- Chinese & Hong Kong listed have traded higher on the back of further stimulus measures announced, while post the lunch break there have been even further headlines out which has caused property stocks to soar higher, Mainland Property Index was last up 8.50%.

- Earlier this morning, the Fed's Adriana Kugler said she is not worried about inflation falling consistently below the central bank’s 2% target.

- The share of Australian borrowers in severe financial stress remains small with the vast majority still able to service their debts, the Reserve Bank said in a half-yearly review

MARKETS / UP TODAY (TIMES GMT/LOCAL)

US TSYS: Tsys Futures Steady Ahead Of Busy US Data Session & Fed Speak

- It has been a very quiet session for US tsys, ranges have been extremely tight while volumes are well below recent averages. Focus in the region has largely been on China, where they have announced further stimulus packages aimed at those in extreme poverty, which saw consumer discretionary & staples stocks rally, while it was also announced they would look to inject 1t yuan ($142 billion) of capital into its biggest state banks.

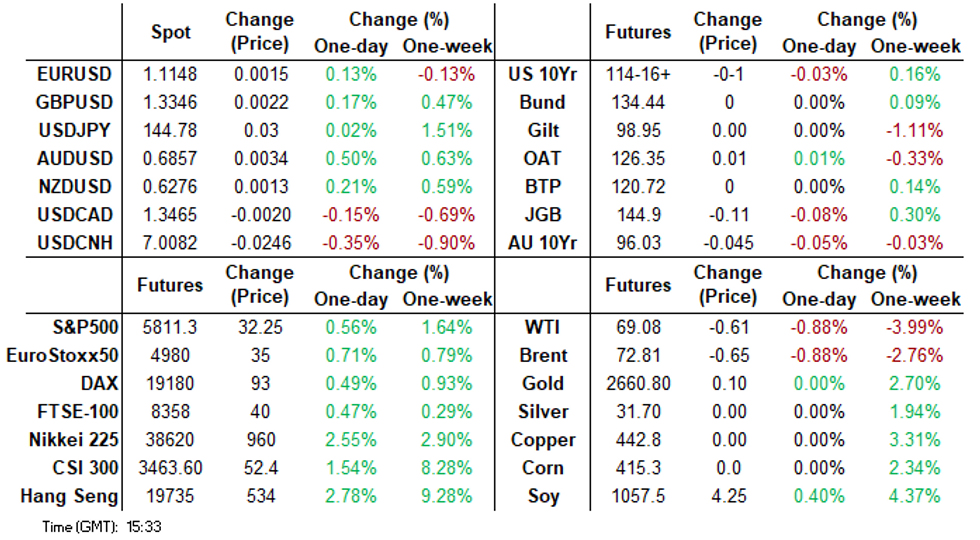

- TU is trading - 00+ at 104-10⅛, while TY is trading - 01 at 114-16+

- Incase missed during the US morning session on Wednesday, there was the largest SOFR block on record with SFRZ4 118k sold at 96.065. The market at the time was trading at 96.09 near cycle highs, after hitting lows of 94.915 in May with the contract last trading at 96.050.

- Fed Gov Kugler, a dovish FOMC member, supported the recent 50bp rate cut, citing a cooling but resilient labor market and ongoing inflation progress. She anticipates further rate cuts if disinflation continues, aiming to balance economic growth and inflation control.

- Cash tsys curves are little changed today, with yields flat to 1bps lower. The 2yr yield is -0.2bps at 3.557%, while the 10yr is -0.2bps at 3.783%, while the 2s10s is hovering near highs at 22.379

- Projected rate cuts into early 2025 held steady to mixed, latest vs Wednesday levels (*) as follows: Nov'24 cumulative -40.4bp (-39.1bp), Dec'24 -77.2bp (-79.1bp), Jan'25 -110.0bp (-112.5bp).

- Looking ahead to Thursday's session: weekly claims, GDP, PCE, Cap Goods, Durables, Pending home sales and a flurry of Fed speakers including Barr, Cook, Kashkari, Williams and Chairman Powell.

JGBS: Cash Bonds Are Cheaper Ahead Of A Heavy US Calendar

JGB futures are weaker, -11 compared to the settlement levels.

- (MNI) A BoJ board member emphasised the need to adjust the degree of easy policy further following the BoJ Board's call to raise the policy interest rate to 0.25% at the July meeting, the minutes showed. The BoJ should raise the policy rate to neutral, estimated to be at least 1%, toward the second half of the projection period, said another member.

- Cash US tsys are ~0.5bp richer in today’s Asia-Pac session. Today’s US calendar will see Weekly Claims, GDP, PCE, Cap Goods, Durables, and Pending Home Sales data alongside a flurry of Fed speakers: Barr, Cook, Kashkari, Williams and Chairman Powell.

- Cash JGBs are cheaper across benchmarks, with the 40-year (+3.5bps) despite solid demand at today’s 40-year auction. The actual high yield of 2.34% was lower than BBG poll dealer expectations (2.35%).

- Swap rates are 1bp lower to 6bps higher, with the curve steeper. Swap spreads are mixed.

- Tomorrow, the local calendar will see Tokyo CPI, Weekly International Investment Flows and Coincident & Leading Index data.

- (Bloomberg Economics) “Tokyo’s September CPI report due Friday is likely to show solid momentum in inflation, propelled by a positive wage-price cycle resulting from spring pay agreements.” (See link)

ACGBS: Cheaper, Narrow Ranges, Awaiting Powell & US Data

ACGBs (YM -4.0 & XM -4.5) are cheaper after dealing in narrow ranges in today’s Sydney session.

- (AFR) Falling interest rates could trigger a property price boom that encourages households to take on too much debt, raising the risk of a future market downturn that ravages the economy, the Reserve Bank of Australia has warned. (See link)

- With the domestic calendar light, local investors have been content to sit on the sideline ahead of a heavy US calendar later today.

- Cash US tsys are ~0.5bp richer in today’s Asia-Pac session. Today’s US calendar will see Weekly Claims, GDP, PCE, Cap Goods, Durables, and Pending Home Sales data alongside a flurry of Fed speakers: Barr, Cook, Kashkari, Williams and Chairman Powell.

- Cash ACGBs are 3-4bps cheaper, with the AU-US 10-year yield differential at +16bps.

- Swap rates are 3-4bps higher.

- The bill strip is cheaper, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing is flat to 5bps firmer across meetings, with late 2025 leading. A cumulative 15bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty apart from the AOFM’s planned sale of A$500mn of the 2.25% 21 May 2028 bond.

NZGBS: Bear-Steepener Ahead Of A Heavy US Calendar

The NZGB curve bear-steepened today, with benchmark yields ending the day flat to 3bps higher, though below their session highs.

- With the domestic calendar light, local investors were content to sit on the sideline ahead of a heavy US calendar later today. Today’s US calendar will see Weekly Claims, GDP, PCE, Cap Goods, Durables, and Pending Home Sales data alongside a flurry of Fed speakers: Barr, Cook, Kashkari, Williams and Chairman Powell.

- Cash US tsys are ~0.5bp richer in today’s Asia-Pac session after yesterday’s bear-steepening.

- “New Zealand faces rising debt in coming decades as an ageing population exacerbates a structural budget deficit, in a major challenge for fiscal policy, a top Treasury adviser said. Government debt is projected to climb to more than 100% of gross domestic product by 2050 from about 43% now, Dominick Stephens, chief economic adviser at the Treasury.” (per BBG)

- The swap curve twist-steepened, with rates closing 2bp lower to 2bps higher.

- RBNZ dated OIS pricing closed little changed across meetings. A cumulative 87bps of easing is priced by year-end.

- Tomorrow, the local calendar will see ANZ Consumer Confidence, ahead of ANZ Business Confidence on Monday.

ASIA STOCKS: Further China Stimulus & Strong Tech Results Spur Market Higher

Asian stocks rallied on Thursday, driven by renewed enthusiasm in the tech sector after strong revenue forecasts from Micron. The weakened yen further boosted Japanese stocks, while Chinese markets gained as the government introduced new stimulus measures, including one-off cash handouts for the poor ahead of the National Day holidays. Investors are optimistic about China's commitment to support the economy, including reports of a potential $142 billion capital injection into state banks. The risk-on sentiment across Asian markets follows the Fed’s recent rate cut, and traders are now focused on the potential for more direct stimulus measures from China.

- China & Hong Kong benchmarks are nearing bull market territory with many indices now trading near or 20% off recent lows. the CSI 300 Consumer Staples Index is trading +3.40% following news that government will give handouts to the poor ahead of the National Holidays, with beer and tobacco stocks gaining the most, while property stocks continue their strong gains with the Mainland Property Index up over 5%. The HSI is +2.30%, whiel the CSI 300 is +0.70%

- Japanese equities have surged higher, led by tech stocks after strong forecast from Micron during the US session, Tokyo Electron is currently trading 7.75% higher. Further moves higher may have been capped by caution ahead of the vote for a new leader, who will likely become the next prime minister. The TOPIX is +1.90%, while the Nikkei is +2.35%

- Foreign investors have returned to buying South Korean equities with net inflows of $250m today, local stocks are outperforming Taiwan equities today, in what seems to be a catch up to the recent underperformance.

- Australia's ASX200 is +0.80% led by Discretionary stocks, benefitting from China stimulus

CHINA STOCKS: China Announces Further Stimulus For People In Poverty

China says it will give one-off cash handouts to people in extreme poverty, this looks like it will be on top of the previously announced stimulus made on Tuesday. The government will issue living subsidies to disadvantaged groups, including the very poor and orphans, before the National Day holiday next week, the state broadcaster CCTV reported.

- Shanghai is also issuing over 500m yuan ($71m) of discount vouchers from late September for the public to spend on dining, accommodation, movie tickets and sports.

- Consumer discretionary & Staples have jumped higher on the back of this news.

- Hong Kong listed equities are outperforming today, with the HSI +1.50%, while the CSI 300 is +0.50%.

ASIA STOCKS: Taiwan Sees Large Inflow, Indonesia & Philippines Run Ends

Taiwan has continued to strong run lately with its largest inflow since Aug 16, while Indonesia & Philippines have ended their multi-week run on inflows.

- South Korea: Saw outflows of $419m yesterday, with the past 5 sessions reaching - $1.86b, while YTD flows are + $10.71b. The 5-day average is - $372m, below both the 20-day average of - $355m and the 100-day average of - $28m.

- Taiwan: Saw inflows of $1.16b yesterday, with the past 5 sessions netting + $3.48b, while YTD flows are - $11.85b. The 5-day average is + $697m, above the 20-day average of - $175m, but below the 100-day average of - $113m.

- India: Saw outflows of $174m Tuesday, with the past 5 sessions netting + $2.22b, while YTD flows are + $23.81b. The 5-day average is + $484m, above both the 20-day average of + $428m and the 100-day average of + $109m.

- Indonesia: Saw outflows of $122m yesterday, with the past 5 sessions netting + $132m, while YTD flows are + $3.64b. The 5-day average is + $26m, below the 20-day average of + $138m, but above the 100-day average of + $31m.

- Thailand: Saw outflows of $17m yesterday, with the past 5 sessions totaling + $148m, while YTD flows are - $2.45b. The 5-day average is + $30m, below the 20-day average of + $46m, but above the 100-day average of - $6m.

- Malaysia: Saw outflows of $40m yesterday, with the past 5 sessions netting - $39m, while YTD flows are + $912m. The 5-day average is - $8m, below both the 20-day average of + $26m and the 100-day average of + $14m.

- Philippines: Saw inflows of $16m yesterday, with the past 5 sessions totaling + $155m, while YTD flows are - $68m. The 5-day average is + $31m, above both the 20-day average of + $13m and the 100-day average of + $2m.

Table 1: EM Asia Equity Flows

GOLD: Fresh All-Time High Ahead Of Heavy Calendar Of US Data & Fed Speakers

Gold is little changed in today’s Asia-Pac session, after climbing to a fresh record high of $2,670 in Wednesday’s session.

- Yesterday’s move in bullion came despite a bear-steepening of the US Treasury curve ahead of today’s flood of data and Fed speakers not to mention next week's September employment data.

- Today’s US calendar includes Weekly Claims, GDP, PCE, Cap Goods, Durables, and Pending Home Sales data alongside a flurry of Fed speakers: Barr, Cook, Kashkari, Williams and Chairman Powell.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- According to MNI’s technicals team, moving average studies are in a bull-mode set-up, highlighting a clear uptrend and positive market sentiment. The focus is on $2675.5 next, a Fibonacci projection.

OIL: OIL DOWN ON LIBYAN COMPROMISE.

- Libyan factions have announced that a compromise has been reached on appointing a new lead for the Central Bank.

- Libya’s Eastern and Western regions have been in dispute since mid-August following attempts by the Central Government to replace the Head of the Central Bank.

- The dispute resulted in the shutdown of production and exports of oil in the East, the main supplier of crude from the country, were suspended.

- The news of the compromise saw oil slip in the US afternoon with West Texas Intermediate declining more than 2%, to break through US$70 to settle at $69.60.

- Brent too trended lower on the news initially breaking through US$73.50 before settling at US$73.67.

- Oil has had a push pull week given the China stimulus news, providing support to risk markets in general as the policy measures announced are aimed at resolving the housing crisis in China.

- As always geo-politics is never far away when it comes to oil and comments by the Iranian President that ‘Israel attacks in Lebanon cannot go unanswered,’ provide support to oil prices.

- The key risks at present is how Libyan production comes back online and the supply risks associated with that.

- Lastly news of Hurricane Helene in the Mexican gulf has been sidelined given Libyan and Israel / Lebanon news yet it is now impacting production and supply and projected to make landfall in Florida Thursday or Friday US time.

- Despite all of these factors it is likely that oil’s fortunes today will be impacted by a deluge of data tonight from the US including GDP, Core PCE, Durable Goods and Initial Jobless Claims.

G10 FX: G-10 Currencies Take a Breather After Yesterday’s Dollar Strength.

- G10 currencies were quiet in Asian trading hours today following yesterday’s surge by the USD.

- As markets continue to digest the China stimulus news, further stories were hitting markets about the Chinese authorities recapitalising the major banks to support the expected rise in lending to support the economy.

- The BBG dollar spot index fell 0.10% in morning trade, giving back some of yesterday’s outperformance.

- Having trading briefly through 140 to the USD ten days ago, the JPY has softened since trending towards 145, settling at 144.90 in the afternoon session in Tokyo.

- The AUD, having trending down to 68.20 this morning, trended higher at 68.45, following Asian FX moves.

- The US will see a barrage of data tonight, potentially given further insight as to the pace of rate cuts by the Federal Reserve. Data out tonight include GDP, Core PCE, Durable Goods and Initial Jobless Claims.

ASIA FX: Currencies Mixed Following Strong Week.

- Asia currencies took were mixed today following a strong week on the back of the FED cut and China stimulus news.

- The CNY Reference Rate at 7.0354 Per USD; Estimate 7.0344, reference rate was fixed 0.22% higher than the previous trading day.

- USD/CNH rallied 0.2% on the news of potential capital injection by the PBOC into the major banks to support their lending objectives.

- IDR was the biggest underperformer, 0.5% higher in Asian trading hours.

- SGD and THB were the stronger currencies in Asia, both up 0.20%. The THB reacted to ongoing calls by the government for the Central Bank to cut rates.

- Malaysia’s Central Bank the BNM issued a statement in which it predicted ‘enduring support for the Ringgit’ which is one of Asia’s best performers for the year. Despite this the MYR was little changed on the day.

NEW ZEALAND: Fonterra Upgraded, Raises Milk 2024/25 Milk Price Forecast

- Fonterra has been upgrade by Macquarie raising their price target 32% to NZ$5.61. Fonterra makes up between 5-6% of the NZX50.

- This follow strong earnings results released yesterday, with the company also lifting its 2024/25 forecast Farmgate Milk Price midpoint 50 cent in $9.00per kgMS.

- Dairy products, especially those from Fonterra, are among New Zealand’s top exports, making the sector a crucial part of the nation's economic landscape.

- The dairy sector directly contributes around 5-7% of New Zealand's GDP. This includes the entire dairy supply chain, from farming to processing and exports.

- In terms of exports, dairy products, primarily milk powder, butter, and cheese, account for about 25-30% of New Zealand's total export revenue, making the dairy industry a cornerstone of the country's export economy.

AUSTRALIA DATA: Australian Job Vacancies

- Australia's job vacancies for the three months to August fell by 5.2% compared to the previous quarter, per the ABS. Non-seasonally adjusted vacancies declined by 2.8% q/q. Key sector changes included significant drops in accommodation and food services (-17.2%), manufacturing (-10.4%), and utilities and waste services (-4.4%). Meanwhile, transport and postal saw a sharp rise (+13.8%), alongside arts and recreation (+8.3%) and wholesale trade (+6.3%).

AUSTRALIA DATA: RBA's Financial Stability Review

Quick summary of the major points from the RBA Financial Stability Review. See Full review here

- The RBA noted that very few mortgage borrowers are in negative equity, indicating limited risk for lenders in case of defaults. There is currently less than 1% of owner-occupier loans are 90+ days in arrears, although there is a slight increase in borrowers experiencing cash flow shortfalls while the RBA anticipates a slight increase in loan arrears as borrowers face ongoing financial pressures.

- Approximately 5% of floating-rate owner-occupier borrowers are experiencing cash flow issues, with essential expenses and mortgage repayments exceeding their income.

- Despite rising loan arrears, Australian banks are reported to have maintained prudent lending standards and have adequate capital and liquidity buffers.

- Most Australian households and businesses are managing pressures from increased inflation and interest rates, with banks remaining resilient.

- The review indicates that small firms, which often have low debt levels, are predominantly responsible for the ongoing increase in insolvencies.

- The RBA cautioned that if financial conditions ease, there is a risk of households taking on excessive debt, which could lead to future financial instability.

- The RBA highlighted potential threats from China's financial sector imbalances, which could impact global and Australian markets.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/09/2024 | 0600/0800 | * |  | GFK Consumer Climate |

| 26/09/2024 | 0700/0900 | ** |  | Economic Tendency Indicator |

| 26/09/2024 | 0730/0930 | *** |  | SNB Interest Rate Decision |

| 26/09/2024 | 0800/1000 | ** |  | M3 |

| 26/09/2024 | 0800/1000 | ** |  | ISTAT Business Confidence |

| 26/09/2024 | 0800/1000 | ** | | ISTAT Consumer Confidence |

| 26/09/2024 | 0900/1100 | | ECB's Elderson remarks at governance & risk meeting | |

| 26/09/2024 | 1230/0830 | *** |  | Jobless Claims |

| 26/09/2024 | 1230/0830 | ** | | WASDE Weekly Import/Export |

| 26/09/2024 | 1230/0830 | *** | | GDP |

| 26/09/2024 | 1230/0830 | * |  | Payroll employment |

| 26/09/2024 | 1230/0830 | ** | | Durable Goods New Orders |

| 26/09/2024 | 1310/0910 | | Fed's Susan Collins, Adriana Kugler | |

| 26/09/2024 | 1325/0925 | | New York Fed's John Williams | |

| 26/09/2024 | 1330/1530 | | ECB Lagarde address at ESRB Conference | |

| 26/09/2024 | 1400/1000 | ** | | NAR Pending Home Sales |

| 26/09/2024 | 1415/1615 | | ECB's De Guindos in macroprudential policy panel | |

| 26/09/2024 | 1430/1030 | ** | | Natural Gas Stocks |

| 26/09/2024 | 1500/1100 | ** | | Kansas City Fed Manufacturing Index |

| 26/09/2024 | 1600/1800 | | ECB's Schnabel at Wirtschaftsrat der CDU e.V | |

| 26/09/2024 | 1700/1300 | | Fed's Neel Kashkari, Michael Barr | |

| 26/09/2024 | 1700/1300 | ** | | US Treasury Auction Result for 7 Year Note |

| 26/09/2024 | 1900/1500 | *** |  | Mexico Interest Rate |