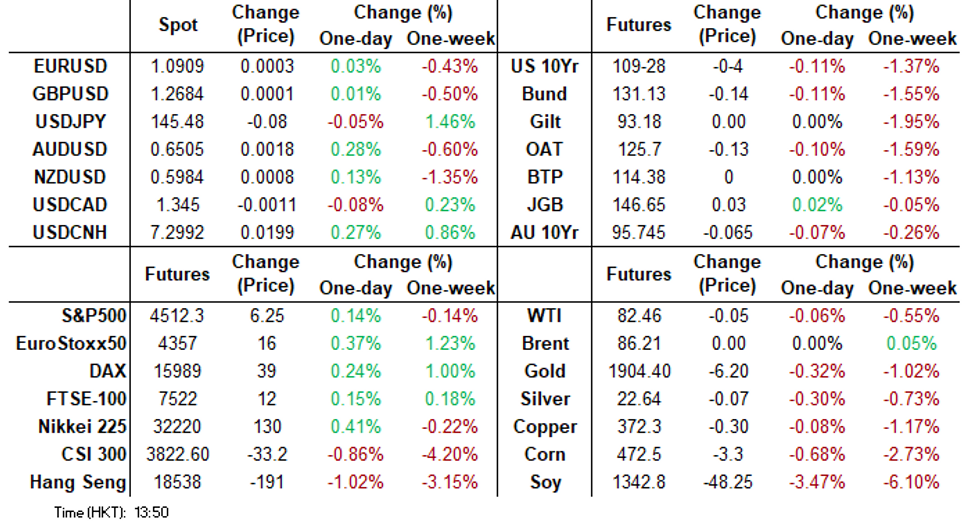

US TSYS: Narrow Ranges In Asia

TYU3 deals at 109-28+, -0-03+, a 0-05 range has been observed on volume of ~66k.

- Cash tsys sit little changed across the major benchmarks.

- Tsys have observed narrow ranges with little follow through on moves in a muted Asian session for the space.

- A recovery from early session lows was facilitated by an unexpected cut to two key policy rates by the PBOC, however narrow ranges persisted through the session.

- The highlight flow wise was a block buyer in FV (8.4k lots).

- UK Employment data for June provides the highlight in today's European session. Further out US retail sales, empire manufacturing, business inventories and cross-border investment are due. Fedspeak from Federal Reserve Bank of Minneapolis President Neel Kashkari crosses.

JGBs: Futures Unchanged, Middle Of The Tokyo Range

JGB futures are unchanged, flat compared to the settlement levels, dealing in the middle of the Tokyo session range. The morning session saw the sell-off sparked by the much stronger-than-expected Q2 GDP print unwound. However, lacklustre demand seen at the 5-year auction saw futures weaken again in the Tokyo afternoon session.

- The 5-year auction faced a lacklustre reception with pricing falling short of dealer expectations. The lack of demand was also reflected in the cover ratio falling to the lowest level observed at a 5-year auction since March. Adding to these concerns, the tail also grew longer, marking its most extended length since March.

- Cash JGBs are cheaper across the curve beyond the 1-year, with yield movements ranging from flat (3-4-year zone) to +1.3bp (10-year). The 10-year yield is at 0.625%, above BoJ's YCC old limit of 0.50% but below its new hard limit of 1.0%.

- The swap curve bear steepened, with rates 0.2bp higher to 1.6bp higher. Swap spreads are wider, apart from the 7-10-year.

- Tomorrow the local calendar is light with Department Store Sales as the highlight.

- Tomorrow also sees BoJ Rinban operations covering 1-3-year, 5-10-year and 25-Year+ JGBs.

AUSSIE BONDS :Cheaper, Post-WPI Richening Pared

ACGBs (YM -5.0 & XM -6.5) are weaker but in the middle of the Sydney session’s range. ACGBs spiked richer after the Q2 Wage Price Index (WPI) missed forecasts, printing +0.8% q/q versus expectations of +0.9%, but around half of those gains were subsequently reversed.

- The reversal could reflect that Q3 data is the key print with not only minimum wages increasing on July 1 but also other awards (awards didn’t contribute to Q2 rise). We should see if services were able to pass on higher wages in Q3 CPI data on October 25. The July NAB wage cost component rose sharply.

- The August RBA Minutes were released also but are unlikely to have had a major impact given RBA Governor’s Lowe testimony to Parliament on Friday outlined the key issues.

- Cash ACGBs are flat to 1bp richer after the releases to be 5-6bp cheaper on the day. The AU-US 10-year yield differential is 2bp wider at +6bp.

- Swap rates are 5-6bp higher on the day.

- The bills strip shifts from a post-release twist steepening to a bear steepening with pricing flat to -9.

- RBA-dated OIS pricing is flat out to December and 1-4bp firmer for meetings beyond.

- Tomorrow the local calendar sees the Westpac–MI Leading Index.

NZGBS: Closed Weaker, Mid-Range, Awaits RBNZ Policy Decision Tomorrow

NZGBs closed 3-6bp weaker, in the middle of the local session’s range, with the 2/10 cash curve steeper.

- Swap rates are flat to 4bp higher with implied swap spreads tighter.

- The local calendar saw a couple of releases today. In addition to the previously mentioned REINZ house sales and price data, the RBNZ published Q3 household expectations survey results. The median expected inflation rate in 2 years to be 3.5% down from 5% in Q2. The survey also showed median expected house price inflation in 1 year of 0.0%.

- Tomorrow sees the RBNZ policy decision, with Bloomberg consensus unanimous in expecting the OCR to be kept at 5.50%.

- RBNZ dated OIS is flat across meetings out to Feb’24 and 1-7bp firmer for meetings beyond. The market attaches an 8% chance of a 25bp hike tomorrow.

- Over the past six weeks, terminal OCR expectations have primarily traded within a range of 5.60-5.65%, aside from a brief uptick to 5.81% in early July. This trading pattern aligns with the "watch, worry, and wait" guidance issued by the RBNZ during its May Monetary Policy Statement.

- Later today, US retail sales, empire manufacturing, business inventories and cross-border investment are due.

OIL: Crude Range Trades As China Data Holds Good News

MNI (Australia) - Oil prices have been in a narrow range during APAC trading today after falling almost a percent on Monday. They rose following China’s rate cut announcement with the 1-year MTF reduced to 2.5% from 2.65% and while they are off their highs following that, they were not too adversely affected by the disappointing China data. The USD index is down slightly.

- Brent is up 0.1% to $86.30/bbl after a high of $86.46. It has found support at $86. WTI is flat at $82.54 with the high at $82.72.

- Bloomberg is reporting that China increased refining to its highest in 3 months in July and so apparent crude demand rose 21.2% y/y. OilChem expects refining operating rates to rise further in August. In July they were 81.2%.

- On the supply side, the US and UK warned about increased risks to shipping in the Strait of Hormuz near Iran, an important for crude shipping route. This is in addition to tensions in the Black Sea.

- Given the attention on supply, the US API inventory data out later is likely to be watched closely. It showed a 4.1mn barrel stock build in the latest week, according to Bloomberg.

- Later the Fed’s Kashkari speaks and US July retail sales are forecast to post solid monthly rises. There are also US trade prices for July, June inventories, August Empire manufacturing & NAHB housing. There is also Canadian July CPI and UK wages and labour data.

GOLD: At Support

Gold is little changed in the Asia-Pac session, after closing 0.3% lower on Monday. Bullion came under pressure from the sell-off in US tsys and a strong USD.

- Cash tsys finished 2-7bps cheaper across the major benchmarks, with the curve flatter. Higher bond yields are typically negative for the precious metal, which doesn’t earn interest income.

- The USD dollar index surged higher and closed above the 103.00 level for the first time since July 6. The index climbed to 103.458, rallying against all of its G10 peers.

- According to MNI’s technicals team, the yellow metal touched support at $1902.8 (Jul 6 low) before bouncing as Treasuries pared losses and the USD index pulled back off highs.

FOREX: Greenback Marginally Pressured In Asia

The USD is marginally pressured in Asia, however ranges remain narrow across the G-10 space.

- AUD is the strongest performer in the space at the margins. AUD/USD is ~0.2% firmer and last prints a touch above the $0.65 handle. The pair firmed off session lows after the PBOC cut 2 key policy rates and a weaker than expected WPI as risk sentiment improved through the session.

- Kiwi is also ~0.2% firmer, however ranges remain narrow and NZD/USD sits well within recent ranges.

- Yen is little changed from opening levels, there was a muted reaction to the stronger than forecast Q2 GDP print and USD/JPY respected a ¥145.30/60 range for the most part.

- Elsewhere in G-10, EUR and GBP are marginally firmer and SEK is lagging however liquidity is generally poor in Asia.

- Cross asset wise; e-minis are ~0.2% firmer and US Tsy are little changed across the major benchmarks. BBDXY is ~0.1% lower.

- UK Employment data for June provides the highlight in today's European session.

MNI RBNZ Preview - August 2023: On Hold, OCR Path Likely Unchanged

- The RBNZ is unanimously expected to keep rates at 5.5% at its August 16 meeting. This is a statement meeting and will include revised forecasts and the focus will be on the expected paths for inflation and the OCR. They are unlikely to be revised significantly with the first rate cut expected in H2 2024 when inflation returns to the band.

- We don’t expect any material changes to the forward guidance in August with the RBNZ continuing to keep its options open. The Board is likely to reiterate that monetary policy needs to remain at a “restrictive level for some time”. But there could be a warning that domestic and underlying prices are looking sticky and that they need to moderate further.

- See full preview here.

NEW ZEALAND: Sticky Household Inflation Expectations Turn Down

Household inflation expectations for Q3 as measured by the RBNZ eased significantly with the 1-yr ahead median moderating to 5% from 7%, the peak, and the 2-year to 3.5% from 5%. Recent research from the RBNZ found that both business and household inflation expectations are useful in projecting the CPI. It found that the 1-year mean household measure was the best and this series eased to 6% in Q3 from 7.4%. It has been sticky until the latest data point, which should reassure the RBNZ.

NZ CPI y/y% vs inflation expectations

Source: MNI - Market News/Refinitiv/RBNZ

AUSTRALIA:Wages Consistent With Inflation, Monitor Q3

The Q2 wage price index rose less than expected at 0.8% q/q and 3.6% y/y after 0.8% and 3.7% in Q1. Thus wages remained consistent with the inflation target in Q2 and should mean that the RBA is on hold again at its September 5 meeting.

- However, the Q3 data is key with not only minimum wages increasing on July 1 but also other awards (awards didn’t contribute to Q2 rise). The WPI rose 1.1% q/q in Q3 2022. While it is not released until November 15, we should see if services were able to pass on higher wages in Q3 CPI data on October 25. The July NAB wage cost component rose sharply.

- The ABS noted that higher inflation and the tight labour market had resulted in higher wages. While the share of workers receiving higher wages in Q2 this year was lower than last year, the size of increase was larger, “… share of jobs which received increases above 3 percent was the highest for a June quarter since 2012”.

- Private wages rose 0.8% q/q and 3.8% y/y in line with Q1, while the public sector continued catching up rising 0.7% and 3.1% after 2.9%. The average hourly private sector increase for those wages that rose continued to trend higher in Q2 at 4.5% compared with 4.3% in Q1 and 3.8% in Q2 2022. For the public sector it was 3% after 3% and 2.4% respectively.

Source: MNI - Market News/ABS/SEEK

AUSTRALIA: Rates Cut As Domestic Data Disappoints

MNI (Australia) - Domestic data from China for July came in weaker than expected across the board adding to evidence that the domestic economy is struggling to recover. As a result, key rates were also reduced today (1-yr MTF to 2.5% from 2.65%). Given slowing growth in domestic indicators, there is also the possibility of further policy measures.

- Markets have not reacted strongly to the data given the offsetting effect of rate cuts. Brent crude is up 0.1% and AUDUSD +0.1%. The CSI 300 is down 0.2%.

- Retail sales rose 2.5% y/y in July, slowest since December 2022, down from 3.1% in June leaving the YTD 7.3% down from 8.2%. The softer outcome was due to car sales.

- IP rose 3.7% y/y down from 4.4% but steady YTD at 3.8%.

- Fixed asset investment YTD growth slowed to 3.4% from 3.8% with property investment contracting 8.5% after -7.9%. Property sales rose only 0.7% y/y YTD down from 3.7%, as problems in the sector continue.

- Finally, the jobless rate rose slightly to 5.3% whereas it had been expected to stay at 5.2%.

JAPAN: Exports Driving Recovery

Q2 preliminary GDP rose a stronger-than-expected 1.5% q/q (6% saar) to be up 2.1% y/y following 0.9% and 1.9% in Q1. This is the strongest quarterly increase since the Covid-affected Q4 2020. The strength was driven by export growth of 3.2% q/q driven by autos, which resulted in net exports contributing 1.8pp to growth. This suggests that global growth is proving resilient so far in 2023. Tourism is also recovering, which should continue over H2. Domestic components were lacklustre though with consumption falling 0.5% q/q, investment flat and inventories detracting 0.2pp.

Japan real GDP growth %

Source: MNI - Market News/Refinitiv

AUSTRALIA: CBA Spending Insights Shows Continued Soft Consumption

CBA has revamped its household spending intentions series and it is now called Household Spending Insights (HSI). The new series is more closely correlated to nominal retail sales than the old one was (see chart). It was flat in July rising 1.3% y/y after 0.5% m/m and 1.2% y/y in June. It is signalling that retail spending is likely to remain weak given rate and cost-of-living pressures.

- The HSI is a seasonally adjusted composite of payments data from CBA customers which cover 30% of Australian consumer transactions. It is census weighted to make it representative of the country as a whole. It includes 12 categories and now has goods vs services, retail vs non-retail, non-discretionary vs discretionary breakdowns.

- The July softness was not broad based with only 5 of the 12 categories recording a monthly fall. Household goods rose 2.1% m/m whereas household services fell 5.5%.

- Goods spending rose 1.1% m/m to be down 1.3% y/y whereas services remained solid rising 0.6% m/m to be up 3.6% y/y. Retail spending is up 0.8% y/y and non-retail +0.6%. Essential consumption rose 2.3% y/y with discretionary slightly lower at +1.7%.

- The Home Buying Index rose 2.1% m/m after falling 13.7% in June. It is now down 9% y/y an improvement from -14.8%.

- See CommBank Household Spending Insights here.

Source: MNI - Market News/Bloomberg/ABS

EQUITIES: APAC Markets Mixed Following China Rate Cuts & Data

Equity markets across the APAC region are mixed today with the Nikkei up 0.6% but the Hang Seng down 1.2%. The PBoC’s rate cuts have helped to support markets following the weaker-than-expected domestic data. The CSI 300 is down 1%. The ASX is up 0.4% and the NZX is down slightly ahead of Wednesday’s RBNZ meeting. India’s Nifty is flat, the KOSPI down 0.8% with ASEAN also mixed. US S&P e-mini is up 0.1% while NASDAQ is +0.2%. The USD index is flat.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/08/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 15/08/2023 | 0600/0800 | *** |  | SE | Inflation Report |

| 15/08/2023 | 0900/1100 | *** |  | DE | ZEW Current Expectations Index |

| 15/08/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 15/08/2023 | 0900/1100 | *** | | DE | ZEW Current Conditions Index |

| 15/08/2023 | 1230/0830 | *** |  | CA | CPI |

| 15/08/2023 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 15/08/2023 | 1230/0830 | *** |  | US | Retail Sales |

| 15/08/2023 | 1230/0830 | ** | | US | Import/Export Price Index |

| 15/08/2023 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/08/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 15/08/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 15/08/2023 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 15/08/2023 | 1400/1000 | * | | US | Business Inventories |

| 15/08/2023 | 1500/1100 | | US | Minneapolis Fed's Neel Kashkari | |

| 15/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 15/08/2023 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.