Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

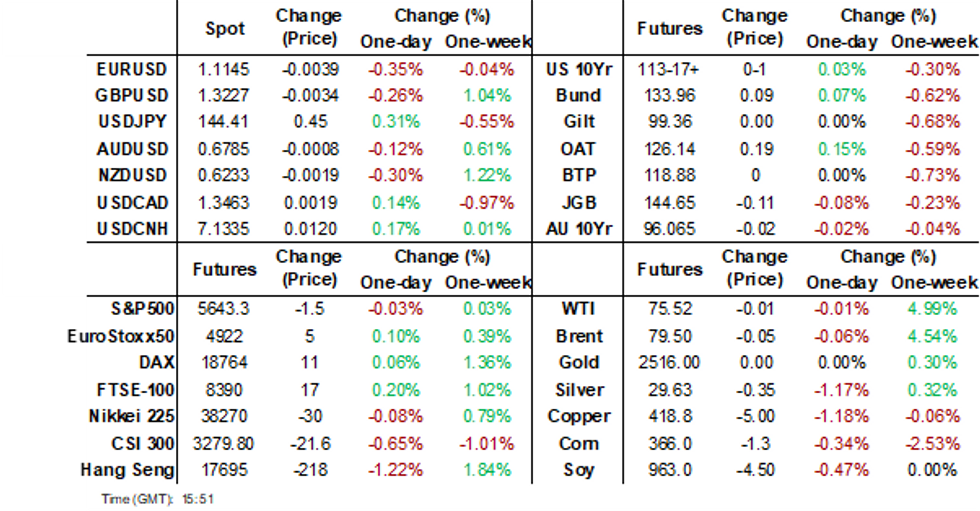

- US Treasury futures are trading at session lows, although little changed from NY closing levels. The USD is higher against the G10, but aggregate gains are modest. The AUD saw some outperformance post the monthly CPI beat, but follow through has been limited.

- Asian equity markets are mostly lower today, with Chinese technology stocks leading the decline amid disappointing earnings Sentiment is weak across the region as investors remain cautious ahead of Nvidia's highly anticipated earnings report. We continue to see outflows from tech sensitive countries in the region.

- Investors have been piling into Global High Yield Indices since the August 5th market sell off, with the yield on the BBG High Yield Index falling about 60bps from Aug 5 highs or 35bps from prior, while yields on IG bonds have held steady since.

- Later the Fed’s Waller and Bostic speak. The data calendar is light with only euro area July M3 of note.

MARKETS

US TSYS: Tsys Futures Slightly Lower Ahead Of 2yr & 5yr Auctions

- Treasury futures are trading at session lows, although little changed from NY closing levels. Early morning we continued the late move higher only to be met with some selling pressure as equity markets sold off. Ranges have remained tight while volumes are likely related to rolls, later today we have $28B 2Y & $70B 5Y bond auctions.

- TYU4 is -0-01 at 113-17+, while TUU4 is trading -00⅝ at 103-11¾

- A bullish theme in Treasuries remains intact and the contract continues to trade above support. Note that moving average studies are in a bull-mode position and this highlights bullish sentiment. Initial resistance is 114-03 (Aug 6 highs), with 114-16 (6.4% of the Aug 5 - 8 pullback) the next resistance, to the downside initial support is 113-03+ (20-day EMA) followed by 112-03 (50-day EMA).

- Cash treasury yields have traded in very tight ranges, the 3-5yr part of the curve has underperformed with yields 1-1.5bps higher while the rest of the curve is about 0.5bps higher, the 2yr is currently 3.907%, while the 10yr is 3.825%.

- The 2s10s curve has jumped 3.400 to -4.578, the least inverted since Aug 9th.

- Projected rate cut pricing through year end has gained vs. early Tuesday levels: Sep'24 cumulative -34.1bp (-31.8bp), Nov'24 cumulative -67.4bp (-64.7bp), Dec'24 -104.6bp (-99.2bp)

- Today, MBA Mortgage Applications, US Treasury auctions include $28B 2Y & $70B 5Y, while Atl Fed Bostic will discuss his economic outlook.

JGBS: Subdued Session, 2Y Supply Tomorrow

JGB futures are weaker and near Tokyo session cheaps, -12 compared to settlement levels.

- (MNI) The Bank of Japan's longer-term plan to normalise its monetary policy and raise interest rates remains intact, MNI understands, although policymakers will likely pause to assess the current situation in at least September, despite Governor Kazuo Ueda's recent comments to legislators that further hikes are still in play this year.

- However, recent market volatility will not derail the BOJ’s long-term rate hike plan considering real interest rates remain at very low levels and far below the perceived neutral rate.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest net movements.

- Cash JGBs are flat to 1bp cheaper across benchmarks. The benchmark 10-year yield is 0.9bps higher at 0.893% versus the cycle high of 1.108%.

- Swap rates are flat to 1bp lower out to the 7-year and 1-3bps higher beyond. Swap spreads are tighter out to the 10-year and wider beyond.

- Tomorrow, the local calendar will see weekly International Investment Flow data and the Consumer Confidence Index alongside 2-year supply.

AUSSIE BONDS: Cheaper After CPI Beat

ACGBs (YM -3.0 & XM -3.0) reversed morning strength to be 5-6bps weaker after July’s CPI Monthly surprised slightly on the upside.

- July headline CPI inflation moderated to 3.5% y/y from 3.8%, slightly higher than expected, driven by lower electricity prices from government subsidies. The trimmed mean moderated to 3.8% from 4.1%, the lowest since January, but few services components were updated. The RBA is likely to look through July and wait for August and especially Q3 data.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session.

- Cash ACGBs are 3bps cheaper, with the AU-US 10-year yield differential 2bps wider on the day at +11bps.

- The latest round of ACGB Dec-34 supply was smoothly absorbed, with the weighted average yield printing through prevailing mids. However, the lower outright yield did appear to hamper the overall strength of bidding today, with the cover ratio declining to 2.3125x from 2.7375x in mid-August and 4.2250x at the June auction.

- Swap rates are 2-3bps higher on the day.

- The bills strip turned this morning’s bull-flattener into a bear-steepener, with pricing -2 to -6.

- RBA-dated OIS pricing is 7-9bps firmer for 2025 meetings after the data. A cumulative 21bps of easing is priced by year-end.

- Tomorrow, the local calendar will see Q2 Private Capital Expenditure data.

AUSTRALIAN DATA: Core Inflation Lower, Need More Data To Ascertain Trend

July headline CPI inflation moderated to 3.5% y/y from 3.8%, slightly higher than expected, driven by lower electricity prices from government subsidies. The trimmed mean moderated to 3.8% from 4.1%, lowest since January, and ex volatile items to 3.7% from 4.0%, but few services components are updated in the first month of the quarter. The RBA is likely to look through July and wait for August and especially Q3 data.

- The ABS said that electricity prices fell 5.1% y/y after rising 7.5% y/y in June due to government rebates resulting in a 6.4% m/m drop. Excluding relief, electricity inflation would have been +0.9% y/y. Federal subsidies were first rolled out in Queensland and WA in July and the rest of the country will receive them in August, thus this month’s headline CPI will be impacted too. WA, Queensland and Tasmania also received state relief.

- Goods inflation rose 2.8% y/y in July down from 3.4%, while tradeables picked up 0.2pp to 1.5%. The latter appeared to trough in December 2023.

- Services inflation increased 0.1pp to 4.4% y/y but non-tradeables eased 0.5pp to 4.5%.

- In terms of housing, there was a slight moderation in rents to 6.9% y/y from 7.1% and builders continue to pass on higher labour and material costs for new builds.

- The pickup in fruit & vegetable prices added to food inflation, which rose 0.5pp to 3.8% y/y.

Source: MNI - Market News/ABS

NZGBS: Cheap Despite Weak Labour Market Data

NZGBs closed near session cheaps, with benchmark yields 1-4bps higher.

- July filled jobs fell 0.1% m/m, the fourth straight monthly decline, to be down 0.5% y/y, the lowest annual growth since April 2010. Given that employment data is quarterly, and the next update is not until November 6 and filled jobs are on the RBNZ’s list of high-frequency data.

- The series is an important gauge of labour market trends. To that end, the data signals weak labour demand continued at the start of Q3. This suggests cuts at the RBNZ’s two remaining 2024 meetings are likely.

- "Weakness in the NZ housing market will persist this year but a recovery is ahead in 2025 as the RBNZ cuts interest rates and lenders follow suit with mortgages, ANZ Bank NZ says in an emailed note." (per BBG)

- Swap rates closed flat to 2bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed flat to 2bps firmer across meetings. A cumulative 72bps of easing is priced by year-end.

- Tomorrow, the local calendar will see ANZ Business Confidence ahead of ANZ Consumer Confidence and Building Permits on Friday.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$200mn of the 4.50% May-35 bond and NZ$50mn of the 2.75% May-51 bond.

NEW ZEALANDS DATA: Filled Jobs Show Weak Labour Demand At Start Of Q3

July filled jobs fell 0.1% m/m, the fourth straight monthly decline, to be down 0.5% y/y, the lowest annual growth since April 2010. Given that employment data is quarterly and the next update is not until November 6 and filled jobs are on the RBNZ’s list of high frequency data, the series is an important gauge of labour market trends. It is signalling weak labour demand continued at the start of Q3 and so cuts at the RBNZ’s two remaining 2024 meetings are likely.

- July SEEK job ads rose 3.4% m/m after five consecutive falls. While this was the largest monthly increase in over two years, vacancies are still down 28.6% on a year ago. Given the weakness in the economy, it is unlikely to mark a turning point but will be interesting to watch.

- Statistics NZ noted that the fall in July filled jobs was broad-based across age groups. The total fell 0.8% 3m/3m but 15-24 year olds declined 3.1% and 25-34 yrs -1.8% and even over 35yrs -0.5%. Younger people are not only likely to be impacted the most by a labour market slowdown but also lead other age groups.

- The sectors that young people tend to be employed in saw a large fall in filled jobs with accommodation and food services down 6.7% y/y.

- Other weak sectors included construction down 7.2% y/y and admin -12.7% y/y.

- Filled jobs are collected through payroll reporting.

Source: MNI - Market News/SEEK/Statistics NZ

FOREX: A$ Tests 0.6800 Resistance Post CPI Beat, USD Pushes Higher Elsewhere

The A$ has outperformed so far in Wednesday trade, aided by a monthly CPI beat. The currency has been testing key resistance around the 0.6800 level The other majors, most notably yen, are down against the USD at this stage.

- The Australian July CPI eased further but not as much as the market expected (printing at 3.5% y/y, versus 3.4% forecast). The outcome is unlikely to impact RBA thinking, but Australian OIS and government bond yields were higher post the print.

- For AUD/USD a clean break would reinforce the bullish trend, with sights on 0.6839 the Jan 2 the next upside target.

- A$ gains have likely been curbed to a degree by weaker region equities, particularly in North East Asia, weighed by China tech earning headwinds. US equity futures are in the red, albeit up from session lows, as the market awaits earnings from tech bellwether Nvidia late in the US Wednesday time.

- AUD/JPY has fallen short of a fresh test of the 20-day EMA but is still up on the day, last near 98.15/20. NZD/USD is down a touch, last near 0.6245.

- USD/JPY has gravitated higher for much of the session, last near 144.45/50, around 0.35% weaker. BoJ Deputy Governor Himino spoke and didn't deviate dramatically away from what Ueda has said recently. The central bank must be vigilant to market volatility, but can adjust the degree of easing if certainty around the outlook firms.

- US yields have ticked a touch higher, which has likely lent some support to USD/JPY. EUR/USD is down around 0.20% to 1.1160. The BBDXY is up 0.15% to 1227.4.

- Looking ahead, the Fed’s Waller and Bostic speak. The data calendar is light with only euro area July M3 of note.

ASIA STOCKS: Equities Struggle Ahead Of Nvidia Earnings

Asian markets are mostly lower today, with Chinese technology stocks leading the decline amid disappointing earnings from major companies like Nongfu Spring and SenseTime. The HSTech Index is under pressure, and mainland Chinese stocks are also struggling. Sentiment is weak across the region as investors remain cautious ahead of Nvidia's highly anticipated earnings report. Japanese & South Korea equities are mixed as we have seen a late bounce in some of the major tech stocks names with Taiwanese names benefitting the most, while the Australian market is weighed down by concerns over inflation following a hotter-than-expected CPI reading.

- Japanese equities are off earlier lowers with the Topix now up 0.15%, while the Nikkei is now unchanged. Investors are awaiting Nvidia’s earnings report, which is expected to significantly impact market sentiment. Shares in Seven & i Holdings Co. dropped 4% following news of the company seeking government protection, potentially complicating the buyout proposal.

- South Korean equities were higher on the open although we have since given back all gains with the KOSPI down 0.30%. Major tech stocks are well off earlier lows with SK Hynix now up 1.50%, while Samsung trades up 0.40% after both trading in the red earlier. Foreign Investors have been better sellers of local stocks today with most outflows coming from tech stocks, totaling -$130m so far today.

- Hong Kong and mainland Chinese markets are under pressure today, driven by disappointing earnings reports from key companies like Nongfu Spring and SenseTime. The HStech Index is leading the selloff, down 1.90%. Elsewhere Property indices continue to trade lower as investors continue to grow concerned around a lack of policy updates and support, the Mainland Property Index is down 2.15%, HS property Index down 0.70%, while the CSI300 Index is down 0.70%, while the HSI is 1% lower, and hte CSI 300 is down 0.75%. Investors remain cautious amid weak corporate performance and ongoing economic concerns, contributing to broad-based losses in both Hong Kong and mainland markets.

- Taiwanese equities are higher today, with TSMC up 1.80% & Hon Hai up 2.20% leading the way. There has been very few headlines out of the region recently, while foreign investors have again started to sell local stocks with the past two session seeing a total outflow of $555m. The Taiex Index is currently trading up 0.70% at 22,340, after earlier trading testing the 20 & 50-day EMAs at 22,150.

- Australian equities are lower following higher-than-expected Australian inflation data, which increased concerns about potential interest rate hikes by the RBA, with the OIS market now pricing in 23bps of cuts by the December meeting, down from 27.5bps on Tuesday. The ASX200 is currently 0.30% lower. New Zealand equities are also lower today with the NZX50 down 0.10%.

- In Asia EM equities today, Indonesian's JCI is up 0.20%, Malaysia's KLCI is 1% higher, Philippines PSEi is 0.25% higher, although it should be noted that FX trading has been closed due to monsoon rains and could be also impacting equity trading, while Singapore's Straits Times is down 0.50%.

HIGH YIELDS: Global IG & HY Yields At 2yr Lows

Investors have been piling into Global High Yield Indices since the August 5th market sell off, with the yield on the BBG High Yield Index falling about 60bps from Aug 5 highs or 35bps from prior, while yields on IG bonds have held steady since.

- Global IG yields have been fallen 51bps in yield since the start of July, with all those move happening before Aug 5.

- Global HY yields saw some early July move lower, although the move has accelerated post the Aug 5 sell-off, with yields now at the lowest since June 2022.

- Flows into US High Yield funds have also increased over the month with the BFFUEHY Index (HY) showing m/m inflows of 2.07b, vs m/m outflows for the BFFUEAG Index (IG) of 100m.

ASIA EQUITY FLOWS: Investors Continue Selling Tech Stocks Ahead Of Nvidia Earnings

- South Korea: South Korea experienced an outflow of $306m on Tuesday, leading to a net outflow of $1.07b over the past five trading days. Year-to-date, however, the country has accumulated substantial inflows totaling $17.08b. The recent 5-day average shows an outflow of $214m, while the 20-day average shows an outflow of $74m, and the 100-day average inflow is $46m.

- Taiwan: Taiwan recorded an outflow of $269m on Tuesday, contributing to a net outflow of $489m over the past five trading days. Year-to-date, Taiwan has seen outflows totaling $8.35b. The 5-day average shows an outflow of $98m, while the 20-day average indicates an outflow of $93m, and the 100-day average shows an outflow of $135m.

- India: India saw an inflow of $116m on Monday, leading to a net inflow of $1.23b over the past five trading days. Year-to-date, India has accumulated inflows totaling $2.67b. The 5-day average inflow is $246m, while the 20-day average shows an outflow of $102m, and the 100-day average remains slightly positive at $12m.

- Indonesia: Indonesian equities recorded an outflow of $35m on Tuesday, ending a 14-day run of inflows, the region still has seen a net inflow of $411m over the past five trading days. Year-to-date, Indonesia has accumulated inflows totaling $883m. The 5-day average inflow is $82m, with a 20-day average inflow of $51m, although the 100-day average shows a small outflow of $9m.

- Thailand: Thailand experienced an inflow of $32m on Tuesday, contributing to a net inflow of $129m over the past five trading days. Year-to-date, Thailand has seen outflows amounting to $3.44b. The 5-day average shows an inflow of $26m, while the 20-day and 100-day averages reflect outflows of $7m and $15m, respectively.

- Malaysia: Malaysia recorded an inflow of $38m on Tuesday, contributing to a net inflow of $167m over the past five trading days. Year-to-date, Malaysia has seen inflows totaling $388m. The 5-day average inflow is $33m, while the 20-day average shows a modest inflow of $15m, and the 100-day average reflects a small inflow of $6m.

- Philippines: The Philippines recorded an inflow of $16m on Tuesday, contributing to a net inflow of $129m over the past five trading days. Year-to-date, the Philippines has experienced outflows totaling $346m. The 5-day average inflow is $26m, aligning with the 20-day average inflow of $5m, but the 100-day average still reflects an outflow of $5m.Table 1: EM Asia Equity Flows

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -306 | -1072 | 17076 |

| Taiwan (USDmn) | -269 | -489 | -8348 |

| India (USDmn)* | 116 | 1229 | 2673 |

| Indonesia (USDmn) | -35 | 411 | 883 |

| Thailand (USDmn) | 32 | 129 | -3435 |

| Malaysia (USDmn) | 38 | 167 | 388 |

| Philippines (USDmn) | 16 | 129 | -346 |

| Total | -410 | 504 | 8890 |

| * Up to Date 26-Aug-24 |

OIL: Crude Retains Tuesday’s Losses, US EIA Inventory Data Out Later

After a technical-driven drop of around 2% on Tuesday, oil prices are slightly higher today with risk sentiment generally weaker. Brent is up 0.1% to $79.61/bbl after a high of $80.01 and WTI is 0.1% higher at $75.60/bbl following $75.95. USD index is 0.1% higher.

- Oil prices rallied recently driven by oil specific factors such as continued trouble in the Middle East and the politically-motivated closing of Libyan oil fields. But Goldman Sachs and Morgan Stanley have cut their 2025 crude forecasts due to soft demand from China related to the economy but also the switch to EVs, according to Bloomberg. It is the world’s largest oil importer. These trends are also likely to impact European demand.

- OPEC plans to reduce its output cuts from October, which is also adding uncertainty to market pricing, but it also said that its intention remains flexible.

- Bloomberg reported a 3.4mn barrel US crude drawdown last week with gasoline down 1.86mn and distillate -1.41mn. The official EIA data is published later today.

- Later the Fed’s Waller and Bostic speak. The data calendar is light with only euro area July M3 of note.

GOLD: Hovering Near All-Time Highs

Gold is 0.4% lower in today’s Asia-Pac session, after closing 0.3% higher at $2524.64 on Tuesday.

- Bullion was assisted higher by the slightly lower US yields and accompanying greenback weakness, which kept the yellow metal hovering close to all-time highs.

- Nevertheless, US Treasuries have largely consolidated their move richer following Chair Powell’s Jackson Hole speech ahead of the weekend. With little on the US data docket until Thursday's claims data, the market has basically taken a breather.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- According to MNI’s technicals team, the recent breach of resistance at $2483.7, the Jul 17 high, confirmed a resumption of the primary uptrend. Note that moving average studies remain in a bull-mode set-up and this continues to highlight a dominant uptrend. The focus is on a climb towards $2536.4 next, a Fibonacci projection.

ASIA FX: North Asia FX Falter Amid Weaker Yen/Equity Headwinds

North East Asia FX has faltered somewhat today. Yen weakness and equity losses have been headwinds. The higher beta won has seen the largest drop so far today. USD/KRW remains sub recent highs though.

- USD/CNH is back above 7.1300, although has found selling resistance near 7.1340, which marked Tuesday highs in the pair. The USD/CNY fixing was close to neutral, while onshore equities continue to struggle. The CSI 300 is off 0.60% and sub 3300 in index terms. Earnings worries are offsetting share buy backs.

- Investors remain cautious ahead of Nvidia's highly anticipated earnings report. In South Korea the Kospi is off 0.30%. USD/KRW spot is up around 0.40%, last near 1337. Recent highs in the pair were close to 1344. We continue to see outflows from the local equity space. The government is looking to boost consumption as part of its broader stimulus plans.

- Spot USD/TWD is a little higher, but still sub the 32.00 level. The Taiex is higher on the day, outperforming other North East Asian equity indices so far. The 1 month NDF is off around 0.30%, last near 31.80.

ASIA FX: SEA FX More Mixed, BoT States Baht Gains In Line With Regional FX

South East Asian FX has been more mixed. Equity trends have been more mixed compared to North Asia, with Malaysia and Indonesian markets firmer in Wednesday trade. Modest THB and IDR spot gains are evident, while steady trends are evident elsewhere. USD/MYR upticks continue to be sold.

- USD/THB has spent much of the session sub 34.00, although support has emerged this afternoon. Like other parts of South East Asia FX , USD/THB has been in oversold territory in recent weeks. The BoT Governor has been on the wires today stating that the central bank is monitoring baht movements very closely but that the movement is in line with regional currencies. In the past 3 months the baht has been a clear standout in the space, along with MYR, both up nearly 8% in spot terms. THB still lags in terms of YTD performance, with SGD and MYR the strongest gainers so far this year. The rise in gold and shift in Fed expectations were cited as Baht positives.

- USD/IDR opened higher, but found selling interest above 15500. The pair was last near 15480. Overseas investors were buyers of Indonesia equity in August, likely the biggest monthly purchases since April 2022, while net inflows into bonds are the strongest this year. (Source: Bloomberg).

- USD/MYR opened weaker, but is up from earlier lows. Still the pair remains sub the 4.3500 level. Malaysia must keep the door open for further monetary policy tightening to tamp down any price pressures as the government winds down subsidies, according to the OECD (Source: OECD Economic Survey on Malaysia).

THAILAND: BoT Remains Focused On The Outlook

The Bank of Thailand’s (BoT) August statement sounded more dovish without signalling imminent rate cuts. It seemed more concerned regarding growth, inflation and financial stability. Headline inflation is now “expected to decline relative to previous assessment” but Governor Sethaput said today that low inflation doesn’t mean deflation and that structural factors persist. BoT focuses on the outlook and not individual data points and Sethaput reiterated that saying that policy will be “outlook dependent”.

- Some forecasters brought forward BoT rate cut expectations following the August meeting. The Q3 Bloomberg survey published this week has 12bp of easing in Q4 2024 with a full 25bp by Q1 2025 and a total of 41bp by Q4 2025, so still modest. But 10 of the 27 responses expect a 25bp cut in Q4 2024.

- BoT easing requires the Fed to cut first, which is expected in September. While there are BoT meetings in October and December, Sethaput’s comments today didn’t sound like the central bank is in a hurry to ease. BoT will adjust monetary policy if needed and won’t be “dogmatic”. He noted that it also has other tools to complement monetary policy, which is set to achieve a number of outcomes.

- Disappointing economic growth could drive a more dovish stance. Sethaput said that the recovery is “uneven” and that there is a growing gap between consumption and manufacturing growth.

- Reducing the household debt ratio has been one of the reasons that BoT has kept rates around “neutral” and Sethaput today said that its aim is to bring it down to around 80% over the long term. Only a third of debt is mortgages with the majority from hire purchases and so BoT’s debt goal will remain important.

BOK Governor Continues to Target Housing Sector.

- BOK Governor Rhee doubled down on recent comments about the housing sector characterizing last week’s decision on rates a ‘wake up call’.

- “This decision reflected the hope to raise an alarm at least once that this vicious cycle (of real estate and household debt growth) is not desirable,” Rhee said yesterday.

- His comments come at a time when officials from the Presidential Office have expressed their disappointment over the BOK’s decision to leave rates on hold for the 13th month straight, raising concerns about domestic consumption.

- Korea has one of the highest household debt levels in the region, an area of concern that the BOK governor has spoken to consistently.

- Whilst the BOK’s independence is not in question, this shows the dichotomy that exists within the economy at present at a time when government plans are underway to provide fiscal support to the economy to boost consumption.

INDONESIA: Consensus Expecting At Least One 25bp Rate Cut In Q4 2024

Bank Indonesia (BI) left rates unchanged at 6.25% at its August 21 meeting and there was little change to the statement. Although there were signs that policy has begun to be normalised with SRBI rates lower and portfolio flows expected to switch into bonds. BI’s focus has been FX stability for some time and it has even hiked to defend the rupiah. With the first Fed cut widely expected for September 18, BI easing in Q4 looks likely.

- BI also meets on September 18 but given it announces before the Fed, we don’t expect the start of an easing cycle that day. Also, BI has been using macroprudential policies to support the economy and so it doesn’t have to risk recent rupiah appreciation by immediately following the Fed.

- Bloomberg’s August survey showed few believe there will be a BI rate cut in September but 33bp of easing are forecast for Q4 2024 with another 71bp by Q4 2025. BI meets monthly and so it can be flexible. Two of the 22 analysts in the survey expect a 25bp rate cut in September but only 3 of 26 don’t expect one in Q4 2024. 13 forecasters project 25bp, so only one cut in the three Q4 meetings, while 10 believe there will be two.

- Headline inflation is expected to pickup to 2.6% in Q4 2024 from July’s 2.1% and then be stable through 2025 ending the year at 2.8%.

- Consensus is forecasting GDP to continue running at around 5.0-5.1% y/y. Q3 2024 is expected to rise 0.5% q/q.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/08/2024 | 0600/1400 | ** |  | CN | MNI China Liquidity Index (CLI) |

| 28/08/2024 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 28/08/2024 | 0800/1000 | ** |  | EU | M3 |

| 28/08/2024 | 0900/1000 | * |  | UK | Index Linked Gilt Outright Auction Result |

| 28/08/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 28/08/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 28/08/2024 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 28/08/2024 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 28/08/2024 | 2200/1800 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.