Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

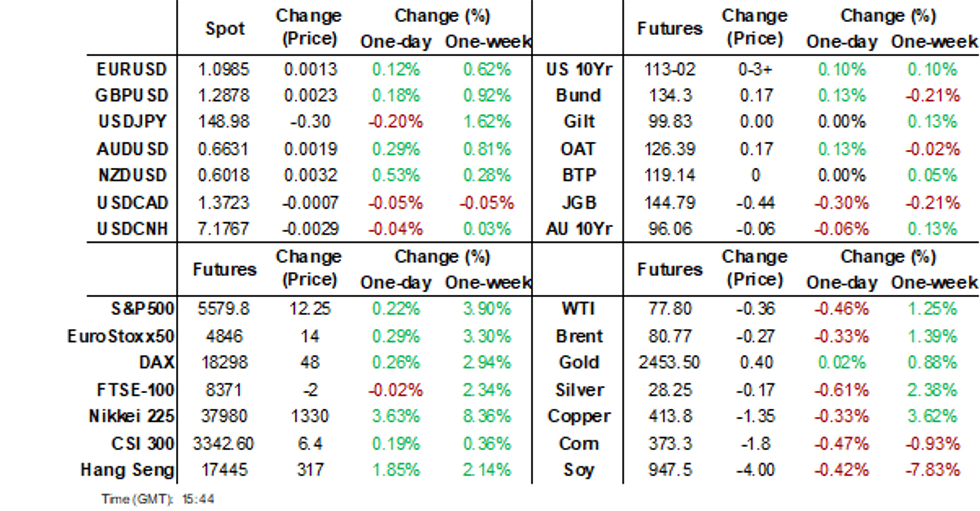

- Regional risk appetite remained positive in the equity space, as carry over from the US Thursday session saw recession fears ease further. China equities are absent from the rebound, as lingering growth concerns remained a headwind. Similarly, iron ore is hold close to the week's lows, not bouncing with other metals.

- The USD weakened in the FX space, with higher beta plays mostly continuing to outperform. JPY and CHF are slightly firmer, but still remain comfortably lower for the week.

- US Treasury futures have ticked higher today, although we now trade slightly off session's best.

- Looking ahead, we have UK retail sales, while in the US, building permits and UMich sentiment data will close out the week.

MARKETS

US TSYS: Tsys Futures Edge Higher, Curve Slightly Steeper

- Treasury futures have ticked higher today, although we now trade slightly off session's best. TUU4 is + 01¼ at 103-04, while TYU4 is + 03+ at 113-02.

- Cash treasury curves are bull-steepening today, yields are 1-3bps lower, short-end outperforming although it did underperform overnight. The 2yr is -2.2bps at 4.071%, while the 10yr is -1.1bp at 3.902%.

- St Louis Fed Pres Musalem is one of the most hawkish members of the FOMC, but his comments overnight suggest he is falling in line with the Fed leadership's view that risks to the inflation vs employment mandates have come into balance - (See link)

- In June, Japanese investors sold a net $30.1 billion in U.S. Treasuries, marking the largest monthly sell-off since September 2022 and the third consecutive month of reductions

- Projected rate cuts through year end have moderated vs. Thursday's pre-data levels (*): Sep'24 cumulative -33.5bp (-35.2bp), Nov'24 cumulative -62.4bp (-69.6bp), Dec'24 -95.3bp (-104.1bp).

- Looking ahead we have Housing Start, Building Permits, U. of Mich. Sentiment and Chicago Fed Pres Goolsbee to speak

JGBS: Belly Of Cash Curve Underperforms, Carry Trade Is Back

JGB futures are weaker, -40 compared to the settlement levels.

- Outside of the previously outlined international investment flow data, there hasn't been much in the way of domestic drivers to flag. The Tertiary Industry Index fell 1.3% m/m in June versus +0.3% estimate.

- (Bloomberg) "Nomura Holdings Inc., Japan’s biggest brokerage, has seen a variety of investors start borrowing the yen again to invest the proceeds elsewhere in higher-yielding assets. It suggests corporate clients and hedge funds, who have been enthusiastic carry traders, are getting back into those deals." (See link)

- Cash US tsys are 1-3bps richer, with a steepening bias, in today’s Asia-Pac session after yesterday’s sharp sell-off following stronger-than-expected data.

- Cash JGBs are 2-5bps cheaper, with the belly of the curve underperforming. The benchmark 10-year yield is 4.1bps at 0.880% versus the cycle high of 1.108%.

- Swaps are mixed, with rates 2bps lower (7-year) to 3bps higher (40-year).

- On Monday, the local calendar will see Core Machine Orders data alongside 1-year supply. 20-year supply is due on Tuesday.

JAPAN DATA: Offshore Investors Bought Local Equities & Bonds Last Week

Last week offshore investors returned to both Japan equities and bonds. In the equity space, we had the first weekly inflow since mid June. Since the start of June, net inflows are close to flat for this segment. Last week's price action in Japan equities was a steady recovery from Monday's sharp slump. Offshore investors may have used that pull back to rebuild some long positions. In the bond space, we saw inflows into this space as well, more than offsetting the prior week's outflow. Still, the broader trend around these flows is close to flat since the start of June.

- Japan buying of offshore bonds was quite strong for the second straight week. As global monetary policy starts to turn, local investors may see offshore bonds more attractive, particularly on an FX hedged basis. Still, the trend back to June remains for net selling by local investors in terms of offshore bonds.

- Local investors sold overseas equities last week, but this only marginally offset the prior week's outflows into this asset segment.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending August 9 | Prior Week |

| Foreign Buying Japan Stocks | 521.9 | -643.7 |

| Foreign Buying Japan Bonds | 1435.0 | -1160 |

| Japan Buying Foreign Bonds | 1539.2 | 677.7 |

| Japan Buying Foreign Stocks | -328.1 | 1288.1 |

Source: MNI - Market News/Bloomberg

STIR: NZ Outperforms $-Bloc After RBNZ Eases

STIR markets within the $-bloc have delivered mixed net results over the past week, with New Zealand outperforming and the US underperforming.

- Year-end official rate expectations softened 13bps in New Zealand over the past week following the RBNZ’s decision on Wednesday to cut the OCR by 25bps to 5.25%. Going into the meeting, the market had priced a 58% chance of a 25bp cut. The market now prices 35bps of easing for the next meeting, with a cumulative 79bps by November.

- By contrast, the US market has seen year-end official expectations firm 12bps over the past week as US recession risks have been priced out.

- Overnight, better-than-expected retail sales and jobless claims data saw the probability for a 50bps cut pared. The market is pricing ~32bps of easing at the September FOMC, with 88bps by year-end.

- There was little net movement in year-end expectations in Canada or Australia.

- The December 2024 expectations and the cumulative easing across the $-bloc are as follows: 4.45%, -88bps (FOMC); 3.78%, -72bps (BoC); 4.11%, -21bps (RBA); and 4.46%, -79bps (RBNZ).

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

AUSSIE BONDS: Cheaper But Near Session Bests, RBA Minutes On Tuesday

ACGBs (YM -7.0 & XM -5.0) are weaker but near Sydney session highs on a light-data day.

- Outside of the previously outlined RBA Governor Bullock’s testimony, there hasn't been much in the way of domestic drivers to flag.

- The latest round of ACGB May-28 supply saw the weighted average yield print 0.8bps through prevailing mids, extending the recent trend of firm pricing at ACGB auctions. However, the cover ratio fell to 3.8286x from 4.0778x at the July auction. A significantly lower outright yield likely impacted bidding.

- Cash US tsys are 1-3bps richer, with a steepening bias, in today’s Asia-Pac session after yesterday’s sharp sell-off following stronger-than-expected data.

- Cash ACGBs are 5-6bps cheaper after paring earlier losses (was 10-11bps cheaper).

- The AU-US 10-year yield differential is +3bps.

- Swap rates are 5-6bps higher, with EFPs slightly tighter.

- The bills strip has bear-steepened, with pricing -2 to -9.

- RBA-dated OIS pricing has moved 4-8bps firmer across meetings beyond November. A cumulative 19bps of easing is priced by year-end.

- Next week, the local calendar is empty on Monday, ahead of the RBA Minutes of August Policy Meeting on Tuesday.

- The AOFM plans to sell A$800mn of the 3.00% 21 November 2033 bond on Wednesday and A$700mn of the 2.75% 21 November 2028 bond on Friday.

NZGBS: Closed Little Changed But At Session Highs

NZGBs closed little changed but a dramatic improvement from earlier in the session when they were as much as 6-7bps cheaper.

- Apart from the previously mentioned Manufacturing PMI and PPI data, there have been few notable domestic influences.

- Notwithstanding today’s cheapening, NZGBs remain 9-25bps richer than Wednesday’s pre-RBNZ decision levels. The 2/10 curve is 16bps steeper.

- The move away from session cheaps was assisted by cash US tsys, which are 1-3bps richer in today’s Asia-Pac session.

- NZ-US 10-year yield differential is 8bps tighter at +23bps. The differential has traded in a +15 to +85bps range over the past 12 months.

- Swap rates closed 1bp lower to 2bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is 4-6bps firmer for meetings out to Apr-25. A cumulative 79bps of easing is priced by year-end.

- Next week, the local calendar will see the Performance Services Index on Monday, REINZ House Sales and Trade Balance data on Tuesday and Q2 Retail Sales Ex Inflation on Friday. Also, RBNZ Deputy Hawkesby Speaks on Tuesday.

FOREX: Dollar Pares Recent Gains, NZD/USD Up On Continued Positive Global Equity Tone

Friday G10 FX trends have been skewed against the USD in the first part of trade. NZD/USD has led gains, up nearly 0.40%, although both JPY and CHF have ticked higher as well, even with a positive regional equity backdrop.

- The BBDXY index is less than 0.10% weaker, last under 1244.00. We are comfortably up from earlier lows this week, just under 1239, but we remain in a broader downtrend going back to late July highs.

- NZD/USD is the best performer, up 0.40%, to be back above 0.6010. This has pared NZD underperformance for the week (we are now up slightly), but pre RBNZ levels remain back near 0.6085. Data showed the manufacturing PMI stayed in contraction but up from recent lows.

- AUD/USD is trailing the NZD somewhat, last near 0.6625, up 0.20%, but still the second best performer in the G10 in the past week. Comments from RBA Governor Bullock before Australian parliament today stated the board is not considering an easing in the near term. AUD/NZD sits back at 1.1020, off recent highs near 1.1060. Iron ore is continuing to soften, not following other metals higher, which is a potential AUD headwind.

- USD/JPY has fallen, last under 149.00. It is up 0.30% in yen terms for the session, but this only modestly pares weekly losses in yen. The receding of US recession risks has buoyed the global equity market backdrop.

- Regional equities are all a sea of green, but onshore China equities are only marginally higher.

- US yields are lower today, but holding close to unchanged for the week.

- Looking ahead, we have UK retail sales, while in the US, building permits and UMich sentiment data will close out the week.

ASIA STOCKS: Hong Kong Equities Higher With Tech Outperforming

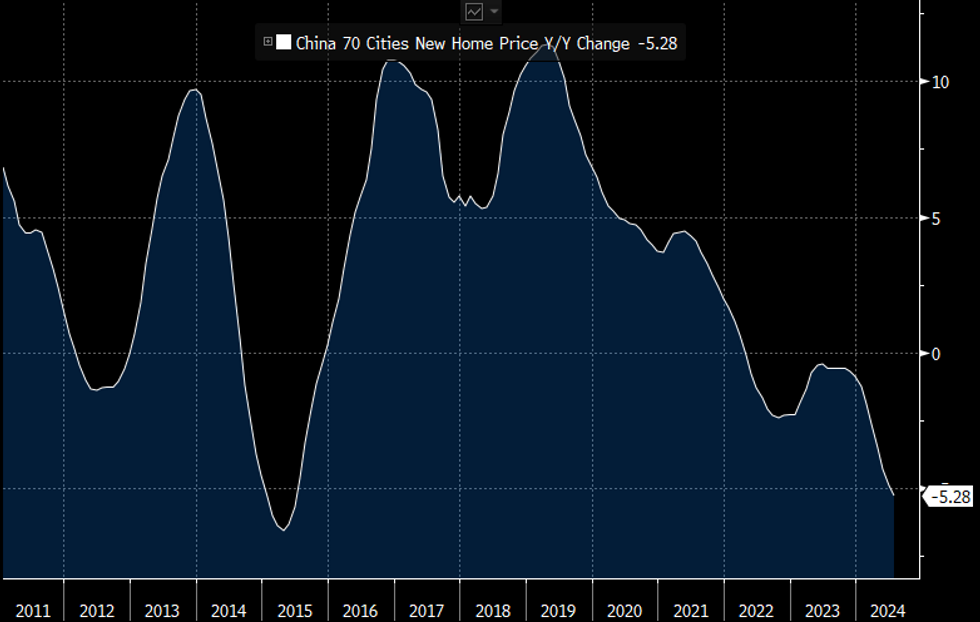

Chinese and Hong Kong markets saw mixed reactions as investors digested weak housing data out of China's after home prices in July plunged the most since 2015, with residential property sale values dropping significantly below their four-year average. Despite these downturns, the PBoC indicated no immediate rush for large-scale economic stimulus, emphasizing a strategy of "policy patience and stability." Hong Kong's HSI started strong on Friday, buoyed by gains in tech stocks like Alibaba, which surged despite reporting a nearly 30% dip in quarterly profits.

- Hong Kong markets are outperforming today with the HSI up 1.70% with tech stocks leading the way (HSTech up 2.15%), property indices have underperformed with (Mainland unch, HS Property -0.37%). China onshore equities are little changed with CSI 300 up 0.04%, small-caps are mixed with the CSI 1000 down 0.30%, while the CSI 2000 is up 0.22%.

- China's central bank chief, Pan Gongsheng, pledged further measures to support the country's economic recovery but emphasized avoiding drastic policy changes. He highlighted the importance of maintaining price stability amid deflationary risks and indicated a gradual shift towards using interest rates over quantitative targets as key monetary tools. Pan also reaffirmed the PBOC's commitment to a supportive monetary policy while acknowledging the relative stability of China's financial system, as per BBG

- China's new home prices in July saw their largest y/y decline since 2015, deepening the bear market for homebuilder stocks.

ASIA PAC EQUITIES: Asian Equities Look To End Week Higher On Tech Rally

Asian markets are rallying today, buoyed by optimism that the US economy will avoid a recession. Almost all major stock benchmarks across the region are up, with a regional gauge poised for its best weekly performance in over a year. Japanese equities are leading the gains, benefiting from a weaker yen which has helped exporters, the currency has fallen significantly against the dollar, easing concerns of a carry trade unwind. The Hong Kong equities saw gains, supported by Alibaba and JD.com posting better-than-expected profits. Meanwhile, China’s central bank pledged more measures to support economic growth, although without drastic interventions. Overall, the Asian markets are extending a recovery from last week’s volatility, driven by positive US economic data and strong performances in tech and export-oriented stocks.

- Japan's benchmark indices are all trading 2-4% higher today, banks again lead the way higher. The rally was fueled by strong U.S. economic data, including better-than-expected retail sales, which eased concerns about a potential recession. The weakening yen also provided a boost, particularly for export-oriented sectors like machinery and electronics. Investor sentiment was further bolstered by signs of stability in the U.S. market and positive reactions to recent domestic corporate earnings. The Nikkei is on track for its best week since April 2020, currently trading 2.90% higher, while the TOPIX is 2.5% higher.

- South Korean stocks are also higher today with the KOSPI up 2%, while the KOSDAQ is lagging although still 1.20% higher, the moves have been driven by eased U.S. recession concerns and strong gains across major sectors. Big-cap stocks led the rally, as Samsung Electronics advanced 2.46%, while SK hynix surged 6.16%, while autos have also jumped between 2-5%. Foreign investors played a key role, injecting $455 million into local equities so far today, particularly in tech stocks.

- Similar to SK, Taiwan's equity market is higher with TSMC contributing the most to the index gains, up 2%.

- Australian equities are higher, although underperforming other region markets. Financials & Materials are the top performers. Earlier, RBA gov Bullock ruled out rate cuts this year, after concerns that inflation is falling very slow. The ASX200 is 1.25% higher today. New Zealand equities are 0.30% today.

- In the Asia EM space, all markets are higher with Indonesia's JCI up 0.40%, Singapore's Strait Times 1.15% higher, Malaysia's KLCI up 0.50%, Philippine's PSEi is up 1.70% higher.

ASIA EQUITY FLOWS: Equities Mostly Recover From Aug 5, Flows Yet To Fully Return After Sell-Off

- South Korea: South Korean was out Thursday for a Public holiday, however over the past 5 trading sessions we saw a net outflow of $220m. Both the KOSPI & KOSDAQ still trade slightly below pre Aug 2nd levels, although the KOSDAQ is slightly outperforming, there is still net outflows of $1.6b since August 5nth. The 5-day average outflow is $44m, compared to the 20-day average outflow of $117m and the 100-day average inflow of $85m. Year-to-date, South Korea has had substantial inflows totaling $17.061b.

- Taiwan: Taiwan recorded an inflow of $445m yesterday, with a net inflow of $2.252b over the past five trading days. The Taiex has recovered all losses made on August 5th, although we still have net outflows of $3.45b since then. The 5-day average inflow is $450m, compared to the 20-day average outflow of $570m and the 100-day average outflow of $157m. Year-to-date, Taiwan has experienced outflows totaling $9.740b.

- India: Indian equities saw an outflow of $169m yesterday, with a net outflow of $919m over the past five trading days. The Nifty 50 has been one of the worst performing benchmark indices post August 5th only recovering 1%, while outflows have increased. The 5-day average outflow is $184m, compared to the 20-day average outflow of $63m and the 100-day average inflow of $18m. Year-to-date, India has seen inflows totaling $1.793b.

- Indonesia: Indonesian equities recorded an inflow of $40m yesterday, resulting in a net inflow of $167m over the past five trading days and has mark 7 straight session of inflows, the JCI has been one of the top performers and now trades 1.45% August 5th highs. The 5-day average inflow is $33m, compared to the 20-day average inflow of $20m and the 100-day average outflow of $8m. Year-to-date, Indonesia has had inflows totaling $277m.

- Thailand: Thai equities saw an outflow of $15m yesterday, leading to a net outflow of $10m over the past five trading days. Flows have been mixed into the SET recently, with no real trend emerging, the index has also struggled to recover from the August 5th sell-off and only trades 1.25% off the lows. The 5-day average outflow is $2m, compared to the 20-day average inflow of $2m and the 100-day average outflow of $24m. Year-to-date, Thailand has experienced outflows amounting to $3.321b.

- Malaysia: Malaysian equities had an inflow of $6m yesterday, resulting in a 5-day net outflow of $27m. The Malay KLCI has fully recovered from the August 5th sell-off. The 5-day average outflow is $5m, which is worse than the 20-day average outflow of $9m and in line with the 100-day average outflow of $0m. Year-to-date, Malaysia has experienced outflows totaling $36m.

- Philippines: The Philippines recorded no inflow or outflow yesterday, with a net inflow of $15m over the past five trading days, flows recently have been very muted, the PSEi has recovered from the August 5 sell-off while the BSP cut rates late yesterday. The 5-day average inflow is $3m, compared to the 20-day average inflow of $1m and the 100-day average outflow of $7m. Year-to-date, the Philippines has seen outflows totaling $486m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn)* | 349 | -220 | 17061 |

| Taiwan (USDmn) | 445 | 2252 | -9740 |

| India (USDmn)* | -169 | -919 | 1793 |

| Indonesia (USDmn) | 40 | 167 | 277 |

| Thailand (USDmn) | -15 | -10 | -3321 |

| Malaysia (USDmn) | 6 | -27 | -36 |

| Philippines (USDmn) | 0 | 15 | -486 |

| Total | 656 | 1258 | 5547 |

| * Up to Date 14-Aug-24 |

OIL: Higher For The Week as Recession Fears Lowered, Middle East Tensions Continue.

- Oil moved higher over night on simmering tensions in the Middle East as concerns over a potential attack on Israel by Iran intensifies.

- Having traded up towards 81.50 overnight, Oil gave back some early gains in the Asia session trading at $80.86, representing a 1.5% increase on the week.

- West Texas Intermediate briefly traded above $78 a barrel before settling at $77.92 during the Asian market session, representing a 1.3% increase on the week.

- Data throughout Asia this week was mixed with China posting a 8% yoy decline in demand whereas Singapore exports saw a marked increase.

- Overnight data from US offset the data from Asia pointing to a more robust US economy than expected.

GOLD: Rises Despite Stronger Than Expected US Data

Gold is 0.2% lower in today’s Asia-Pac session, after closing 0.4% higher at $2456.79 on Thursday.

- Broad dollar strength in the aftermath of stronger US data yesterday had a very brief negative impact on the yellow metal. Spot gold swiftly recovered to finish moderately higher on the session.

- July's advance retail sales report showed that the recent unexpected pickup in consumer momentum continues. June retail sales came in well above expectations at 1.0% M/M (0.4% expected, -0.2% prior rev from 0.0%).

- Initial jobless claims surprised lower for the second consecutive week with a seasonally adjusted 227k (cons 235k) in the week to Aug 10 after a marginally upward revised 234k (initial 233k).

- 2-year yields spiked 14bps to 4.09% as investors reduced expectations for aggressive easing by the Fed. 10-year yields rose 8bps to 3.91%.

- Higher rates are typically negative for gold, which doesn’t pay interest.

- According to MNI’s technicals team, attention remains on $2483.7, the Jul 17 high and a bull trigger. Clearance of this hurdle would resume the technical uptrend.

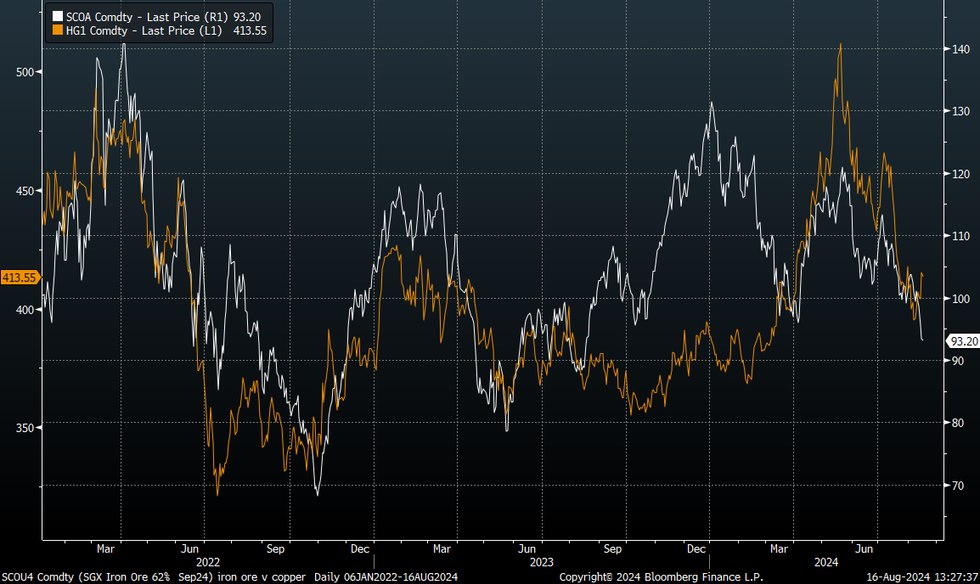

METALS: Iron Ore Not Bouncing With Other Metals

Iron ore is holding close to this week's lows. The active SGX contract last near $93.00/ton. Yesterday's lows at $92.65/ton mark recent lows, while an earlier spike above $95.00/ton wasn't sustainable.

- Broader risk appetite has stabilized as this week has progressed, with global equity sentiment continuing to improve as US recession fears have faded based off recent data outcomes (retail sales and initial jobless claims from Thursday).

- Iron ore hasn't benefited from such trends though, particularly compared to other commodities. The chart below overlays spot iron ore versus copper prices, which highlights this divergence in the metals space.

- Likely concerns around China's local steel industry outlook are keeping iron ore under pressure. Post yesterday's July activity update, sell-side economists are mostly talking about downside risks to growth in the near term. Onshore steel pressures have stabilized somewhat but still hold close to recent lows.

- Data on China iron ore inventories, which should print later for this week, will also be in focus.

Fig 1: Iron Ore Not Bouncing With Other Metals

Source: MNI - Market News/Bloomberg

ASIA FX: CNH Lags G10 FX Gains, KRW and TWD Aided By Tech Equity Gains

USD/CNH is back sub 7.1800, although is only down modestly on end Thursday levels. The pair is underperforming G10 gains against the USD and some parts of the Asia FX complex. China equities aren't rallying with the rest of the region. The CSI 300 is close to flat at this stage.

- Lingering growth concerns is likely weighing on some broader China related assets, which could be slowing CNH's advance at the margin. The CNY CFETS basket has tracked to multi month lows in recent sessions.

- USD/KRW is probing sub 1360, but remains above earlier August lows near 1355. The continued recovery in global equity sentiment is offsetting reduced Fed easing odds (in terms of magnitude for the September meeting). The Kospi is up nearly 2%.

- It is a similar backdrop for USD/TWD, although like USD/TWD, the pair remains a touch above recent lows. Spot sits near 32.30, with a break sub 32.25 potentially paving the way for a move towards the low 32.00 region.

- We are seeing a gradual return of offshore inflows to both South Korean and Taiwan equities, although August to date remains in negative territory.

ASIA FX: MYR & SGD Outperform On Better Data, THB & PHP Weaker Into Week's End

USD/MYR is off earlier highs, last back under 4.4400. Earlier the pair got to 4.4650. This leaves us flat for the session, outperforming the likes of PHP and THB. SGD is up though, aided by a stronger than expected bounce in export growth for July.

- Malaysia's earlier Q2 growth figures pointed to continued firm economic growth for the economy, with growth towards the upper end of the central bank's 4-5% target range for this year. This has likely helped some degree of differentiation. Recent lows just under 4.4000 will be a target for ringgit bulls. Firm local growth is being aided by repatriated offshore earnings/less offshore investment.

- Growth remains strong in the Philippines as well, but the BSP commenced its easing cycle late yesterday and Governor Remolona stated today the peso fallout should be manageable. USD/PHP is back to 57.20/25, so still comfortably off recent highs, but 0.50% weaker for the session so far.

- USD/THB is also higher, last to 35.10. The local parliament is current voting for Paetongtarn Shinawatra as the new Prime Minister, who should secure enough votes. Political uncertainty/further delays in fiscal stimulus risk undermining Thailand growth. Until the dust settles on how the new government will unfold, offshore investors may remain somewhat on the sidelines.

- USD/SGD is back close to 1.3200, aided by the better July trade figures earlier. Export growth was well above expectations and returned to a double digit pace. USD/SGD is just out of oversold conditions, so that may limit the downside in the pair.

- USD/IDR is firmer back above 15700, as a firmer US yield backdrop has provided some support for the pair. Recent lows remain intact near 15600.

Malaysia GDP: Surprises to the Upside.

- Malaysia GDP rose 5.9% in the second quarter from a year earlier.

- Bank Negara’s data release revealing that the economy is expanding at the upper end of the bank’s forecast of 4 -5% this year.

- Semiconductor and AI driven data center investment remains strong as well as inbound tourism.

- Agriculture, construction and Services were all ahead of expectations.

- Whilst government expenditure declined, consumer expenditures and investment expanded.

- This is the second time this year GDP has exceeded expectations.

- Malaysia’s GDP numbers are further evidence that Southeast Asian nations growth outlook appears to be able to weather the global uncertainties weighing down their Northeast Asian neighbors.

SINGAPORE: Exports Turn Positive for July.

- Singapore exports surprised to the upside in July rising 15.7% yoy / +12.2% mom.

- Led by an electronic exports rise of 16.5% yoy, this was welcome relief following June’s release.

- June saw a significant decline of -8.7% as electronic shipments weakened.

- The data showed large increases in exports to the US, China, Malaysia and Indonesia with declines to the EU.

China: Bond Wrap

- Shorter dated bonds finished the week higher in yield given the sell off Monday and Tuesday.

- The 10 year finished virtually unchanged for the week but importantly inside the 2.20% level deemed important by authorities.

- Data saw a mixed outcome for the week with Industrial Production expanding in line with expectations and Retail Sales surprising to the upside.

- Property investment and Residential Property Sales data however confirming the challenges that exist for the property sector and broader sentiment in China.

- Bonds resumed their rally today with short and intermediate maturity yields all lower whilst longer dated yields widened as Hubei and Sichuan issued 30yr bonds.

2yr 1.634% (-1.5bp) 5yr 1.874% (-1.1bp) 10yr 2.17% (-1bp) 30yr 2.368% (+3bps)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/08/2024 | 0600/0700 | *** |  | UK | Retail Sales |

| 16/08/2024 | 0900/1100 | * |  | EU | Trade Balance |

| 16/08/2024 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 16/08/2024 | 1230/0830 | * | | CA | International Canadian Transaction in Securities |

| 16/08/2024 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 16/08/2024 | 1230/0830 | *** |  | US | Housing Starts |

| 16/08/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 16/08/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.