Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

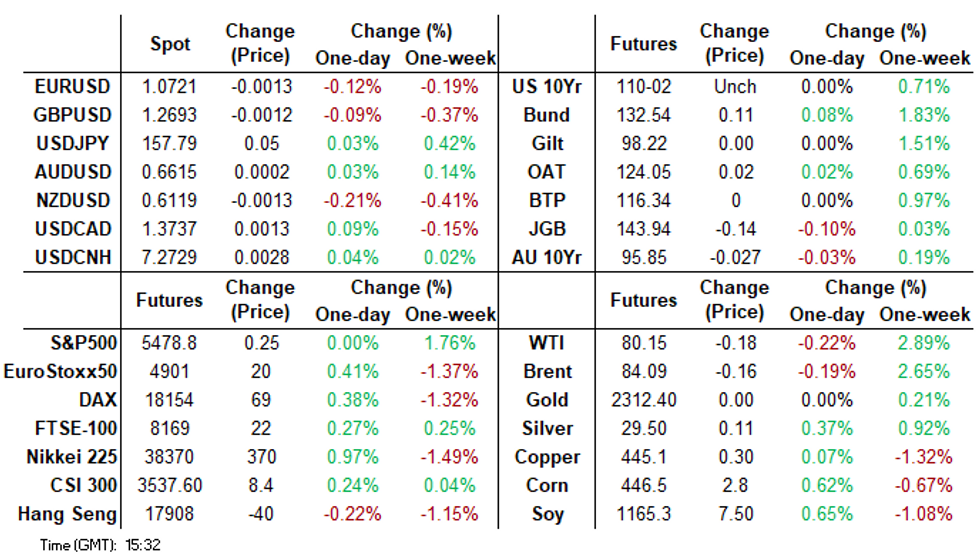

- US treasuries were little changed as the markets awaits US Retail Sales Data and Fed speakers later today

- Australia's RBA kept rates on hold at 4.35%, however warned that government spending risk fueling demand, and admitted inflation was stickier than expected.

- JGB's were weaker further out the curve as the BOJ Gov warned that the board could raise the policy interest rates at the July 30-31 meeting

MARKETS

TSYS: Tsys Futures Little Changed, Ranges Tight Ahead Of Fed Speakers

- Treasury futures are little changed today, ranges have been very tight with TUU4 -0-00⅛ at 102-04+, while TYU4 is +0-00+ at 110-13+.

- Volumes: TU 29k, FV 36k, TY 80k

- Cash treasury curve is little changed, yields are about 1bps lower across the curve. The 2Y -1.1bps to 4.754%, 7Y -1.1bps to 4.68%, with the 10Y -1.2bps at 4.269%.

- APAC Markets: ACGB yields are 3-4bps higher, NZGB yields are flat to 1.5bps higher, while JGBs are flat to 5bps higher, with better selling seen in the long end.

- Short end selling sees rate cut projections cooling vs. late Friday levels (*): July'24 at -10% w/ cumulative at -2.5bp at 5.302%, Sep'24 cumulative -17.5bp (20bp), Nov'24 cumulative -26.6bp (-29.9bp), Dec'24 -46.1bp (-50.5bp).

- Looking ahead, Retail Sales, IP/Cap-U and TIC Flows, Several Fed speakers on tap as well.

NZGBS: Closed Little Changed But The Session’s Best Levels

NZGBs closed little changed but at the session's best levels across benchmarks. With the domestic calendar light, the local market benefited from a stronger tone to its $-bloc counterparts in today’s Asia-Pac session.

- Cash US tsys were 1-2bps richer in today's Asia-Pac session after yesterday's sell-off.

- Ahead of the RBA Policy Decision (1430 AEST), ACGBs were also near session highs with benchmark bonds 1-2bps richer.

- Nevertheless, the NZGB 10-year outperformed on the day, with the NZ-US and NZ-AU yield differentials both 2bps tighter.

- Swap rates closed unchanged.

- RBNZ dated OIS pricing closed 1-2bps firmer for 2025 meetings. A cumulative 29bps of easing is priced by year-end.

- Tomorrow, the local calendar will see Q1 Current Account Balance data, ahead of Q1 GDP on Thursday.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.5% May-31 bond, NZ$200mn of the 4.25% May-34 bond and NZ$50mn of the 5.0% May-54 bond.

ACGBS: Slightly Cheaper After The RBA’s Policy Decision

ACGBs (YM -3.4 & XM -3.9) sit a little cheaper and at session cheaps after the RBA Policy Decision. The last two paragraphs of the RBA statement were little changed from the last meeting. To summarise:

- The RBA Board prioritises returning inflation to target, aligning with its mandate for stability and full employment. While inflation has eased slowly, it remains high. The Board remains vigilant to risks, relying on data to guide interest rate decisions, and will closely monitor economic developments.

- Cash ACGBs are slightly cheaper after the decision, with yields 3bps higher on the day. The AU-US 10-year yield differential is at -13bps after being at -15bps earlier in the day.

- Swap rates are 1-2bps higher after the decision.

- The bills strip has shifted cheaper, with pricing -2 to -5.

- RBA-dated OIS pricing is flat to 2bps firmer across meetings after the decision. Currently, the market is pricing approximately 13bps of easing by year-end from an anticipated terminal rate of 4.34%. In the run-up to the RBA’s May Policy meeting, the market was pricing no easing by year-end from an anticipated terminal rate of 4.42%.

- Tomorrow, the local calendar is empty part from the AOFM's planned sale of A$800mn of the 2.75% Jun-35 bond.

JGBS: Bear-Steepener After BoJ Ueda’s Comments, BoJ’s April Minutes Tomorrow

JGB futures are weaker and at session cheaps, -19 compared to settlement levels, after today’s remarks in Parliament by BoJ Governor Ueda.

- (MNI) Bank of Japan Governor Ueda told lawmakers Tuesday the Board could raise the policy interest rate at the July 30-31 meeting when the bank announces the detailed plan to reduce its government bond buying. Ueda, however, noted raising the policy interest rate will depend on developments of economic activity and prices at that time. He also said any hike decision would be separate from the JGB reductions.

- Today's BoJ Rinban operations saw mixed results, with both positive and negative spreads and both higher and lower offer cover ratios across the buckets. On balance, the operations generated some slight pressure on longer-dated JGBs in the early rounds of the Tokyo afternoon session.

- Cash US tsys were 1-2bps richer in today's Asia-Pac session.

- The cash JGB curve has bear-steepened, with yields flat to 4bps higher. The benchmark 10-year yield is 1.2bps higher at 0.947% versus the cycle high of 1.101%.

- The swaps curve has twist-steepened, pivoting at the 10s, with rate movements bounded by -0.5bp and +2bps. Swap spreads are mostly tighter.

- Tomorrow, the local calendar will see Trade Balance and Tokyo Condominiums for Sale data alongside the BoJ Minutes of the April Meeting.

GOLD: Fed Speak Weighs

Gold is slightly higher in the Asia-Pac session, after closing 0.6% lower at $2319.14 on Monday.

- Bullion was hit by waning optimism with regards to multiple Federal Reserve easing this year following a series of hawkish statements from officials.

- Fed Bank of Philadelphia President Harker stated on Monday that he considers one rate 25bps cut appropriate for this year, echoing similar remarks made by his counterparts from Minneapolis and Cleveland over the weekend.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- Gold is sitting approximately 5% below its May 20 record high.

- The recent trading below the 50-day EMA at $2,314.7 has opened the possibility of reaching $2,277.4, the low from May 3, according to MNI’s technicals team. The initial firm resistance to monitor is $2,387.8, the high from June 7.

LNG: Natural Gas Sells Off As Supply Conditions Improve

Natural gas prices fell on Monday. European LNG fell 3% to EUR 34.29 on Monday to be little changed in June. Flows returning to usual rates, forecasts of warmer weather and seasonally high storage levels weighed on prices. A cool start to summer has seen UK gas demand rise sharply in June to date.

- After maintenance and outages, supplies from Norway are above their 30-day average, according to Bloomberg. Russian gas coming through the Ukraine was also flowing as usual.

- US natural gas fell 3.3% to $2.79 despite hot weather but is still 7.7% higher this month. The forecast for the next 10 days though is showing that temperatures should come down, according to EBW AnalyticsGroup.

- The American Petroleum Institute has asked for the halt on new LNG export permits to be cancelled.

- North Asian markets followed Europe with prices down 2% to be up 3.1% in June.

OIL: Crude Supported By Positive Risk Tone, US Retail Sales Later

Oil prices are holding onto most of yesterday’s gains. They are marginally lower during APAC trading today after rising over 2% on Monday. Benchmarks have found support from better risk sentiment as equities and other commodities rise. Brent is down 0.2% to $84.07/bbl, after a low of $84.05. WTI is also 0.2% lower but is holding above $80 at $80.15/bbl. The USD index is slightly higher.

- With geopolitics currently in the background, supply/demand fundamentals are at the fore. The demand outlook remains uncertain but the market has been concerned about Asia for some time. China’s refining output fell 1.8% y/y in May and India is reporting softer petrol consumption.

- CBA thinks that OPEC’s management of supply will keep the H2 average of Brent between $80 and $85/bbl, according to Bloomberg.

- Last week the EIA reported an unexpected crude inventory build in the US. The API releases its data later today.

- Later there are numerous Fed speakers including Barkin, Collins, Logan, Kugler, Musalem and Goolsbee as well as the ECB’s de Guindos. US May retail sales print and core sales are expected to rise. US May IP & April inventories and euro area May CPI and German June ZEW are released.

ASIA STOCKS: Asian Equities Head Higher, Led By Tech, RBA Keeps Rates On Hold

Asian stock markets experienced gains today, driven by a recovery in Japanese equities following previous losses due to concerns over political turmoil in France. The MSCI Asia Pacific Index rose by up to 0.8%, marking its best performance in over a week, supported largely by strong performances in chip-related shares like TSMC and Samsung, following gains in their US counterparts. Australian stocks held onto gains after the Reserve Bank of Australia (RBA) maintained its key interest rate at a 12-year high of 4.35%, signaling a cautious approach amidst global economic uncertainties. Overall, optimism over tech sector strength and expectations of stable monetary policy in Australia contributed to positive sentiment across the region's markets today.

- Japanese stocks rebounded strongly from Monday's slump, tracking US shares higher. The benchmark Nikkei 225 index climbed 0.87%, while the Topix index rose 0.53%. Tech shares led the gains, with Tokyo Electron up 1.94% and Fanuc gaining 1.17%. Exporters also contributed significantly, with Toyota rising 1.12% and Honda jumping 2.13%. The positive sentiment was supported by optimism over a resilient US economy and easing political concerns in France.

- South Korean stocks opened higher, reflecting overnight gains on Wall Street. The KOSPI is 0.73% higher with large caps leading the way higher, with the small-cap Kosdaq trading down 0.25%. Samsung Electronics adding 1.79% and SK Hynix jumping 3.59%. Hyundai Motor and LG Energy Solution also posted gains of 1.62% and 1.49%, respectively, which contributed the most to index gains. Foreign investors were net buyers of equities on Monday, with that trend continuing this morning.

- Taiwan equities are currently up 1.12%, driven by gains in semiconductor stocks. TSMC contributed significantly to the index's rise, gaining as much as 3.2% after Citigroup raised its price target by 12% to NT$1,150, citing strong utilization-rate recovery and advanced node demand, while Morgan Stanley also increased TSMC’s price target to NT$1,080, highlighting potential upside from Apple Silicon and Edge AI processors.

- Australian stocks advanced, buoyed by the rally in US technology stocks. The RBA is kept its benchmark cash rate at a 12-year high of 4.35% for a fifth straight meeting. The ASX200 is currently up .90%

- Elsewhere, New Zealand equities are 0.40% earlier Westpac Consumer Confidence for Q2 was 82.2 vs 93.2 prior. Singapore equities are 0.15% higher, Malaysian equities are 0.27% higher, Thailand equities are 0.90% higher, Indian equities are 0.45% higher

ASIA STOCKS: China & HK Equities Mostly Higher, Property Weighs On Sentiment

Hong Kong and China equities had a mixed performance today, influenced by positive developments in Tesla’s operations in Shanghai and regulatory changes in Hong Kong, while also weighed down by persistent concerns in the Chinese property market and mixed economic data. Overall, while tech and semiconductor stocks provided a boost, concerns over the property market and mixed economic indicators continued to cast a shadow over the broader market sentiment.

- Hong Kong Equities, the HSTech Index rose by 0.62%, the Mainland Property Index remained relatively flat, down just 0.10%, while the HS Property Index was slightly up by 0.10%, while the broader Hang Seng Index (HSI) increased by 0.45%.Hong Kong's bourse will now remain open during typhoons or torrential rains starting September 23, aligning with global practices, as announced by Chief Executive John Lee.

- China Onshore Equities, Small-cap indices saw gains with the CSI 1000 up by 0.90% and the CSI 2000 rising by 1.10%. The CSI 300 Real Estate Index fell by 0.46%, while the broader CSI 300 Index increased by 0.35%. The growth-focused ChiNext Index was up by 0.46%.

- Shares of Tesla’s China suppliers advanced following news of Shanghai’s approval for Tesla to test its advanced driver assistance system, boosting companies like NavInfo (+2.7%), Zhejiang Sanhua Intelligent (+2.7%), Lens Technology (+3.4%), and VT Ind Tech (+2.5%).China's pork-related stocks rose after the nation initiated an anti-dumping probe on EU imports, with New Hope Liuhe up 2.2% and Jiangxi Zhengbang Technology up 3%. Copper prices slipped to an eight-week low due to weak economic data from China, emphasizing the ongoing challenges in the property sector despite various government measures.

- Looking ahead, focus will turn to China's 1yr & 5yr LPR and Hong Kong Unemployment Rate on Thursday

ASIA STOCKS: Equity Flows Muted, As Majority Of Regions Closed Monday

- South Korean equities were lower on Monday, (Kospi down 0.52%, Kosdaq down 0.37%). Flows were muted with just a small $99m outflow , the past 5 session now netting a total inflow of $1.61b. The Kospi have now failed three times since March to trade above 2,780, with focusing turning to PPI on Friday. The 5-day average is $321m, above both the 20 day average of $34mm and the longer-term 100-day average at $150m.

- Taiwan equities were unchanged on Monday with a small inflow of $73m. The Taiex continues to make new all time highs. The past 5 session's seeing a total inflow of $1.5b with the 5-day average now $304m, above both the 20-day average at $20m, while the 100-day average is just $40m.

- Thailand equities were again lower on Monday, down 0.76% and off 1.67% for the past 5 sessions. Foreign investors continue to sell equities as we now have marked the 18 straight session of selling for a total outflow of $951m with $285m of that coming in the past 5 sessions. The Thai SET continues to make new lows and we now trade back at Dec 2020 levels. The 5-day average is now -$57m, below both the 20-day average at -$46m and the 100-day average at -$25m.

- Indonesia, Philippines, India & Malaysia were closed for Public Holiday on Monday

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -99 | 1610 | 15898 |

| Taiwan (USDmn) | 74 | 1524 | 4069 |

| India (USDmn)** | 0 | 1405 | -3386 |

| Indonesia (USDmn)** | 0 | -44 | -423 |

| Thailand (USDmn) | -73 | -285 | -2775 |

| Malaysia (USDmn) ** | 0 | 13 | -3 |

| Philippines (USDmn) ** | 0 | -15.3 | -481 |

| Total | -99 | 4208 | 12899 |

| * Public Holiday |

ECO: RBA On Hold, Remains “Vigilant To Upside Risks”

The RBA left rates at 4.35% as was unanimously expected. Its hawkish neutral stance was unchanged reiterating that it is “not ruling anything in or out” and that the Board will “remain vigilant to upside risks to inflation”. It returned to acknowledging the uncertainties around the consumption outlook and reinforced its resolution to return inflation to target by adding that it “will do what is necessary to achieve” that outcome. The RBA remains highly data dependent and cautious and is yet to be confident that inflation is returning to target. It is taking things meeting by meeting.

- Key parts of the May statement were unchanged including that higher rates are working, excess demand persists, wage and productivity growth aren’t yet at sustainable rates, and return to target is “unlikely to be smooth”. Importantly, the Board is yet to feel “confident” that inflation will return to target and it will still be “some time before inflation is sustainably” in the corridor.

- The Board acknowledged the upward revisions to consumption in Q1 GDP and reverted to recognising the uncertainty around household spending. It noted the revisions and the persistent inflation “suggest that risks to the upside remain”. It notes numerous factors that should support expenditure going forward including July 1 tax cuts, wealth effects from rising house prices and lower inflation. But uncertainties mean there is also a risk it disappoints.

- Federal and state budgets “may also have an impact on demand” but energy “rebates will temporarily reduce headline inflation”.

- The RBA also added concerns that supply chains may be impacted by recent geopolitical uncertainties, which would add to price pressures.

- See full statement here.

FOREX: Currencies Range Trading During Asian Session

Most currencies have been trading in narrow ranges during the APAC session today with kiwi the largest mover. The BBDXY USD index is little changed rising only slightly to around 1267.20. USDJPY fell somewhat following comments from BoJ Governor Ueda not ruling out a rate hike in July but is now little changed (see MNI BOJ's Ueda Sees Possible July Lift To Policy Rate).

- Ueda said that any rate move would depend on growth and inflation and would be separate from plans to reduce JGB purchases. USDJPY fell to 157.52 following the remarks but is currently trading around 157.70 to be down only slightly.

- Kiwi has underperformed with NZDUSD down 0.2% to 0.6117, close to the intraday low.

- AUDUSD was down 0.1% before the RBA decision after a little post meeting volatility it is now marginally higher at 0.6616 as the statement was a touch more hawkish (see MNI RBA On Hold, Remains "Vigilant To Upside Risks"). AUDNZD is 0.3% higher and has exceeded the 1.080 level at 1.0814, close to the intraday high.

- They CNY fixing was 58pips tighter than yesterday. USDCNH is slightly higher today at 7.2734.

- Asian currencies are generally little changed with USDKRW steady around 1381.30 and USDTHB down 0.1% to 36.78.

- Later there are numerous Fed speakers including Barkin, Collins, Logan, Kugler, Musalem and Goolsbee as well as the ECB’s de Guindos. US May retail sales print and core sales are expected to rise. US May IP & April inventories and euro area May CPI and German June ZEW are released.

MARKETS UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/06/2024 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 18/06/2024 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 18/06/2024 | 0900/1100 | *** |  | EU | HICP (f) |

| 18/06/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 18/06/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 18/06/2024 | 1200/1400 | | EU | ECB's Cipollone chairing session on market supervision | |

| 18/06/2024 | 1230/0830 | *** |  | US | Retail Sales |

| 18/06/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 18/06/2024 | 1315/0915 | *** | | US | Industrial Production |

| 18/06/2024 | 1330/1530 | | EU | ECB's De Guindos at EC and ECB joint conference | |

| 18/06/2024 | 1400/1000 | * | | US | Business Inventories |

| 18/06/2024 | 1400/1000 | | US | MNI Webcast with Richmond Fed's Tom Barkin | |

| 18/06/2024 | 1540/1140 | | US | Boston Fed's Susan Collins | |

| 18/06/2024 | 1700/1300 | | US | Fed Governor Adriana Kugler | |

| 18/06/2024 | 1700/1300 | | US | Dallas Fed's Lorie Logan | |

| 18/06/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 18/06/2024 | 1720/1320 | | US | St. Louis Fed's Alberto Musalem | |

| 18/06/2024 | 1800/1400 | | US | Chicago Fed's Austan Goolsbee | |

| 18/06/2024 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.