Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

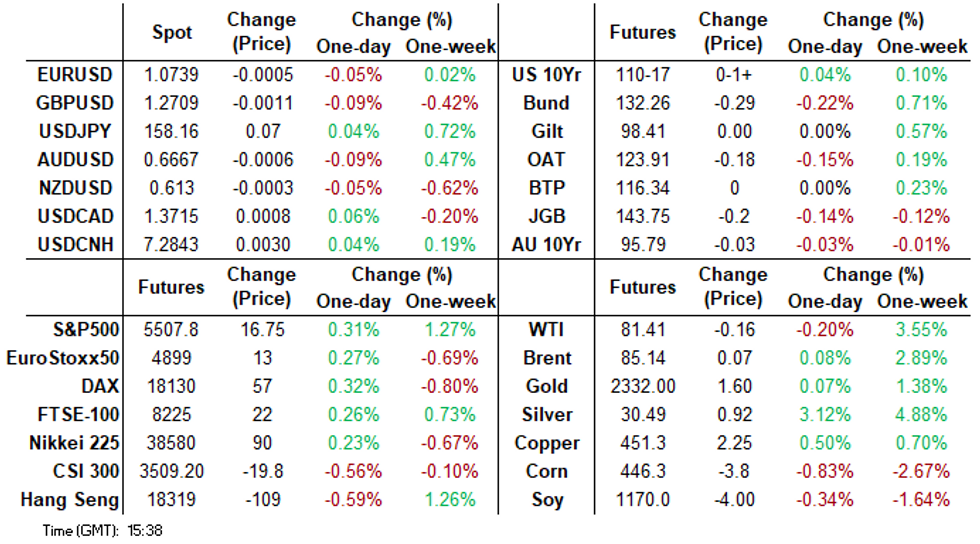

- Global rates are cheaper today, with US cash trading returning from the Juneteenth holiday, NZGBs were the worst performing following stronger than expected GDP numbers

- New Zealand Q1 GDP came in above expectations rising 0.2% q/q to be up 0.3% y/y after falling 0.1% q/q and 0.2% y/y.

- Equities markets were lower today with very little in the way of headlines or eco data to drive prices, investors are awaiting BoE and the US to return

- Bank Indonesia meets today and while it is expected to keep rates at 6.25%, there is a material risk of a hike given that USDIDR is rising again

MARKETS

US TSYS: Tsys Futures Edge Lower Ahead Of US Jobless Claims

- Treasury futures have edged lower throughout the day and now trade at session's worst as cash trading returned from a break. TUU4 is -0-02⅜ at 102-05¾, while TYU4 is -0-08+ at 110-17.

- We have broken below Wednesday lows across the curve, although TYU4 still holds well above initial support at 109-22+ (50-day EMA).

- Cash treasuries are cheaper across the curve today with slightly better selling through the belly, yields are +2-3bps. The 2Y is +2.3bps at 4.735%, 5Y +3bps at 4.273% while the +2.7bps at 4.25%, the 2y10y is a touch higher than Tuesday's & the YTD lows +0.801 at -48.768 vs -49.936 lows.

- APAC markets: NZ GDP came in above estimates at 0.2% vs 0.1%, we had some weak bond auction results earlier with NZGBs closing 4.5-6bps cheaper across the curve, ACGBs are 2-3bps cheaper, curve has steepened. While Japan had a solid 5y auction, the curve has bull-flatten with yields +/- 2bps

- The Fed's Neel Kashkari and Thomas Barkin will speak later today

- Looking ahead, Weekly Claims, House Starts & Build Permits while the Bank of England makes their policy announcement.

NZGBS: Closed On A Weak Note, Yields Pressured By GDP, Supply & US Tsys

NZGBs closed near session cheaps, with benchmark yields 5bps higher. Domestic and offshore factors were at play.

- On the home front, the NZ economy exited its technical recession, with Q1 GDP printing +0.2% q/q (+0.3% y/y) versus consensus expectations of +0.1% (+0.2%).

- The RBNZ forecast +0.2% q/q in its May Monetary Policy Statement. Accordingly, the result is unlikely to change the MPC’s wait-and-see stance.

- NZGBs extend losses after lacklustre weekly bond auctions. May-31 supply saw a cover ratio of 1.24x, down from 2.46x at the prior outing. The ratio for the May-34 bond fell to 1.85x from 2.60x prior.

- Cheaper cash US tsys, yields 2-3bps higher, in today’s Asia-Pac session after yesterday’s holiday was also a drag on the local market.

- Swap rates closed 4-6bps higher.

- RBNZ dated OIS pricing closed 3bps firmer for 2025 meetings. A cumulative 30bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

- Today, the US calendar will see Weekly Claims, House Starts and Building Permits. The Bank of England will also make their policy announcement, with an on-hold decision likely.

ACGBS: At Session Cheaps, AU-US 10Y Diff Almost Flat, Jun-31 Supply Tomorrow

ACGBs (YM -3.0 & XM -3.5) are cheaper and at Sydney session lows. With the domestic calendar light, the local market has taken its cue from cash US tsys, which are 2-3bps cheaper in today’s Asia-Pac session after yesterday’s holiday.

- That said, ACGB market weakness is also likely to reflect an ongoing adjustment by local participants to the RBA’s hawkish hold on Tuesday.

- Cash ACGBs are 3bps cheaper, with the AU-US 10-year yield differential at -4bps, its highest level since February.

- Swap rates are 2bps higher.

- The bills strip is slightly cheaper, with pricing flat to -2.

- RBA-dated OIS pricing is 7-12bps firmer for meetings beyond August versus pre-RBA levels. A cumulative 8bps of easing is priced by year-end from an expected terminal rate of 4.37%.

- Tomorrow, the local calendar will see Preliminary Judo bank PMIs alongside the AOFM’s planned sale of A$700mn of the 1.5% Jun-31 bond.

- Today, the US calendar will see Weekly Claims, House Starts and Building Permits. The Bank of England will also make their policy announcement, with an on-hold decision likely.

JGBS: Futures Near Cheaps, Cash US Tsys Weigh, National CPI Tomorrow

JGB futures are weaker, -17 compared to settlement levels, but above cheaps seen early in the Tokyo afternoon session.

- Outside of the previously outlined international investment flow data, there hasn't been much in the way of domestic data drivers to flag.

- Today's supply of 5-year bonds showed solid results, with the auction's low price meeting dealer expectations, the cover ratio rising and the auction tail shortening.

- Any positive impetus from today's supply, however, was countered by cash US tsys, which are 2-3bps cheaper in today’s Asia-Pac session.

- Today, the US calendar will see Weekly Claims, House Starts and Building Permits. The Bank of England will also make their policy announcement, with an on-hold decision likely.

- The cash JGB curve has twist-flattened, pivoting at the 40s, with yield movements bounded by +/- 2bps. The benchmark 10-year yield is 1.7bp higher at 0.949% versus the cycle high of 1.101%. The 5-year yield is 0.7bp higher at 0.517% after today’s supply.

- Swap rates are flat to 2bps higher out to the 30-year and 6bps higher beyond. Swap spreads are tighter out to the 10-year zone and wider beyond.

- Tomorrow, the local calendar will see National CPI and Jibun Bank PMIs (Preliminary).

ASIA RATES: Slightly Mixed After China’s LPR Is Left Unchanged

Asian Government Bonds are slightly mixed in today’s session.

- China’s government bond curve is displaying a modest twist-flattening, with yield movements bounded by +/- 1bp, after the Loan Prime Rate, based on the People’s Bank of China’s medium-term lending facility (MLF) rate, remained at 3.45% for the one-year maturity and 3.95% for over-five-year tenor on Thursday.

- (MNI) China's LPR will likely fall in the coming months as lenders’ funding costs decline due to lower deposit interest rates and as regulators crack down on extra interest payments to depositors, while the central bank looks to downgrade the role of its medium-term lending facility. (See link)

- South Korean sovereign bonds are generally cheaper across benchmarks following a strong performance in June. While the 10-year yield is 2bps higher today, it remains approximately 30bps lower since late May.

- A committee of South Korea’s ruling party will meet with BoK and Financial Services Commission officials on June 27 to discuss interest rate issues, including potential rate cuts and reducing the interest rate burden for citizens.

- Some ruling party officials are advocating for a rate cut, but BoK Governor Rhee Chang-yong has emphasised the independence of the monetary policy board's decisions.

STIR: RBA Dated OIS’ Post-RBA Firming Continues

RBA-dated OIS pricing is 7-12bps firmer for meetings beyond August relative to pre-RBA levels.

- Going into Tuesday’s meeting, the market was pricing approximately 15bps of easing by year-end from an anticipated terminal rate of 4.33%.

- As it currently stands, the market attaches a 23% chance of a 25bp hike in August, with an expected terminal rate of 4.38%.

- The expected official rate at year-end is 4.32% versus 4.21% ahead of Tuesday’s meeting.

- For context, the market was pricing no easing by year-end from an anticipated terminal rate of 4.42% in the run-up to the RBA’s May Policy meeting.

Figure 1: RBA-Dated OIS – Pre-RBA Vs. Post-RBA

Source: Bloomberg / MNI - Market News

GOLD: Subdued Session With US On Holiday

Gold is 0.3% higher in the Asia-Pac session, after closing little changed at $2328.16 on Wednesday. Yesterday’s session was relatively quiet with the US market closed for the Juneteenth holiday.

- European bond markets traded modestly higher in yield, with 10-year bund 1bp higher.

- The 10-year gilt yield increased 2bps to 4.06% despite UK headline and core inflation printing in line with consensus expectations at +2.0% y/y and +3.5% y/y respectively. The BoE will also make their policy announcement later today, with an on-hold decision likely.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- From a technical perspective, gold has pierced the 50-day EMA, at $2,315.9, signalling scope for a deeper correction to $2,277.4, the May 3 low. Initial firm resistance remains at $2,387.8, the Jun 7 high.

LNG: European Gas Prices Higher, Senate Recommends France Stop Russian LNG Imports

European LNG rose 1.9% on Wednesday to EUR 35.35 after a high of EUR 35.63 to be up 3.3% in June. Prices rose sharply following France’s senate committee recommending that imports of Russian LNG be halted “as soon as possible”. This is significant as Russia is France’s second largest supplier. Europe continues to look for ways to reduce its use of Russian LNG after it stopped pipeline flows following the invasion of Ukraine.

- The European Union would like to ban all imports of Russian LNG but is yet to find a consensus on increasing sanctions on gas. Reliance on its LNG has increased with shipments from Qatar dropping as vessels have avoided the Suez canal due to attacks by Houthi militants in the Red Sea. This means that routes are lengthened and costs increased as ships go via southern Africa.

- US natural gas rose 0.5% to $2.92 and is 13% higher this month. It has continued to climb in today’s trading. Prices have risen on the back of warmer weather predictions and a tropical storm off the coast of Texas.

- North Asian prices are 3.6% higher in June. Gas consumption in the region has increased due to cooling demand and forecasts that hot weather will continue in July signal that high usage will continue.

ASIA STOCKS: Asian Tech Stocks Continue To See Inflow

- South Korean equities were higher on Wednesday (Kospi up 1.21%, Kosdaq up 0.26%). Flows were slightly below the recent run rate, at just $273m on Wednesday, the past 5 sessions have netted a total inflow of $2.3b. The Kospi hit new cycle highs on Wednesday and now trades back above 2,800. The 5-day average is $460m, above both the 20 day average of $77m and the longer-term 100-day average at $152m.

- Taiwan equities were higher on Wednesday with another strong inflow of $1.39b, the largest inflow since 16th May. The Taiex continues to make new all time highs and is now up 4.74% for the week, with the majority of gains coming from TSMC. The past 5 session's have seen a total inflow of $3.9b with the 5-day average now $786m, above both the 20-day average at $93m, while the 100-day average is $60m.

- Thailand equities were slightly higher again on Wednesday, however the two consecutive days of inflows has not stemmed the flow of outflows with foreign investors now marking 20 straight sessions of selling for a total of $1.07b, with $268m of that coming in the past 5 sessions. The 5-day average is now -$54m, below both the 20-day average at -$53.5m and the 100-day average at -$24m.

- Philippines equities were little changed on Wednesday and holds near ytd lows. Foreign investors have been better sellers of equities recently, the past 5 sessions have seen a net outflow of $34m. The 5-day average is now -$6.75m, slightly above the 20-day average at -$10.5m, but inline with the long term average at -$5.60

- Indonesian equities were slightly lower on Wednesday and make new ytd lows with the JCI tapping 6,700. Foreign investors have been better sellers of stocks recently apart from a decent inflow on the 13th, otherwise it has been 17 of the past 18 days of selling. the past 5 sessions have seen an inflow of $31

- m. The 5-day average is now $6.18m, 20-day average is -$23m, while the 100-day average is -$5m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 273 | 2304 | 16638 |

| Taiwan (USDmn) | 1390 | 3930 | 5990 |

| India (USDmn)** | 189 | 996 | -2810 |

| Indonesia (USDmn) | -43 | 31 | -467 |

| Thailand (USDmn) | -73 | -269 | -2896 |

| Malaysia (USDmn) ** | -17 | 24 | -20 |

| Philippines (USDmn) | -10 | -33.8 | -495 |

| Total | 1709 | 6982 | 15940 |

| ** Up to 18th June |

ASIA STOCKS: Asian Equities Mixed On Little Catalyst, BoE Shortly

Asian markets are mostly mixed today as investors sought new catalysts after a US holiday. The MSCI Asia Pacific Index slipped 0.4% following a 1.7% jump the past two sessions. Japanese stocks moved lower, led by losses in cyclical value shares such as brokerages, real estate companies, and automakers. In South Korea equities are higher driven by gains in tech stocks like Samsung Electronics. New Zealand released Q1 GDP which beat estimates, equities have reacted positively to it, while Australian equities are little changed this morning. In the EM space, most markets continue to see foreign investors sell stocks, while markets hit ytd lows.

- Japanese equities opened lower on Thursday as European markets drifted downwards overnight, while Wall Street remained closed. We currently trade just off session lows with the Nikkei 225 index down 0.38%, and the broader Topix index lost 0.62%. Market sentiment was cautious with no significant news driving activity, leading investors to hold back on purchases. Tourism-related sectors showed resilience amid ongoing international visitor arrivals to Japan. Major automakers and chip-related stocks faced selling pressure, while Japan Airlines and ANA Holdings saw modest gains.

- South Korean equities are mixed today with the KOSPI up 0.51%, while the KOSDAQ is down 0.43% The market was buoyed by tech stocks, with Samsung Electronics Co. rising 0.5% and SK hynix climbed 1.1%. Positive sentiment was driven by tech gains amid concerns over a potential delay in US interest rate cuts.

- Taiwan equities have opened slightly higher this morning, TSMC was up over 4% on Wednesday which has been the contributor to the Taiex gains recently, while foreign investors have also been better buyers of local stocks recently with a 3.6b inflows over the past 5 sessions. The Taiex is up 0.30%

- Australia equities are a touch lower today, with gains in industrial and energy shares were offset by losses in the financial sector. Mexican fast-food chain Guzman Y Gomez listed on the ASX and was up about 40% at one point, investors remain cautious following a weak lead from European markets and the closure of Wall Street for a federal holiday. The ASX 200 is down 0.20%

- New Zealand's equities are higher this morning, following positive GDP data indicating the economy exited recession with a 0.2% expansion in Q1, surpassing economist estimates of 0.1% growth. The upbeat GDP data is seen as reducing the likelihood of early rate cuts, the NZX 50 is 0.65% higher heading into the close.

- Elsewhere, foreign investors continue to sell stocks in Indonesia, Thailand, Philippines with all markets trading near or at their ytd lows. Singapore equities are down 0.30%, Malaysian equities are 0.45% lower, Philippines equities are 0.35%, Thailand equities are down 0.25% Indian equities are unchanged, while Indonesian equities are up 0.90%.

ASIA STOCKS: Equities Head Lower, Amid A Lack Of Policy Updates

Hong Kong and China equity markets are lower today. In Hong Kong, stocks opened higher on hopes for market-boosting measures from Chinese authorities, but overall gains were limited and have since vanished. While Chinese onshore markets opened lower amid ongoing economic concerns and a lack of fresh policy catalysts.

- Hong Kong equities are mostly lower this morning with the HSI 0.48%, HSTech Index is 1.35% lower, while property is the worst performing sector with the Mainland Property Index down 2.09% and the HS Property Index down 1.36%

- China onshore equities are also lower today with the CSI 300 Index down 0.49%. Small-cap indices also fell, with the CSI 1000 down 1.37% and the CSI 2000 down 1.62%. The CSI 300 Real Estate Index saw a significant decline of 2.33%.

- Investors are awaiting policy developments, especially regarding the potential waiver of the 20% tax on dividends from Hong Kong stocks bought via Shanghai and Shenzhen links. This uncertainty continues to weigh on market sentiment.

- Chinese authorities' cautious stance on monetary easing, despite the economy's struggles, is contributing to investor caution. The PBOC's focus on maintaining exchange rate stability is a key factor in their policy decisions.

- The CSRC introduced eight measures to reform the STAR market in Shanghai, focusing on facilitating M&As, optimizing IPO pricing, increasing lock-up periods for institutional investors, enhancing supervision, and improving the efficiency of financing approvals.

- Later today we have BoP Current Account Balance, and CPI composite at 1830 AEST/ 1630 HKT

FOREX: G10 Little Changed, Rupiah Weakening Ahead Of BI Decision

With the US closed yesterday and few events today, currencies have generally stayed in narrow ranges. The US dollar is slightly higher with the BBDXY index at 1265.12.

- Despite stronger-than-expected Q1 GDP, NZDUSD is now flat on the day at 0.6133 after falling to 0.6125 following the post-data high of 0.6148.

- AUDUSD is down slightly at 0.6671 after trading between 0.6667 and 0.6678. AUDNZD is also lower at 1.0876 following a low of 1.0852.

- USDJPY is little changed at around 158.13, following a low of 157.92 and close to the intraday high.

- Ahead of today’s BoE decision GBPUSD is around 1.2714. The SNB also meets and USDCHF is 0.8838. EURUSD is steady at 1.0742.

- The USDCNY fix today was 88pips wider than yesterday. USDCNH rose to 7.2877 following the announcement, but is now around 7.2842. The 1- and 5-year LPRs were unchanged.

- Bank Indonesia (BI) is expected to keep rates at 6.25% today, but there is a material risk of a hike given that USDIDR is rising again and is currently around 16422, above the June 14 high and up 2.7% since the May 22 meeting. It reached a high of 16425 earlier today. This is likely to keep BI sounding hawkish and focussed on FX stability (see MNI BI Preview June 2024).

- USDKRW is up 0.2% at 1384.25 and has oscillated around 1384 for much of the session. The won was pressured by the softer yuan.

- Later the Fed’s Kashkari and Barkin speak and the BoE & SNB decisions are announced. The eurogroup meeting also takes place. In terms of data, US Q1 current account, May housing starts/permits, June Philly Fed and jobless claims print.

INDONESIA: BI Concerned Rupiah Weakness Boosting Import Prices

Bank Indonesia (BI) meets today and while it is expected to keep rates at 6.25%, there is a material risk of a hike given that USDIDR is rising again and is currently around 16414, close to the June 14 high and up 2.6% since the May 22 meeting. This is likely to keep BI sounding hawkish and focussed on FX stability (see MNI BI Preview June 2024).

- While inflation is firmly within BI’s 1.5-3.5% target band, BI is concerned that the weak rupiah will increase inflation through the import channel. This is well founded as respondents in the May S&P Global manufacturing PMI survey observed that the softer currency is adding to their cost pressures, although they are struggling to pass them on in full.

- Import prices were disinflationary between November 2022 and February 2024. At their trough in July last year, they were down 11.4% y/y. This changed in March this year when they became positive and in April they picked up to 3.7% y/y.

- This upward trend in imported inflation looks likely to continue given its close correlation with the NEER which has weakened substantially in recent months. The JP Morgan NEER fell 0.3% m/m in May and 1.3% in June and is now down 5.3% y/y. Fiscal worries have been weighing on the rupiah.

Source: MNI - Market News/Refinitiv

EQUITY FLOWS: Foreign Inflows Into Local Equities Resume, But Sell Bonds Again

- Offshore investors returned to the Japanese equity market buying a net ¥80.0bn last week. The selling the previous week was the first outflow after 6 weeks. In terms of bonds, foreign investors sold securities to the tune of ¥235.8bn after two straight weeks of net purchases.

- In terms of Japan outbound flows, we saw some purchases of offshore bonds worth ¥653.6bn after the previous week's sharp selling, which was the largest weekly outflow since 2015. Returns have been unappealing on a FX hedged basis.

- Local investors continued to sell offshore stocks for the fourth straight week but last week saw some improvement with the lowest amount (-¥108.4bn).

Table 1: Japan Weekly Investment Flows

Billion Yen | Week ending June 14 | Prior Week |

Foreign Buying Japan Stocks | 80.0 | -346.2 |

Foreign Buying Japan Bonds | -235.8 | 404.4 |

Japan Buying Foreign Bonds | 653.6 | -2648.6 |

Japan Buying Foreign Stocks | -108.4 | -526.3 |

Source: MNI - Market News/Bloomberg

NZ ECO: Q1 Growth Soft But Improving, In Line With RBNZ Forecast

NZ Q1 GDP came in above expectations rising 0.2% q/q to be up 0.3% y/y after falling 0.1% q/q and 0.2% y/y. It remains weak and fell 0.3% q/q and 2.4% y/y per person. It has returned to positive territory though ending the technical recession. It was in line with the RBNZ’s forecast and so is unlikely to change the MPC’s wait-and-see stance. It expects growth to continue to improve with H2 around 0.4% q/q.

NZ GDP (production) %

Source: MNI - Market News/Refinitiv

- Expenditure-based GDP was soft on the quarter rising 0.1% q/q but is up 0.5% y/y after recording another 0.1% q/q rise in Q4. Q1 was driven by strong private consumption growth and a build in inventories. Whereas net exports, government spending and investment were negative.

- Private consumption rose 1.6% q/q contributing 1pp to GDP growth. It is now up 1.3% y/y after 0.2%. Whereas investment fell 1.3% q/q with the weakness broad-based but residential building down 3.7%. Imports rose 6.1% q/q which added to inventories. But it outpaced exports resulting in a net export drag of 2pp in Q1 after a 1.7pp contribution in Q4.

Source: MNI - Market News/Refinitiv

- Statistics NZ observes that half the industries it covers saw positive growth in Q1 with electricity generation and hiring & real estate services particularly strong, whereas construction, manufacturing and business services fell.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/06/2024 | 0600/0800 | ** |  | DE | PPI |

| 20/06/2024 | 0700/0900 |  | EU | ECB's Lagarde and Cipollone in Eurogroup meeting | |

| 20/06/2024 | 0730/0930 | *** |  | CH | SNB PolicyRate |

| 20/06/2024 | 0730/0930 | *** | | CH | SNB Interest Rate Decision |

| 20/06/2024 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 20/06/2024 | 1100/1200 | *** |  | UK | Bank Of England Interest Rate |

| 20/06/2024 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 20/06/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 20/06/2024 | 1230/0830 | * | | US | Current Account Balance |

| 20/06/2024 | 1230/0830 | *** | | US | Housing Starts |

| 20/06/2024 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 20/06/2024 | 1245/0845 | | US | Minneapolis Fed's Neel Kashkari | |

| 20/06/2024 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 20/06/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 20/06/2024 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 20/06/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 20/06/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 20/06/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 20/06/2024 | 1900/2000 | | UK | Question Time Leaders' Special | |

| 20/06/2024 | 2000/1600 | | US | Richmond Fed's Tom Barkin | |

| 21/06/2024 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.