Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- At the July RBA meeting, the Board discussed both a 25bp hike and a pause but decided that the arguments for the latter were “stronger”. This time it appears that the decision was not “finely balanced”, but the minutes indicate that the cycle may not yet be over and that decisions remain very data dependent. Tomorrow, we get NZ CPI, which is expected to print weaker than RBNZ projections.

- More broadly, supply chain issues were one of the reasons why G20 inflation rose above rates not seen since the series began in 1997. But they have been easing for around a year now and signal further downward pressure on headline inflation from this source.

- Elsewhere, fresh support for China households was overshadowed somewhat by renewed property developer concerns.

- There is a thin data calendar in Europe today, further out Canadian CPI and US Retail Sales cross.

MARKETS

GLOBAL: Inflation Should Keep Moderating As Supply Chain Tensions Resolve

Supply chain issues were one of the reasons why G20 inflation rose above rates not seen since the series began in 1997. But they have been easing for around a year now and signal further downward pressure on headline inflation from this source.

- The Federal Reserve Bank of New York’s measure of global supply chain pressures fell further in May to -1.56, lowest since November 2008, but then ticked up to -1.2 in June. On a 3-month average basis it is unchanged at a very low level. It is indicating that global inflation pressures should continue to ease over the months ahead.

- G20 headline CPI inflation eased in May to 5.9% from 6.5% and a peak of 9.5% in September 2022. June is likely to moderate further with US, euro area and non-Japan Asian inflation declining again. Underlying price pressures have been stickier in coming down, thus keeping central banks alert.

Source: MNI - Market News/Refinitiv

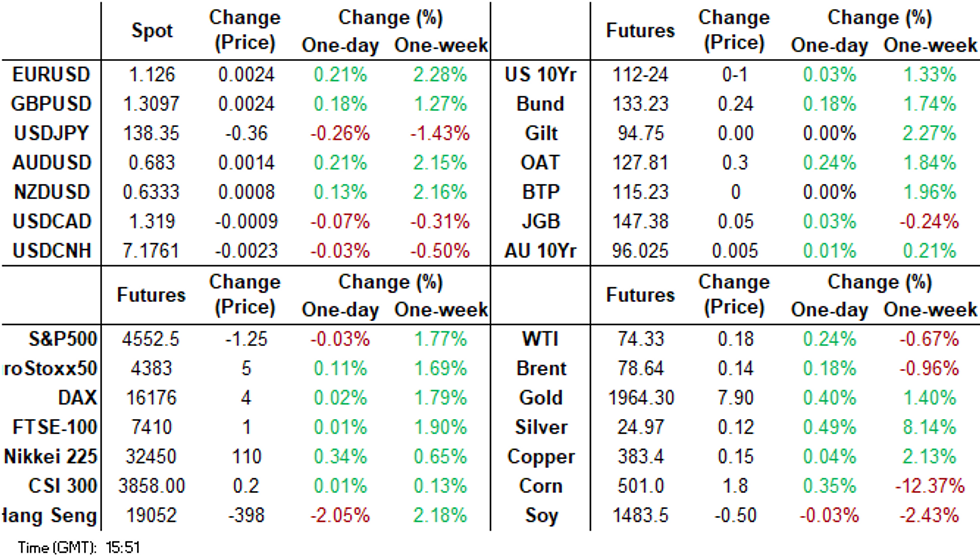

US TSYS: Marginally Firmer In Asia

TYU3 deals at 112-23+, +0-00+, a 0-04+ range has been observed on volume of ~32k.

- Cash tsys sit 1-2bps richer across the major benchmarks, light bull steepening is apparent.

- Tsys firmed in early dealing as a bid in JGBs spilled over despite the absence of any headline driver.

- A block buyer in FV, 2,312 lots, added a level of support.

- Little in meaningful macro news flow crossed and tsys held richer for the remainder of the session.

- The docket is thin in Europe today. Further out we have retail sales, industrial production and business inventories.

STIR: US Market Unwilling To Price Higher For Longer Outlook

The US market is currently indicating a 33bp easing by the end of March 2024 from a 5.37% terminal rate, while the other $-bloc markets show almost no chance of easing.

- Conversely, the CA and NZ STIR markets are adopting a higher-for-longer outlook.

- RBA-dated OIS continues to price a narrowing in the official rate differential with the other $-bloc markets but remains unique in projecting a cash rate below 5.0% by the end of March 2024.

Figure 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

ECB: Visco Expects Inflation To Decline Faster Than ECB Forecast

ECB governing council member and Bank of Italy Governor Visco has given an interview to Bloomberg TV and said that he believes inflation will return to 2% faster than the ECB’s forecast of end-2025. He expects lower energy prices to result in a significant moderation in core inflation. A recession shouldn’t be necessary to contain inflation (our recession probability model indicates only a small chance of a recession). Visco believes that the ECB needs to find a balance so that it doesn’t do too much or too little. He is also happy with the pace of ECB bond portfolio reduction. The next ECB meeting is on July 27 and the market has a 25bp hike almost fully priced in.

JGBS: Futures Richer, Mid-Range, Liquidity Enhancement Auction Tomorrow For OTR 1-5-Year JGBs

JGB futures are dealing in the middle of the Tokyo session range in afternoon trade, +7 compared to settlement levels.

- There haven't been many specific domestic drivers worth noting, except for the growing speculation surrounding a potential adjustment to the YCC policy at the upcoming policy meeting of the BoJ next week.

- JGB futures have a downside bias into the Japan inflation report due on Friday, according to Bloomberg. (See link ICYMI)

- May Tertiary Industry Index rises 1.2% m/m versus +0.4% est.

- The cash JGBs are trading mixed with yield movements ranging from 0.5bp lower (7-year zone) to 2.6bp higher (40-year). The benchmark 10-year yield is 0.3bp lower at 0.478%, just shy of its highest level in three months of 0.485% set on Friday.

- Swap rates are also mixed across the curve with changes ranging from +/-0.8bp. Swap spreads are generally wider out to the 7-year and tighter beyond.

- Tomorrow the local calendar has no data. The MoF does however plan to sell Y500bn at a Liquidity Enhancement Auction for OTR 1-5-year JGBs.

- Later today sees June US retail sales and industrial production, May US business inventories, and the July NAHB housing market index.

AUSSIE BONDS: Slightly Richer, July Decision Not Finely Balanced (RBA Minutes)

ACGBs are dealing slightly higher (YM +3.0 & XM +1.0) after the release of the RBA Minutes for the July meeting.

- The Board discussed both a 25bp hike and a pause but decided that the arguments for the latter were “stronger”. This time it appears that the decision was not “finely balanced”.

- The minutes indicated that the cycle may not yet be over and that decisions remain very data dependent, as growth concerns seem to have increased. Q2 CPI is due on July 26 and staff forecasts are likely to be key components in the August 1 outcome.

- Cash ACGBs are 1-3bp richer with the AU-US 10-year yield differential at +17bp.

- Swap rates are 2-3bp lower with the 3s10s curve steeper.

- Bills pricing is +2 to +4.

- RBA dated OIS pricing 1-5bp softer across meetings.

- Tomorrow the local calendar sees Westpac -MI Leading Index.

- Commodity prices declined on Monday after China’s economy grew slower than expected in the second quarter, adding to concern about the lacklustre recovery for Australia’s largest export partner. Fund managers say the big concern for the market is whether authorities will step in and announce more meaningful economic stimulus. (See link)

- Tomorrow the AOFM plans to sell A$800mn of the 3.50% 21 December 2034 bond.

RBA: August Meeting Live, Watch Q2 CPI & June Labour Data

At the July meeting, the Board discussed both a 25bp hike and a pause but decided that the arguments for the latter were “stronger”. This time it appears that the decision was not “finely balanced” but the minutes indicate that the cycle may not yet be over and that decisions remain very data dependent, as growth concerns seem to have increased. Q2 CPI due on July 26 and staff forecasts are likely to be key components in the August 1 outcome.

- The statement that “some further tightening of monetary policy may be required to bring inflation back to target within a reasonable timeframe” was repeated in the minutes from the meeting statement. This suggestion of further hikes had been omitted from the June minutes. Thus the August meeting remains live.

- One of the key reasons for the pause was to have time to “assess the impact” of recent tightening and the minutes note specifically that at the August meeting the Board will have more information on inflation (ie Q2 CPI data), global economy, labour market (July 19) and household spending plus updated RBA forecasts and “revised assessment of the risks” (ie. to achieving inflation target by mid-2025).

- The risk that growth slows more than expected driven by weaker consumption and thus unemployment rises more than forecast was discussed giving the minutes a more dovish tone. The RBA paused because of lags, restrictive stance, further refis, declining inflation & lower commodity/shipping costs, slowing growth and uncertainties.

- Inflation concerns were more explicit in the minutes than the meeting statement. The case for a hike included the risk that the inflation target wouldn’t be met by mid-2025, high rent, services & electricity prices, strong unit labour cost growth, sticky overseas inflation, tight labour market and the risk to wages.

NZGBS: Closed Richer Ahead Of Q2 CPI Tomorrow

NZGBs closed on a positive note with benchmark yields flat to 2bp lower ahead of Q2 CPI tomorrow. Without meaningful domestic drivers, local participants have been content to monitor developments in US tsys and ACGBs. NZ/US and NZ/US 10-year yield differentials closed little changed.

- Tomorrow sees the release of Q2 CPI with economists expecting the quarterly pace to step down to +0.9% q/q from +1.2% in Q1. This will leave the annual rate at +5.9% down from +6.7%. If analysts are correct, then inflation would be below RBNZ’s Q2 forecast of +1.1% q/q and +6.1% y/y. The RBNZ appears to be on hold for now, unless inflation isn’t in the target band by H2 2024, with the risk to rates likely to stem from sticky non-tradeable inflation (+1.0% q/q versus +1.7% prior).

- Swap rates are flat to 3bp lower with the 2s10s curve flatter.

- RBNZ dated OIS closed little changed with terminal OCR expectations sitting at 5.64%.

- The latest 1News/Verian poll showed support for the incumbent Labour Party down 2pp to 33% but the opposition Nationals also down 2pp to 35%. The NZ election is scheduled for October 14.

- Later today sees June US retail sales and industrial production, May US business inventories, and the July NAHB housing market index.

NZ DATA: Q2 CPI Expected To Slow More Than RBNZ Forecasts

Q2 CPI data is released on Wednesday July 19 and economists expect it to moderate further. The quarterly pace is forecast to step down to 0.9% q/q from 1.2% in Q1 to leave the annual rate at 5.9% down from 6.7%. If analysts are correct then inflation would be below the RBNZ’s Q2 forecast of 1.1% q/q and 6.1% y/y. The RBNZ appears to be on hold for now, unless inflation isn’t in the target band by H2 2024, with the risk to rates likely to stem from sticky non-tradeables inflation.

- If the CPI rises 0.9% as expected, that would be the smallest quarterly increase since Q1 2021. The annual rate will be helped significantly by base effects from tradeables inflation as the Ukraine-war-impacted Q1 2022 +2.4% q/q drops out. More moderate non-tradeables, driven by lower construction costs, should also assist.

- Analysts’ estimates are in a narrow range between 0.8% and 1.2% q/q and 5.8% and 6% y/y. ASB and Westpac both expect 0.9% & 5.9%, ANZ 1.0% & 5.9%, Kiwibank 1.0% & 6.0% and BNZ 1.1% & 6.0%.

- The tradeables CPI is forecast to rise 0.9% q/q in Q2 after 0.7% and domestically-driven non-tradeables by 1% following 1.7%. The latter will be watched closely for signs that it is “sticky”.

FOREX: Greenback Marginally Pressured In Asia

The USD is marginally pressured in Asia, BBDXY is down ~0.1%, however ranges do remain relatively narrow thus far on Tuesday. Chinese authorities have announced measures to boost household consumption however market impact has been fairly modest.

- AUD/USD prints at $0.6825/30, the pair is ~0.2% firmer and has pared some of Mondays losses. The latest minutes showed that the RBA remains very data/forecast dependent but did have a more dovish tone with discussion of downside risks to growth and the removal of “finely balanced”.

- Kiwi is firmer, NZD/USD is up ~0.2%. The pair was supported at $0.6320 in early dealing and has firmed through the Asian session. Ranges do remain narrow with a $0.6320/40 persisting for the most part.

- Yen is also marginally firmer, USD/JPY is down ~0.1%. The pair firmed in early dealing however resistance was seen ahead of ¥139 and losses were erased. Resistance comes in at ¥140.18 the 50-Day EMA, support is seen at ¥137.25 low from July 14.

- Elsewhere in G-10 EUR and GBP are both ~0.2% higher.

- Cross asset wise; Regional Equities and US Equity futures are lower. Hang Seng is down ~2% and e-minis are ~0.2% lower. US Tsy Yields are at touch softer across the curve.

- There is a thin data calendar in Europe today, further out Canadian CPI and US Retail Sales cross.

EQUITIES: Renewed China Property Woes Weighs On Broader Sentiment

Hong Kong markets have returned today and lost ground (HSI off by more than 2%). Japan markets are faring better on their return, but are only modestly higher in terms of the Topix. Trends are mixed elsewhere. US equity futures sit modestly in the red at this stage. Emini last just under 4550, -0.10% weaker, while Nasdaq futures were down 0.17%.

- The HSI is off by 2.17% at the break. Some catch up to the softer tone in mainland China shares yesterday post weaker data is in play, while renewed property market concerns is another headwind.

- Property developers have weighed on the HSI, amid a warning from Dalian Wanda Group on a funding short fall (it has a $400mn bond due on July 23). Elsewhere, China's Evergrande reported larges losses for the past two years, while a creditor is seeking bankruptcy for Evergrande's real estate Xian unit.

- The mainland CSI 300 is off 0.30% at the break, despite a rebound in consumer discretionary stocks as the authorities pledge to aid the consumption recovery.

- Elsewhere both the Kospi and Taiex are down despite positive leads from US tech related indices in Monday trade. Losses are under 0.50% at this stage.

- Japan shares are higher, although the Nikkei 225 is struggling to hold gains. The ASX 200 is down 0.36%.

- In SEA, the picture is mixed, although more markets are down than up.

OIL: Prices Up Slightly As Russian Cuts Balance China Demand Worries

Oil is up moderately during APAC trading following two days of sharp falls, helped by Russian intentions to reduce crude exports. WTI is up 0.4% to $74.41/bbl, just off the intraday high of $74.51. Brent is 0.3% higher at $78.75 after a high of $78.83. Crude swings today have also been impacted by moves in the greenback which is now down 0.1%.

- Oil prices are likely to remain very sensitive to demand indicators after China’s Q2 disappointed and a number of forecasters cut their growth projections. Treasury Secretary Yellen also warned of the risks to global growth and Australian Treasurer Chalmers said that China’s slowdown was “concerning”. China is the world’s largest crude importer.

- Offsetting demand concerns are expectations that the oil market will tighten in H2 2023. Russia plans to reduce Q3 2023 exports by 2.1mn tonnes in line with its announced August 500kbd cut, which should be aided by the Urals price exceeding the price cap.

- US API crude & product inventory data for last week are released later. There was a 3.03mn barrel build in the latest data according to Bloomberg.

- Later the Fed’s Barr and Gibson speak ahead of the blackout period before the July 26 meeting. US June retail sales, IP and July NAHB housing index, and Canadian June CPI print. The ECB’s Panetta speaks and updated European Commission forecasts are scheduled.

ASIA: Lower Food Prices Helping Asian Inflation Moderation

Supply chain issues were one factor that drove Asian inflation higher over 2021-2022 but food prices also contributed (see MNI Inflation Should Keep Moderating As Supply Chain Tensions Resolve). The local peak in FAO global food price inflation was in March last year at +34% y/y (wheat and oils were heavily impacted by Russia’s invasion of Ukraine) but were down 20.9% y/y in June this year. Food price deflation has stabilised in recent months at a very low level signalling further downward pressure on Asian headline inflation is likely in the coming months.

- All components were down on a year ago in June but Russia’s refusal to sign an extension of the grain deal with Ukraine could put upward pressure on cereal prices again, which are currently down 23.9% y/y. Oils are -45.3% y/y, dairy -22.2% and meat -6.4%. Sugar is the only main component to be higher at +29.7% y/y.

Source: MNI - Market News/Refinitiv/IMF/FAO

CHINA: Authorities Announce Measures To Boost Household Consumption

Headlines have crossed that the authorities are aiming to boost household consumption. A variety of measures will be utilized: the authorities will encourage financial institutions to strengthen credit support for households by providing loans at reasonable rates. The other focus will be on improving the quality of household goods and boosting the innovation of smart appliances for homes.

- The authorities will also kick off household goods promotion and encourage service platforms to create online platforms for household consumer services.

- These moves come in the wake of yesterday's slightly larger than expected fall in retail sales growth. A firmer uptick in household/consumer spending has largely been missing from the post Covid China economic rebound. No doubt these policies are aimed at improving these trends are we progress through H2.

- The market impact for these announcements has been fairly modest. USD/CNH sits below session highs, last around 7.1760, which is close to NY closing levels from Monday. Onshore equities are in the red (CSI 300 last down ~0.30%), as is Hong Kong's index. The consumer discretionary index of the CSI 300 is back in positive territroy though, last +0.24%.

GOLD: Treads Water Ahead Of US Retail Sales Today

Gold has shown slight strength (+0.25%) during the Asia-Pac session, having closed steady for the second consecutive day on Monday. Investors are carefully evaluating the impact of China's slow economic recovery on global growth, while also considering signs that the Federal Reserve is nearing the end of its monetary-tightening cycle. The US dollar and US Treasuries were tame ahead of the release of US retail sales data today.

- US Treasury Secretary Janet Yellen expressed concern about the repercussions of the sluggish Chinese economy, but she reassured that she doesn't foresee a recession in the US, where the inflation threat is diminishing. This has sparked optimism that the Fed might soon pause its rate hikes, which typically have a negative effect on gold due to its lack of interest-bearing nature.

- According to MNI's technicals team, gold remains reasonably close to resistance at $1968.0 (Jun 16 high) with an intraday high nudging $1960, whilst support is seen at $1934.4 (20-day EMA).

ASIA FX: THB & KRW Rally, More Modest Gains Elsewhere

Most Asia FX currencies are higher today, although outside of the standouts of THB and KRW, the gains have been fairly modest elsewhere. USD/CNH has been range bound, with positives in terms of efforts to drive higher consumption growth and a firmer CNY fixing, offset by renewed property developer concerns. THB has rallied on hopes the political impasse may be getting closer to an end. The local data calendar remains light tomorrow.

- USD/CNH sits slightly lower for the session, last near 7.1750. The CNY fixing bias firmed back to 200pips today, while the authorities are aiming to boost household consumption. This has been overshadowed somewhat by renewed concerns over China property developers, although China mainland shares are doing somewhat better after the break. The HSI is still off by ~2% though.

- 1 month USD/KRW got to fresh lows of 1255 not long after the stronger than expected CNY fixing result printed. We steadied from there, but the pair has mostly stayed under 1260 since. Earlier highs were just above 1264. 1250 is the next downside target. Won gains go against equity market weakness (Kospi - 0.51%, but Kosdaq +1.45%), but the majors are higher against the USD, with USD/JPY also lower, as US yields have pulled back further today.

- THB is the standout in Asia FX so far today. The pair last tracked near session lows in the 34.25/30 region, gains of ~1% in the session to date. We were last at these levels back in mid-May. This is sub all key EMA levels. In the first half of May we reached the 33.55/60 region, which could be a downside target for baht bulls. Recent highs come in just above the 35.00 level, which would also put us back above key EMAs (100 day is the nearest at 34.66). Optimism that Thailand may be closer to forming a new government, with Pita prepared to step aside if he fails to win support again, is aiding sentiment (this would see Pheu Thai PM candidate stand, most likely Srettha). This drop may take some of the risk premium out of the baht outlook, indeed it was one of the factors Goldman's highlighted as underpinning a fresh long recommendation in the currency.

- The Rupee is little changed thus far today as broader USD/Asia trends dominate early flows. USD/INR is a touch above the 82 handle, the pair has see-sawed around 82 in recent dealing with little follow through on moves. In RBI's latest monthly state of the economy report the bank noted that after an uptick in CPI in June the fight against inflation is far from over and monetary policy must remain tight to return inflation to target.

- The Ringgit is little changed from yesterday closing in early dealing. USD/MYR prints at 4.5340/4.5380, and has been dealing in a narrow range thus far. The Ringgit is held onto the majority of last week's post-US CPI gains sitting ~3% below last week's opening levels. Looking ahead the only data on the docket this week is June Trade Balance which crosses on Thursday. A surplus of MYR16.65bn is expected.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing, the measure sits a touch off cycle highs and is ~0.3% below the top of the band. USD/SGD is a touch lower in early trading, the pair is consolidating above the $1.32 handle in a narrow range and last prints at $1.3210/20. Broader USD trends continue to dominate flows. Looking ahead the local data calendar is empty for the remainder of the week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/07/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 18/07/2023 | - |  | EU | ECB Panetta at G20 Finance/Central Bank meeting | |

| 18/07/2023 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 18/07/2023 | 1230/0830 | *** | | CA | CPI |

| 18/07/2023 | 1230/0830 | * | | CA | Industrial Product and Raw Material Price Index |

| 18/07/2023 | 1230/0830 | *** |  | US | Retail Sales |

| 18/07/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 18/07/2023 | 1315/0915 | *** | | US | Industrial Production |

| 18/07/2023 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 18/07/2023 | 1400/1000 | * | | US | Business Inventories |

| 18/07/2023 | 1400/1000 | | US | Fed's Michael Barr | |

| 18/07/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 18/07/2023 | 2000/1600 | ** | | US | TICS |

| 19/07/2023 | 2245/1045 | *** |  | NZ | CPI inflation quarterly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.