Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- JGB futures remain weaker but off session cheaps, -20 compared to settlement levels, after the BOJ conducted an unscheduled bond purchase to buy Y300bn of 5-to-10-year and Y100bn of 3-5bn notes at market yields. US Tsys have observed narrow ranges for the most part in Asia today, moves have had little follow as the proximity to this evening's FOMC rate decision comes into focus.

- NZ labour market data was either below or close to expectations. Q3 employment contracted 0.2% q/q after rising 1%, the first drop since Q2 2022. NZD/USD fell below 0.5800 but is up off lows. Yen has outperformed as verbal rhetoric on FX weakness stepped up.

- Elsewhere, manufacturing PMIs across Asia have fallen in October with most now in contractionary territory, see below for details.

- The aforementioned FOMC rate decision headlines today's docket, the MNI preview is here. We also have US construction spending, ISM Manufacturing, job openings and light vehicle sales.

MARKETS

US TSYS: Narrow Ranges In Asia, FOMC In View

TYZ3 deals at 105-30, -0-07+, a 0-04 range has been observed on volume of ~80k.

- Cash tsys sit 1-2bps richer across the major benchmarks, light bull flattening is apparent.

- Tsys have observed narrow ranges for the most part in Asia today, moves have had little follow as the proximity to this evening's FOMC rate decision is perhaps keeping participants on the sidelines.

- The space looked through a weaker than forecast Chinese Caixin Mfg PMI print. The USD was marginally firmer in Asia and e-minis were a touch lower.

- FOMC dated OIS price no change in today's meeting, a terminal rate of ~5.45% is seen in January with ~55bps of cuts by Sep 24.

- The aforementioned FOMC rate decision headlines today's docket, the MNI preview is here. We also have US construction spending, ISM Manufacturing, job openings and light vehicle sales.

JGBS: Futures Off Session Lows After BOJ Unscheduled Bond Purchase

In Tokyo afternoon dealings, JGB futures remain weaker but off session cheaps, -20 compared to settlement levels, after the BOJ conducts an unscheduled bond purchase to buy Y300bn of 5-to-10-year and Y100bn of 3-5bn notes at market yields.

- There hasn’t been much in the way of domestic data drivers to flag today, outside of the previously outlined Jibun Bank Japan PMI Mfg data.

- Bloomberg reports that BofA believes the BOJ’s next step will probably be the removal of negative interest-rate policy and yield-curve control. BofA’s base case scenario is for the central bank to move at its January meeting. A change may come by April at the latest, they said. (See link)

- Cash JGBs are cheaper across benchmarks, with yields 0.5bp (1-year) to 3.3bps higher (30-year). The benchmark 10-year yield is 1.8bp higher at 0.966% versus the cycle high of 0.974% (set earlier today) and the BOJ’s YCC reference level of 1.0%.

- Swap rates are 2-4bp higher across the curve, with swap spreads wider, apart from the 30-40-year zone.

- Tomorrow, the local calendar sees Monetary Base and International Investment Flow data, along with 10-year supply.

AUSSIE BONDS: Cheaper But Well Off Lows After Building Apps Miss & NZGB Rally, FOMC Decision Due

ACGBs (YM -3.0 & XM -3.0) remain cheaper but are well above the Sydney session’s worst levels. This push away from session cheaps can be attributed to weaker-than-expected building approvals data and spillover from NZGB’s post-employment data rally. NZ Q3 employment contracted 0.2% q/q after rising 1%, the first drop since Q2'22. Nevertheless, wages looked stubborn, with Q3 labour costs rising 1.1% q/q and 4.3% y/y.

- The intraday rally in ACGBs was also assisted by US tsy dealings in the Asia-Pac session. Cash US tsys are 1-3bp richer, ahead of the FOMC decision later today.

- The cash ACGB 10-year yield is 4.96%, 3bps higher on the day, after earlier touching 5.0% for the first time since 2011.

- Swap rates are 1-2bps higher.

- The bills strip is flat to -2.

- RBA-dated OIS pricing is 2bps firmer (Feb’24) to 1bp softer (Jun’24) across meetings, with terminal rate expectations at 4.54% (+47bps by Jun’24). The expected terminal rate hit 4.58% earlier in the session.

- Tomorrow, the local calendar will see Trade Balance and Home Loan data.

- AFR reports that the IMF, in a staff report, said Australia needs to tighten monetary policy further as part of stepped-up efforts to rein in inflation that include governments slowing the pace of public investment. (See link)

RBA: IMF Sees Inflation Moderation Too Slow, Says RBA Needs To Hike More

The IMF has released its conclusions from its 2023 Article IV Mission on Australia. It recommends further rate hikes to reduce sticky core inflation and reforms to boost productivity growth, which the RBA has noted for some time is too low. The market has over a 70% chance of a 25bp move at the November 7 meeting priced in.

- The IMF is forecasting 2024 growth of 1.25%, resulting in the closure of the output gap, down from 1.8% this year. 2024 is lower than the RBA’s August projections but 2023 higher. The main risks stem from “high and persistent inflation”, climate change and the uncertain global outlook, especially China.

- Inflation is expected to average 4% next year, well above the RBA’s current forecast of around 3.5%. An upward revision of that magnitude would delay the return to target which would require further tightening.

- The IMF observes that the moderation in Australian inflation is slow and that core is sticky and so “more is needed to bring inflation back to target”. In other words, the RBA needs to increase rates more to contain inflation and inflation expectations. The Australian policy rate remains below many other OECD countries.

- Australia needs to implement productivity boosting reforms including in the areas of the digital economy, labour market, tax, innovation and competition. It also suggests supporting green energy.

- See full report here.

NZGBS: Closed At Session Bests After Softer Labour Market Data

NZGBs closed on a strong note, with yields 5-7bps lower, after labour market data printed either below or close to expectations. Q3 employment contracted 0.2% q/q after rising 1%, the first drop since Q2'22. However, wages look stubborn, with Q3 labour costs rising 1.1% q/q and 4.3% y/y. Private wages saw growth slowing but the public sector boosted overall wage costs. Accordingly, it looks difficult for the RBNZ to meet its early 2024 forecast of 3.8% y/y. Revised projections are due at the November 29 meeting.

- Swap rates closed 8-10bps lower, with the 2s10s curve steeper. Implied swap spreads closed 3-4bps tighter.

- RBNZ dated OIS pricing closed 1-7bps softer across meetings, with late’24 leading. Terminal OCR expectations drop to 5.58% (+8bp by Feb’24).

- RBNZ released its Financial Stability Report stating that “the vast majority of [household] borrowers have been able to manage these [interest rate] increases”. Businesses continue to service debt, although the dairy and commercial property sectors are facing challenges.

- RBNZ Deputy Governor Christian Hawkesby said no decisions have been made on implementing debt-to-income restrictions.

- The local data docket is empty tomorrow.

- Tomorrow, the NZ Treasury plans to sell NZ$225mn of the May-30 bond, NZ$175mn of the May-34 bond and NZ$100mn of the May-51 bond.

NZ DATA: Orderly Easing Of The Labour Market In Line With RBNZ Outlook

NZ labour market data was either below or close to expectations. Q3 employment contracted 0.2% q/q after rising 1%, the first drop since Q2 2022. The unemployment rate rose 0.3pp to 3.9% in line with consensus but the highest since Q2 2021. It was slightly higher than the RBNZ’s projected 3.8% but still consistent with Q4’s 4.4% forecast. Private wage growth came in below the 1% q/q forecast.

NZ unemployment rate %

Source: MNI - Market News/Refinitiv

- Employment growth was 2.4% y/y in Q3 on track to meet the RBNZ’s 1.1% projection for Q1 2024. Hours worked rose 0.1% q/q to be up 2.3% y/y down from 3.4% and the underutilisation rate rose 0.5pp to 10.4%, indicating growing labour market capacity especially amongst the under 25s (underutilisation rate 27%).

- The weakness in job growth was in full-time employment which fell 0.4% q/q whereas part-time grew 0.2%. This is a signal of more cautionary hiring.

Source: MNI - Market News/Refinitiv

- The increase in the supply of labour has helped to alleviate labour shortages although the participation rate fell 0.4pp to 72% in Q3 but working age population rose 0.6% q/q to be up 2.6% y/y, fastest pace since Q1 2017. With job growth positive until Q3, this has driven a strong increase in the number of unemployed which rose 7.3% q/q and 24.2% y/y in Q3 but the level remains historically low.

FOREX: Kiwi Pressured, Yen Firmer In Asia

The NZD has been pressured in Asia today, early pressure came after the Q3 employment report and Kiwi has been see-sawing around $0.58 for the majority of today's session. The Yen is the best performer in the G-10 space, trimming Tuesdays post BoJ losses as Japanese authorities hint at possible currency intervention.

- NZD/USD is down ~0.3%, last printing at $0.5805/10. Q3 employment contracted 0.2% q/q after rising 1%, the first drop since Q2'22. However Q3 labour costs rose 1.1% q/q and 4.3% y/y.

- The Yen is up ~0.3% however at this stage the ¥151 handle remains intact. Japan's top currency official Kanda noted today that authorities are ready to act on the Yen if needed.

- AUD is a touch below opening levels, however ranges have been narrow with little follow through on moves. Technically the trend outlook is bearish, support comes in at $0.6270 low from Oct 26 and key support. Resistance comes in at $0.6406, 50-Day EMA.

- Cross asset wise; US Equity futures are off session lows however e-minis remain ~0.2% lower. US Tsy Yields are 1-2bps lower across the curve. BBDXY is up ~0.1%.

- The highlight of today's session is the latest FOMC rate decision.

EQUITIES: Japan Outperforms, Weaker Data Weighs On China/HK

Japan markets are the clear outperformers in Asia Pac trade so far in Wednesday trade. Mixed trends are evident elsewhere. US futures are down but away from session lows. Eminis were last near 4206, off close to 0.15%. Earlier dips sub 4200 were supported. Nasdaq futures are also weaker (last -0.10%), but likewise away from earlier lows.

- Some late earnings disappointment from the NY session on Tuesday has weighed on US futures, but overall ranges have been tight. Proximity to the upcoming Fed meeting later may be leaving participants in wait and see mode.

- Japan's Topix is up around 2% at this stage, putting the index back above 2300 (levels last seen in the first half of October). The electrical appliances sector and transportation have been the strongest contributors to the rise.

- A weaker yen/dovish BoJ backdrop will be aiding sentiment for some these sectors. The yen is slightly stronger today though as the authorities raised their verbal rhetoric around FX weakness.

- Hong Kong and China markets sit close to flat at the break. This is away from session lows, which came after a weaker than expected Caixin manufacturing PMI print (49.5). The CSI 300 is near 3574.

- South Korea's Kospi is nearly 1% higher, while the Taiex is +0.30% firmer.

- In SEA, Indonesian markets continued their recent volatility, the JCI off 1% so far today. Thailand stocks are also weaker, down 0.40%.

OIL: Crude Range Trading Ahead Of Fed

Oil prices are marginally higher in the APAC session after falling on Tuesday. They have been range trading ahead of the Fed decision later today. The USD index is slightly higher.

- Brent is 0.3% higher at $85.25/bbl. It reached a high of $85.58 before the Caixin China PMI but was already declining before the data was published. It fell to a low of $85.14 after the release. WTI is up 0.2% to $81.14/bbl after an intraday low of $81.03. With China’s PMI below 50, there is limited upside to crude as it is the largest importer.

- The attention of the oil market has returned to demand, particularly with the Fed and payrolls this week, as the situation in Israel/Gaza seems to be contained for now. US Secretary of State Blinken will return to the region including Israel to continue his efforts to ensure the conflict doesn’t spread.

- BP has said that gasoline and diesel is currently oversupplied, according to Bloomberg.

- Bloomberg reported that US crude inventories rose 1.35mn barrels in the latest week according to people familiar with the API data. The official EIA data is out later.

- Markets are looking to today’s Fed meeting and press conference (see MNI Fed Preview). Also October US ADP employment and manufacturing ISM print.

GOLD: Second Consecutive Day Of Decline Unwinds Friday’s Gaza-Invasion-Induced-Surge

Gold has weakened further (-0.3%) in the Asia-Pac session, after closing 0.6% lower at $1983.88 on Tuesday. Price action this week has effectively unwound Friday’s surge sparked by news of Israel’s ground invasion of Gaza. Bullion hit $2000 for the first time since May on Friday.

- Higher US Treasury yields on Tuesday, following a slightly higher-than-expected employment cost index, weighed on the precious metal. Higher rates are typically negative for non-yielding bullion.

- Attention now turns to the FOMC’s policy meeting decision later today.

- According to MNI’s technicals team, the outlook still suggests the yellow metal could head northbound with resistance at $2009.4 (Oct 27 high) but support is seen at $1943.2 (20-day EMA) should some geopolitical de-escalation be seen.

ASIA DATA: Lower Orders Weighing On Asian Manufacturing

Manufacturing PMIs across Asia have fallen in October with most now in contractionary territory. Indonesia is the highlight with the S&P Global PMI still above the breakeven-50 mark even though it fell. Singapore and the Philippines were above 50 in September but their October data is not out until November 3 with the ASEAN aggregate.

- Indonesia’s S&P Global manufacturing PMI eased to 51.5 from 52.3 signalling a slowdown in industrial activity growth. The moderation is due to slower orders growth particularly from overseas. Exports contracted slightly in October. As a result business confidence is at its least optimistic since February and employment was cut marginally.

- Costs for Indonesia’s manufacturers continued to rise from transport, raw materials and financing and at the fastest pace since March. Due to weaker demand though they were only partially passed on to selling prices, so inflation fell from September.

- The S&P Global manufacturing PMI for Thailand deteriorated to 47.5 from 47.8 after being as high as 60.4 only 6-months ago. The drop was due to shrinking new orders including from overseas. But production growth was positive as businesses worked through order backlogs. But with orders down for the fourth straight month employment and purchasing activity were reduced. Business confidence was lower but still optimistic.

- Thai input costs eased again due to substituting towards cheaper but slower transport options. Selling price inflation rose in October but remains below average.

- Malaysia’s PMI was steady in October at 46.8 suggesting that manufacturing activity continued to shrink at the start of Q4. New orders and thus output are weighing on activity in the sector.

- See reports here.

Source: MNI - Market News/Bloomberg

BNM: MNI BNM Preview - Nov 2023: Unlikely To Join The South East Asia Tightening Trend

- We don't expect BNM to join other central banks in SEA (Indonesia, Philippines etc) and resume its tightening cycle. Malaysian inflation pressures are much lower compared to elsewhere in the region.

- MYR FX weakness is a source of domestic concern, but a 25bps hike won't do much to close the yield gap with the US.

- Economic growth is comfortably off 2022 highs and partial indicators continue to suggest the manufacturing/export side remained under pressure through the tail end of Q3/early Q4. All in all, the growth backdrop points to caution around tightening policy further.

- See our full preview here:

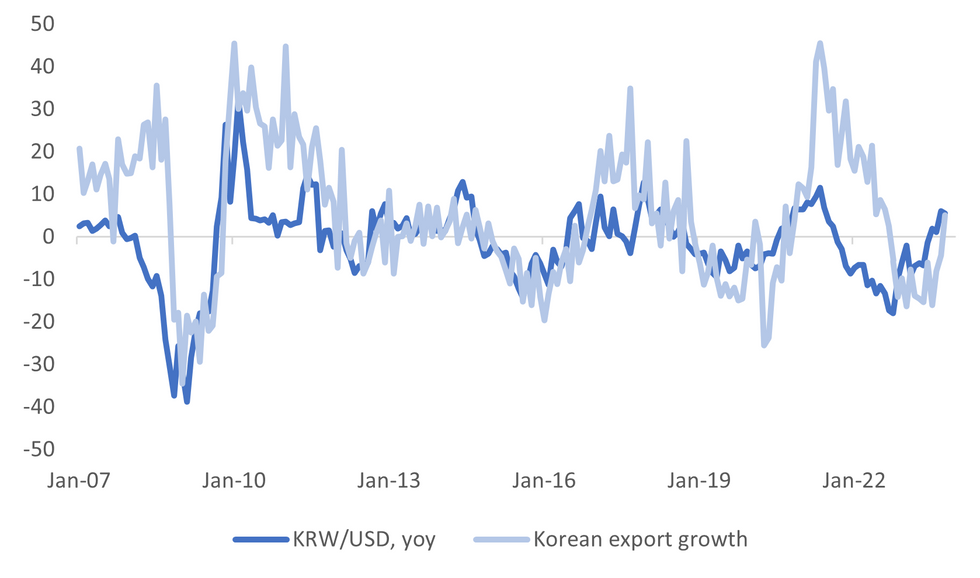

SOUTH KOREA: Exports Rise In Line With Forecasts, Import Weakness Sees Trade Surplus Maintained

South Korean October trade figures saw exports print close to expectations, up 5.1% y/y (versus 6.1% forecast and -4.4% prior). Imports were weaker than expected at -9.7% y/y (-2.1% forecast and -16.5% prior). This saw the trade position remain in surplus, +$1636mn, versus a projected deficit of -$1700mn (the prior surplus was $3697mn).

- This paints an improving export backdrop, although base effects are less favorably in Nov and in coming months. From a KRW standpoint, we are also roughly in line with the y/y export trend, see the first chart below.

- In terms of the detail, auto exports remained a source of strength, up 19.8% y/y. Machinery exports were also strong, while the drag from chip exports (-3.1%) lessened.

- China exports were down -9.5% y/y, which is also on an improving y/y trend. Exports to the US remained up strongly in y/y terms. By share US exports have also almost surpassed those to China.

Fig 1: KRW/USD Y/Y Versus South Korea Export Growth Y/Y

Source: MNI - Market News/Bloomberg

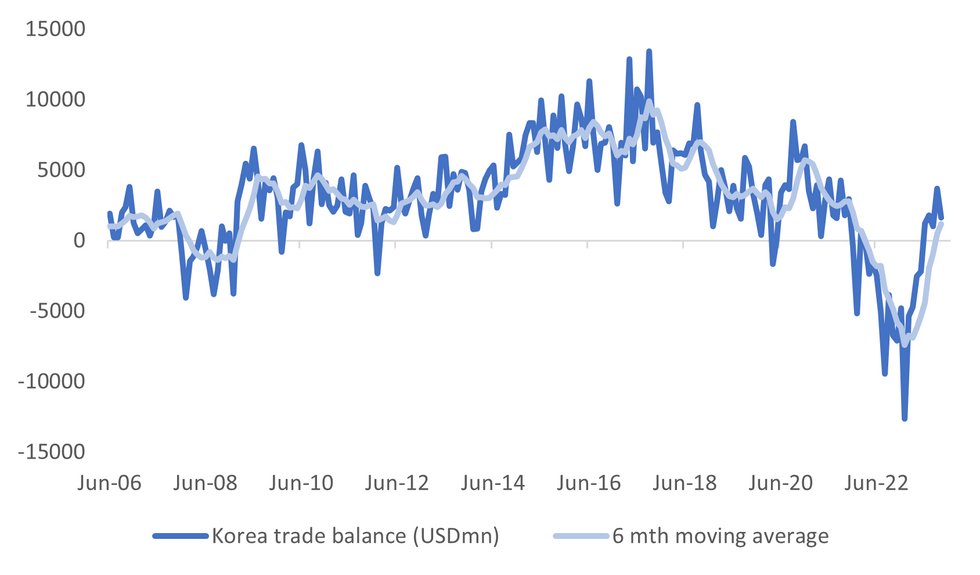

- The larger import drop aided the trade position, although today's surprise hasn't aided won sentiment (last near 1354 for the 1 month NDF, -0.25% weaker in won terms).

- The trade position is comfortably past the 2022 trough (see the chart below), although further significant improvement may be more difficult given terms of trade proxies have stabilized.

Fig 2: South Korea Trade Position Surprises On The Upside In October

Source: MNI - Market News/Bloomberg

INDONESIA DATA: Inflation Contained, BI Focus On IDR

Indonesia’s CPI inflation for October was close to the Bloomberg consensus. Inflation remains moderate and within Bank Indonesia’s target band for 2023 and 2024 but that may not be enough to prevent a further rate hike to attract portfolio flows and contain imported inflation. Today USDIDR has jumped to 15950 as the market waits for the upcoming Fed decision. This is close to the October high, which will not be welcomed by BI. The next meeting is November 23.

- Headline printed in line with consensus at 2.6% y/y up from 2.3% due to higher food and transport inflation. Core inflation was slightly lower than expected at 1.9% down from 2% in September, the lowest since January 2022. It is now slightly below the bottom of this year’s 2-4% target band but it shifts down to 1.5-3.5% for 2024.

- Food, drink & tobacco saw a pickup in October to 5.4% y/y from 4.2%. Transportation rose 1.2% y/y up from 1% but utilities edged lower to 1.2% from 1.3%. Most other components were steady or down slightly.

Source: MNI - Market News/Refinitiv

ASIA FX: USD/Asia Pairs Higher, THB Slumps, CNH Still Sidelined

USD/Asia pairs are pretty much higher across the board, although once again CNH is steady near 7.3400, largely ignoring broader USD trends. The weaker Caixin PMI did weigh on sentiment elsewhere though. Baht has been the weakest performer, down over 1%, unwinding some of its October outperformance. Tomorrow, we have South Korean CPI, along with the BNM decision in Malaysia (no change is expected), as the main watch points.

- USD/CNH has tracked recent ranges, last just under 7.3380. Equity sentiment struggled post the Caixin PMI miss, although we are away from lows. USD/CNY spot remains under 7.3200, in line with the CNY fixing cap. US authorities stated a Biden-Xi meeting would take place in November, although the China authorities stated that they had nothing to add to these reports (BBG).

- 1 month USD/KRW is higher for the session, last near 1356, around 0.40% weaker in won terms. A better equity backdrop, coupled with a surprise trade surplus has done little to lift sentiment for the won. The weaker China data has weighed, while higher beta FX has also generally been on the backfoot in terms of the majors.

- USD/HKD sits just near 7.8245, well within recent ranges. The pair hasn't spent much time above 7.8250 since mid-October though (with the 50-day EMA at 7.8255). The 200-day remains near 7.8290. On the downside, late October dips below 7.8200 were supported. This fits with a broadly stable US-HK short end yield differential backdrop over this period (see the chart below). The 3 month differential sits at +23bps as we head into the Fed meeting later. 1 month Hibor has drifted a touch lower, last fixed at 4.875%. The 3 month is steadier though, near 5.23% today.

- USD/THB sits back in 36.30/35 region, +1.0% higher for the session so far. We closed yesterday at 35.94, but recent dips sub the 36.00 level haven't been sustained in the pair. These levels also come close to the 50-day EMA support point at 36.01. Broader USD gains, particularly against the yen, post yesterday's onshore spot close has seen the baht play catch up to the downside in the first part of trade today. Earlier the Oct manufacturing PMI ticked down to 47.5 from 47.8.

- Like elsewhere in the region, USD/IDR has rebounded today. The pair last at 15950, just under recent reported intervention levels above 15960. In the past week the pair has largely drifted sideways, but dips have been supported as we head into the US FOMC meeting later. Oct CPI has just printed with headline close to expectations (2.56% y/y and m/m at 0.17%, core at 1.91%y/y). Pressures are just up off recent lows. Offshore developments, particularly in terms of the Fed and pressure on IDR, will likely have a greater say on any follow up BI tightening actions though. Earlier we had the Oct PMI print at 51.5, from 52.3 prior.

- The SGD NEER (per Goldman Sachs estimates) is marginally firmer in early trade this morning and sits a touch off the touch of recent ranges. The measure sits ~0.4% below the top of the band. USD/SGD has firmed back above the 20-Day EMA ($1.3685), the pair has see-sawed around the measure for the majority of recent trading as a $1.3650/1.3750 range persists. A reminder that the local docket is empty today. Tomorrow we have the Purchasing Managers Index and Electronic Sector Index, on Friday October S&P Global PMI and September Retail Sales cross.

- The Ringgit has been pressured in early dealing on Wednesday as onshore participants digest yesterday's session which saw US Tsy Yields tick higher, which has partially unwound in Asia, and the USD also firm. We sit at 4.7740/65 ~0.2% above yesterday's closing levels and well within the recent range. October S&P Global Mfg PMI crossed this morning, the measure held steady at 46.8. The Output and New Orders components fell to their lowest levels since Jan 23.

- The Rupee has opened dealing little changed from yesterday's closing levels in a muted start to Wednesday's session. USD/INR prints at 82.25/26, the pair continues to consolidate in a narrow range above the 20-Day EMA (83.2120). RBI Gov Das noted yesterday at a banking conference in Mumbai taht he expects Q2 GDP to surprise to the upside (BBG).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/11/2023 | 0930/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/11/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 01/11/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 01/11/2023 | - | *** | | US | Domestic-Made Vehicle Sales |

| 01/11/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 01/11/2023 | 1230/0830 | ** | | US | Treasury Quarterly Refunding |

| 01/11/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/11/2023 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/11/2023 | 1400/1000 | * | | US | Construction Spending |

| 01/11/2023 | 1400/1000 | *** | | US | JOLTS jobs opening level |

| 01/11/2023 | 1400/1000 | *** | | US | JOLTS quits Rate |

| 01/11/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 01/11/2023 | 1800/1400 | *** | | US | FOMC Statement |

| 01/11/2023 | 2015/1615 |  | CA | BOC Governor testifies at Senate hearing |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.