Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

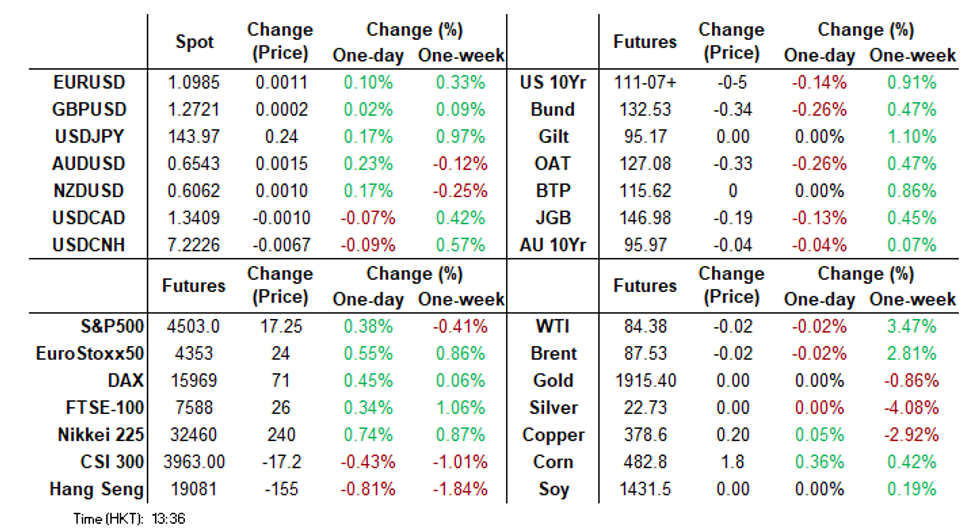

- There has been a muted session across G-10 FX in Asia today, ranges have been narrow with little follow through on moves as the market awaits the US CPI print. The Antipodeans are the strongest performers in the space, with AUD and NZD both up ~0.2% USD/JPY briefly dealt through the ¥144 handle for the first time since early July.

- USD/CNH is down slightly, while onshore equities are modestly weaker. The fallout from US investment restrictions into China technology fairly limited so far.

- In the fixed income space trading was subdued for the most part as the proximity to the aforementioned inflation print from the US limited activity. Elsewhere; Crude has been range trading during the APAC session as markets wait for July US CPI data out later but has held onto most of Wednesday’s gains. Gold is slightly higher in the Asia-Pac session, after closing 0.6% lower on Wednesday.

- Looking ahead, there is a thin docket in Europe today, further out the latest US CPI print headlines. The MNI preview of the event is here. Fedspeak from SF Fed President Daly and Atlanta Fed President Bostic also crosses. We also have the latest 30-Year supply.

MARKETS

US TSYS: Marginally Cheaper In Asia

TYU3 deals at 111-08+, -0-04, a 0-04+ range has been observed on volume of ~48k.

- Cash tsys sit ~1bp cheaper across the major benchmarks.

- Tsys have ticked lower through the Asian session, however ranges remain narrow with little follow through.

- The proximity to this evening's July US CPI print has perhaps limited activity in Asia.

- FOMC data OIS remains stable, a terminal rate of 5.40% is seen in May with ~70bps of cuts by July 2024.

- There is a thin docket in Europe today, further out the latest US CPI print headlines. The MNI preview of the event is here. Fedspeak from SF Fed President Daly and Atlanta Fed President Bostic also crosses. We also have the latest 30-Year supply.

STIR: $-Bloc Markets Steady Ahead Of US CPI Data

$-Bloc markets are steady as they await today's release of US CPI data. In fact, $-bloc STIR has maintained stability over the course of the past week. The chances of a 25bp hike at the next policy meeting sit at:

- 17% for Sep 20 (FOMC);

- 25% for Sep 6 (BoC);

- 9% for Sep 5 (RBA); and

- 9% for Aug 16 (RBNZ).

Figure 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

JGBs: Futures Holding Weaker, Narrow Range Ahead Of US CPI & Jobless Claims

In the Tokyo afternoon session, JGB futures are holding the morning’s early losses, -29 compared to settlement levels, after trading in a narrow range.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined annual PPI miss and weekly international investment flow data that showed offshore investors were large sellers of Japanese bonds.

- US tsys are sitting at session lows in Asia-Pac trade, with no obvious headline driver. This leaves cash tsys ~1bp cheaper across the major benchmarks.

- The cash JGB curve has bear steepened with yields flat to 3.2bp higher. The benchmark 10-year yield is flat at 0.584%, above BoJ's YCC old limit of 0.50% but below its new hard limit of 1.0%.

- The swaps curve has also bear steepened. Swap spreads are wider apart from the 40-year.

- Tomorrow is a public holiday in Japan.

- Later today, the US calendar sees CPI and Initial Jobless Claims data along with Fedspeak from SF Fed President Daly and Atlanta Fed President Bostic. There is also the latest 30-year supply.

AUSSIE BONDS: Subdued Trading Ahead Of US CPI

ACGBs (YM -4.0 & XM -3.5) are weaker but above Sydney session lows as global bond markets await today’s US CPI data.

- Consensus puts core CPI inflation at 0.2% m/m in July in what’s likely only a minor uptick from the unrounded 0.16% m/m in June. Analysts see two conflicting (and familiar) drivers on the month: airfares (upside) and used cars (downside). Some expect the Fed’s closely watched core services ex-housing measures to firm from particularly weak flat or near flat readings in June but to still help the trend moderate. See the MNI CPI preview here.

- US tsys have cheapened in Asia-Pac trade, sitting at session lows, with no obvious headline driver. The move aligns with JGBs moving lower. This leaves cash tsys ~1bp cheaper across the major benchmarks.

- Cash ACGBs are 3-4bp cheaper with the AU-US 10-year yield differential 2bp wider at +1bp.

- The 3s10s swaps curve bear flattens, with rates 2-3bp higher.

- The bills strip bear steepens, with pricing -1 to -4.

- RBA-dated OIS pricing is little changed, with terminal rate expectations at 4.23%.

- Tomorrow RBA Governor Lowe’s final appearance before the House of Representatives standing committee on economics headlines.

- In addition to US CPI data later today, the US calendar sees Initial Jobless Claims data.

NZGBS: Cheaper, Mixed Outcomes For Weekly Supply, US CPI Due

NZGBs closed 2-3bp weaker, mid-range, as global bonds braced for today’s US CPI data.

- US tsys are sitting at session lows in Asia-Pac trade, with no obvious headline driver. This leaves cash tsys ~1bp cheaper across the major benchmarks.

- In terms of the weekly supply, outcomes were varied. The auction of NZ$275 million worth of May-26 bonds and NZ$75 million of the 2.75% Apr-37 bonds witnessed decreased cover ratios (2.77x and 2.01x respectively). Conversely, the sale of NZ$150 million of May-32 bonds experienced an elevated cover ratio (3.01x). Nevertheless, the lines were 2-3bp richer in post-auction trading.

- Swap rates are 2-3bp higher with the 2s10s curve flatter.

- RBNZ dated OIS pricing is flat to 3bp softer, with '24 meetings leading.

- Tomorrow the local calendar sees July’s Manufacturing PMI and Food Price Index.

- In addition to US CPI data, the US calendar sees Initial Jobless Claims along with Fedspeak from SF Fed President Daly and Atlanta Fed President Bostic. There is also the latest 30-year supply.

GOLD: Steady Ahead Of US CPI

Gold is slightly higher in the Asia-Pac session, after closing 0.6% lower on Wednesday. The move was surprisingly large considering the USD index moved lower on the day.

- That said, short-end US tsy yields were higher. Nervousness over the potential for stronger-than-expected US CPI data today, which could keep the FOMC on a tightening path, appeared to encourage some position squaring. See the MNI CPI preview here.

- Core inflation is expected to fall, extending a downward trend that Bloomberg consensus believes will support a pause in monetary tightening when the Fed next meets in September. The market attaches a 17% chance of a 25bp hike at the 20 September FOMC meeting.

OIL: Crude Range Trading Ahead Of US CPI Data

Crude has been range trading during the APAC session as markets wait for July US CPI data out later but has held onto most of Wednesday’s gains. WTI is down 0.1% to $84.30/bbl and has held above $84. Brent is 0.2% lower at $87.42 after a low of $87.29. The USD index is flat.

- Brent is up 16% since the start of July and prices have broken above the previous 2023 high in April. There are signs supply is tightening with OPEC+ cutting output, US stocks declining and building tensions in the Black Sea. Futures contracts are signalling tighter supply too.

- Demand concerns persist though, especially from China, but potential LNG shortages from planned strike action in Australia heading into the northern hemisphere winter could increase demand for oil (see MNI’s Australian Strike Risk Pushing Gas Prices Higher, Inflation Risk).

- OPEC publishes its monthly report later today with the IEA’s due tomorrow.

- The focus later is on July US CPI which is expected to rise to 3.3% y/y from 3% with core down 0.1pp to 4.7% (see MNI’s US CPI preview here). The Fed’s Daly, Bostic and Harker also speak.

FOREX: Greenback Little Changed In Asia, CPI In View

The USD is little changed in Asia, ranges have been narrow with little follow through on moves.

- Kiwi is ~0.2% firmer and is the best performer in the G-10 space at the margins. NZD/USD prints at $0.6065/70, the pair remains well within recent ranges. Bulls first look to break yesterday's high ($0.6095) and the 20-Day EMA ($0.6140).

- AUD/USD is also up ~0.2% and last prints at $0.6535/40. Tuesday's low in AUD/USD reinforces bearish conditions, support comes in at $0.6497, the Aug 8 low, and $0.6458, low from May 31 and bear trigger. Resistance comes in at $0.6610, the high from Aug 10.

- Yen is a touch softer, USD/JPY is marginally higher than opening levels. July PPI was softer than expected printing at 0.1% M/M vs 0.2% exp.

- Elsewhere in G-10, GBP is marginally lower and EUR is little changed from opening levels.

- Cross asset wise; US equity futures are firmer, a post-market rise in Disney has supported the space. The Hang Seng is down ~1%. BBDXY is flat, US Tsy Yields are a touch firmer across the curve.

- The July US CPI print headlines today's docket, the MNI preview is here.

EQUITIES: Most Regional Markets Tracking Lower, Japan Shares Outperforming

Outside of Japan, Asia Pac region stock markets are mostly weaker. China and HK markets track lower. US equity futures are higher though. Eminis were last around 4503, up from recent lows in the 4480/4490 region, which is still offering support. We are +0.40% firmer, but remain comfortably below Wednesday session highs around 4536. Nasdaq futures are +0.43% higher, but this unwinds less than half of Wednesday's cash index loss. Focus remains very much on the upcoming US CPI print.

- In Hong Kong the HSI is off by close to 1% at the break. The HSTECH index is off by 1.50%. Late US time on Wednesday, US President Biden signed an executive order around US investment limits in China technology. This may be weighing on sentiment, but has been well telegraphed and some commentators suggest it is not as limiting as feared.

- Mainland China shares have also tracked lower. The CSI 300 is down nearly 0.50% at the break. The real estate sub index is close to flat. Some support is coming from higher energy stocks, which is flowing from the oil bounce.

- Japan shares are bucking these trends, with the Topix +0.70% firmer, and Nikkie 225 at +0.60% higher at this point. Top contributors to the rise have been car makers Honda and Toyota.

- South Korean shares are seeing less outperformance compared to yesterday, with the Kospi off by ~0.40%. The Taiex is down 1.20% in Taiwan, in line with fresh weakness in the SOX index in recent sessions.

- Australian shares are a touch higher, while most markets are modestly lower in SEA. Indian shares are around -0.30% lower at this stage, with the RBI decision due shortly.

ASIA DATA: Regional Inflation Eases Further, Moderation Likely To Slow Going Forward

Numerous Asian economies have reported July inflation and the data to date show that inflation continued to moderate at the start of Q3. But certain global disinflationary forces such as food and fuel prices appear to have turned which is likely to make further declines tougher to achieve (see MNI Disinflationary Forces Easing).

- Excluding China non-Japan Asian inflation eased to 3.6% from 3.8%, the slowest pace since October 2021. This assumes though that July was equal to June for countries that have not yet released data and so it could be even lower when all countries have reported. Core is also moderating coming down to 3.2% from 3.4%, the lowest since May 2022, which should reassure the central banks across the region, most of which have paused tightening.

- China’s July CPI fell 0.3% y/y and so non-Japan Asian inflation moderated further to 1.5% y/y from 1.7%, the slowest since February 2021. But China has said that disinflation is expected to be temporary and so Asian inflation is probably close to a trough. China’s core CPI rose 0.8% y/y from 0.4%, thus underlying Asian inflation rose to 1.5% from 1.2%. See MNI Negative CPI Y/Y Momentum Expected To Be Temporary, PPI Deflation Moderates.

Source: MNI - Market News/Refinitiv

RBI: Policy Steady, But Hawkish Undertones

As widely expected by the sell-side, the RBI has held rates steady at 6.50%. The decision to hold rates was unanimous. While 5 out of 6 board members were in favor of maintaining the current stance - 'withdrawal of accommodation'. The outcome was largely expected, although the revision higher in the inflation forecast and moves to mop up excess liquidity were hawkish developments.

- Not surprisingly much of the focus was on the RBI's inflation outlook. Das stated the central bank has revised the FY 24 inflation forecast to 5.4% from 5.1%. This due to surging food prices, particularly in the vegetable space.

- Das stated vegetable prices can come down quickly in coming months, but is mindful of the impact on inflation expectations. The RBI can look through such shocks but if they persist the central bank will have to act. Das also noted other watch points for the RBI, - el nino and global food prices. He stated the central bank was resolute in bringing inflation back to the 4% target (it isn't enough just to bring it into the target band, 2-6%).

- The RBI kept the FY 24 growth projection unchanged at 6.5%. Das sounded upbeat on the domestic economy, although said weaker external conditions need to be watched.

- Das also announced a temporary measure to absorb excess liquidity in the banking system, generated by the return of 2000-rupee notes from earlier in the year. From August 12 banks will maintain an incremental cash reserve ration of 10% on the increase in their deposits seen in the May 19 to July 28 period (which is when the withdrawal of the 2000-ruppe notes started). This is in addition to the 4.5% cash reserve ratio that banks already have to maintain. Das stated excess liquidity can pose a threat to price stability, and that the incremental rule will be reviewed on September 8.

- Indian equities have retreated on this news. The Sensex off by 0.60%, with bank stocks under pressure. USD/INR is steady around 82.80/85. India's 10yr yield is a touch higher from session lows, last near 7.17%.

ASIA FX: CNH Steady, Other USD/Asia Pairs Mostly Firmer

USD/Asia pairs are mostly trading with a firm bias, albeit with USD/CNH slightly lower. THB and PHP have continued to trade with a softer bias. INR is relatively steady post the RBI's on hold outcome. Tomorrow, we get Singapore Q2 GDP revisions, South Korean money supply and Thailand consumer confidence. China aggregate credit figures and new loans data is also due between now and the 15th of August.

- USD/CNH has had a very quiet session compared to recent history. The pair has oscillated around 7.2200. The CNY fixing was again much stronger than expected. Weaker local equities have kept moves sub 7.2200 supported though.

- 1 month USD/KRW has continued to track recent ranges, albeit with a positive bias this afternoon (with some spill over from weaker yen levels likely weighing). The pair was last just above 1316.

- USD/INR hasn't moved a great deal after the as expected RBI on hold decision. There were hawkish undertones from the RBI, but this has impacted local equities more so than INR. USD/INR was last in the 82.80/85 region, little changed in the session to date.

- USD/THB is pushing above 35.00, the pair last in the 35.10/15 region, +0.60% firmer for the session. Next week the Constitutional Court is due to decide on whether to allow PM candidate renominations which should mean the next vote can go ahead soon after. It is still unclear whether Pheu Thai’s candidate Srettha will get enough support though. Political uncertainty has weighed on the baht since late July.

- USD/PHP is off earlier session highs, last near 56.30. Moves above 56.40 continue to draw selling interest. Earlier Q2 GDP was much weaker than expected, but the officials still believe the full year growth target can be reached.

- The Ringgit is little changed in dealing on Thursday. In yesterday's session the 20-Day EMA (4.5674) provided support to USD/MYR as broader USD trends dominated flows, the pair pared losses to finish ~0.1% lower than opening levels. We sit at 4.5720/50 in recent dealings.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing, remaining well within the recent range. The measure sits ~0.7% below the top of the band. USD/SGD is also little changed (1.3475/80), and is dealing in a tight range. The pair was unable to sustain a break of the 200-Day EMA ($1.3467) yesterday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/08/2023 | 0600/0800 | * |  | NO | CPI Norway |

| 10/08/2023 | 0600/0800 | ** |  | SE | Private Sector Production |

| 10/08/2023 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 10/08/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 10/08/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 10/08/2023 | 1230/0830 | *** | | US | CPI |

| 10/08/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 10/08/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 10/08/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 10/08/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 10/08/2023 | 1800/1400 | ** | | US | Treasury Budget |

| 10/08/2023 | 1900/1500 | | US | Atlanta Fed's Raphael Bostic | |

| 10/08/2023 | 1900/1500 | *** |  | MX | Mexico Interest Rate |

| 10/08/2023 | 2015/1615 | | US | Philadelphia Fed's Pat Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.