Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

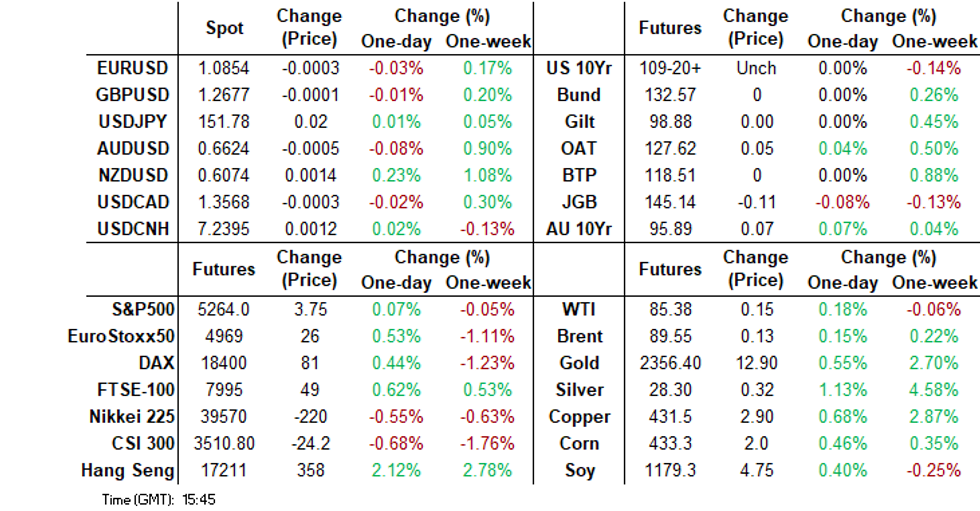

- US Tsy futures have tested Tuesday highs, albeit amid light volumes. The USD is slightly softer, mostly against the NZD, which has outperformed in the G10 space, post the RBNZ decision. The central bank left rates on hold as expected, but didn't give any fresh dovish hints around the outlook.

- Elsewhere, Fitch downgraded China's credit outlook to negative, citing the general trend around rising debt levels. The market impact has been limited though. China equities have underperformed, but these trends were in place ahead of Fitch news.

- Looking ahead, the main focus in the US session will be the CPI print, followed by the FOMC Mins.

MARKETS

US TSYS: Treasury Futures Test Tuesday's Highs Ahead Of CPI

- Jun'24 10Y futures has seen low volumes and remained in tight ranges, lows of 109-19+ were made during the morning session, before edging higher were we have been testing the highs from Tuesday of 109-23, currently the contract is up + 02 from NY closing levels at 109-22+.

- Looking at technical levels: Initial support lays at 109-00 (round number support), a break here would open up a move to 108-25+ (2.00 proj of Dec 27 - Jan 19 - Feb 1 price swing). While to the upside resistance holds at 110-06 (Apr 4 high), above here 110-24+/31+ (50-day EMA / Mar 27 high and key resistance)

- Cash Treasury curve has is a touch flatter today with the 2Y yield -0.6bp at 4.737%, 10Y -0.6bp to 4.356%, while the 2y10y +0.180 at -38.486.

- Cross markets, NZGBs yields are 1-3bps lower post the RBNZ decision to be 5-9bps lower on the day, while ACGBs yields are 3-8bps lower

- Looking Ahead: MBA Mortgage Applications, CPI and March FOMC minutes later today.

JGBS: Cheaper Apart From the 10Y, US CPI & FOMC Minutes Due, 20Y Supply Tomorrow

JGB futures are holding weaker, -8 compared to the settlement levels.

- There haven't been domestic data releases to highlight, apart from the previously mentioned PPI and Bank Lending data.

- The domestic market seems to have been influenced by remarks made by BoJ Governor Ueda in his Semi-Annual Report on Currency and Monetary Control. In addition to previously outlined comments, Ueda also said it’s undesirable for a central bank to hold a large volume of government bonds on the scale of the BOJ’s holdings over the long term. (See link)

- (Reuters) - BoJ Governor Ueda also said the central bank would not directly respond to currency moves in setting monetary policy, brushing aside market speculation that the yen's sharp falls could force it to raise interest rates. (See link)

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session ahead of today’s US CPI data and the release of the FOMC Minutes.

- Cash JGBs are flat to 2bps cheaper, apart from the 10-year. The benchmark 10-year yield is 0.7bp lower at 0.793% versus the YTD high of 0.802%, set earlier in the week.

- The swaps curve has bear-steepened, with rates 1-3bps higher.

- Tomorrow, the local calendar will see International Investment Flow, Money Stock and Tokyo Avg Office Vacancies data alongside 20-year supply.

AUSSIE BONDS: Richer, Awaiting US CPI Data & The FOMC Minutes

ACGBs (YM +3.0 & XM +8.0) are richer and near session highs. In the absence of domestic data, the local market has extended overnight moves in line with US tsys in today’s Asia-Pac session ahead of US CPI & the release of the FOMC Minutes. Cash US tsys are currently dealing 1bp richer. (See MNI U.S. CPI Preview: Apr 2024 - Key Framing Of Trends With June Cut Seen As A Coin Toss here)

- The latest round of ACGB Apr-27 supply went well, with pricing comfortably through mids and the cover ratio at a robust 3.8375x.

- There has also likely been a positive spillover from a 1-3bps richening in NZGBs following the RBNZ Policy Decision. The RBNZ's April monetary policy decision delivered few surprises.

- Cash ACGBs are 4-8bps richer, with the AU-US 10-year yield differential 3bps lower at -26bps, just above the bottom of the range it has traded in since late 2022.

- Swap rates are 5-7bps lower, with the 3s10s curve flatter.

- The bills strip has bull flattened, with pricing flat to +4.

- RBA-dated OIS pricing is flat to 5bps softer across meetings, with early-25 leading. A cumulative 32bps of easing is priced by year-end.

- Tomorrow, the local calendar sees CBA Household Spending and Consumer Inflation Expectations data.

NZGBS: Closed Richer & At Session Highs, Few Surprises From The RBNZ

NZGBs closed at the session’s best levels, 6-8bps richer, after the RBNZ's April monetary policy decision delivered few surprises. As expected, the decision was to hold rates steady at 5.50%.

- RBNZ board members acknowledged that most major central banks are “cautious” about easing policy given the risk of inflation remains sticky.

- The RBNZ noted that growth in unit labour costs remains elevated. Inflation will continue to be persistent in regions where higher labour costs have not been accompanied by improved productivity or reduced profit margins.

- The central bank also noted: "Overall, members agreed that the balance of risks was little changed since the February Statement."

- Cash US tsys have slightly extended yesterday’s richening in today’s Asia-Pac session ahead of US CPI data and the release of the FOMC Minutes.

- Swap rates are 4-8bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is flat to 2bps firmer after the decision, with 60bps of cumulative easing priced for year-end.

- Tomorrow, the local calendar sees Finance Minister Willis in front of a Select Committee on Budget Policy.

- Tomorrow, the NZ Treasury plans to sell NZ$275mn of the 3.0% Apr-29 bond, NZ$175mn of the 2.0% May-32 bond and NZ$50mn of the 2.75% May-51 bond.

RBNZ: Restrictive Policy Settings To Be Maintained

The RBNZ's April monetary policy decision has delivered few surprises. The central bank noted: "Overall, members agreed that the balance of risks was little changed since the February Statement." See this link for the full April statement.

- The central bank sees the need to maintain a restrictive policy stance for a sustained period to ensure that inflation returns to target in the 2024 calendar year.

- Recent growth outcomes have come in close to expectations, with economic growth described as weak, although this is likely necessary to ensure that capacity pressures are reduced further, which in turn will aid the return to the inflation target.

- Upside and downside risks to the inflation outlook were discussed, with some modest upside risks noted for Q1. Although as per above there has been little change in the balance of risks versus the Feb meeting.

- The RBNZ again noted there is limited tolerance for any increase in time to achieve the inflation target (again this point was also made at the February policy meeting).

- All in all, the RBNZ clearly sees it as being too early for a dovish shift in terms of the outlook. Whilst the bar to hike further is clearly elevated, the statement didn't give any hints that the restrictive policy stance will be changed in the near term.

- Note the next RBNZ meeting is on the 22nd of May. In terms of data releases between now and then, Q1 CPI prints on Apr 17. Wages and employment figures are out on May 1, then inflation expectations on May 13.

FOREX: NZD Outperforms Post RBNZ Decision

Outside of NZD gains, the general G10 FX tone has been a quiet one ahead of key event risks in the US later. The BBDXY was last near 1240.65, slightly down on end Tuesday levels.

- NZD/USD is up around 0.25% in latest dealings, which puts the pair at 0.6075. The RBNZ left rates on hold as expected, but didn't give off any dovish rhetoric. The central bank reiterated that restrictive policy has to be maintained for a sustained period to ensure a return to the inflation target.

- For NZD/USD we are right on Tuesday highs and testing resistance at the 50-day EMA. A break above would likely see 0.6100 targeted, while initial support is at 0.6040 (20-day EMA), then 0.6000 (round number support).

- AUD/USD sits slightly weaker, last near 0.6620. This has helped nudge the AUD/NZD cross back to 1.0900, with recent highs at 1.0950/60.

- USD/JPY has been steady, last in the 151.75/80 region. BoJ Governor Ueda was again before parliament. He noted the BOJ would consider monetary policy change should the risk of the underlying inflation rate rising above 2% increase due to higher import prices driven by the weak yen. His appearance didn't impact yen though.

- Looking ahead, the main focus in the US session will be the CPI print, followed by the FOMC Mins.

ASIA EQUITIES: HK Equities Surge Higher Lead By Tech, China Equities Underperform

Hong Kong and China equities are mixed today with Hong Kong equities again out-performing China mainland indices. The HSI is close to 2%, while the HS China Enterprise Index is now in bull market territory up 20% from lows mad Jan 22, while China Mainland Indices are lower with small-cap and growth stocks the worst performers. Tech stocks are the top performing sector lead higher by Tencent and Alibaba which have been supported by share buybacks and news of more approvals of online games. EV stocks have also rallied higher after EV penetration recovered in April.

- Hong Kong equities are higher today, led by the HSTech Index which is up 2.49%, the Mainland Property Index is up 1.42%, HS China Enterprise Index up 2.15% while the HSI is up 1.88%. China equity markets are lower today, with the CSI1000 erasing all of Tuesday gains, down 1.52%, while the CSI300 is faring a bit better down just 0.43%.

- China Northbound flows were 1billion yuan on Tuesday, with the 5-day average at -0.71billion, while the 20-day average sits at 1.42billion yuan.

- Over the past week in the property space, China Jinmao Holdings Group has told some investors it’s in talks with banks to refinance a HK$4 billion ($511 million) syndicated loan due in July. Country Garden’s President Mo Bin pledged to ensure delivery of the company’s housing projects during a monthly management meeting on Sunday. Sunac China will sell the remaining 51% stake in Chongqing College Town project and related debts to Chongqing Xiangyu Real Estate and Xiamen Xianghe Investment for 540 million yuan ($74.7 million) and Shimao Group shares fell as much as 12% in Hong Kong after China Construction Bank filed a winding-up petition against the company.

- (Bloomberg) Chinese Brokerages Lower Rate on Margin Deposits, Newspaper Says (See link)

- (Bloomberg) CHINA PREVIEW: CPI to Pull Back to 0.3% as Holiday Demand Fades (see link)

- (Bloomberg) Chinese EV Stocks Rise as EV Penetration Recovers in April (see link)

- Looking ahead, Focus is on China CPI Thursday

ASIA PAC EQUITIES: Asian Equities Mixed As Japanese Equities Head Lower Ahead Of US CPI

Regional Asian equities are mixed on Wednesday, US equity futures are unchanged as we await inflation data due out later today. In local markets the MSCI APAC Index is on track for the third day of gains as HK equities offset losses in Japanese equities. Apart from The RBNZ decision, where they kept rates on hold, the calendar has been very quiet. Markets are closed in South Korea, Singapore, Indonesia, Malaysia and the Philippines.

- Japan equities opened lower on Wednesday with investors expected to take a wait-and-see stance ahead of the release of US inflation data. BoJ Governor Kazuo Ueda made comments Tuesday that suggested he is keeping his options open for a further paring back of monetary easing, he also spoke earlier this morning where he mentioned the BoJ owns about 7% of the entire Japanese stock market and that deciding the fate of ETF holdings will be a difficult task while also noting a potential increase in bond buying if yields rise sharply and is cautious about directly responding to FX movements but suggests a potential policy shift if FX movements risk pushing inflation above expectations. While Microsoft will invest $2.9 billion over the next two years to boost its hyperscale cloud computing and artificial intelligence infrastructure in Japan, marking its biggest investment in the country. The Nikkei 225 index dropped 0.38% to 39,924 while the broader Topix Index slipped 0.27%, to 2,747.

- Taiwanese equities saw a $500m inflow from foreign investors on Tuesday, while equities surged. Equities are unchanged on Wednesday, as investors await US inflation data later today, while late on Tuesday CPI released which missed estimates, the March print came in at 2.14% vs 2.50% show a decent drop from the Feb where CPI was 3.08%.

- Australian equities have opened higher with the ASX 200 up 0.27% marking the third day of gains. Miners, Health care and Real Estate names are the top performing sectors with Financials and Tech stocks the worst sectors.

- Elsewhere in SEA, New Zealand equities are up 0.15% with little reaction to the RBNZ decision to keep rates on hold. Thailand equities are up 0.44%, Indian equities are up 0.25%

ASIA EQUITY FLOWS: Asian Tech See Inflows, Thai Inflows Surge Ahead Of BoT Decision

- China equities were mixed on Tuesday, there was little in the way of market headlines or economic data. The large cap indices closed largely unchanged, while small-cap and growth indices close up over 1%. Flows via northbound connect turned positive on Tuesday with inflows of 1.1b yuan, while flows over the past week remain negative. The 5-day average is now at -0.7b, vs the 20-day average at 1.4b above the 100-day average at 0.47b yuan.

- Taiwan reversed Monday's $500m outflow, with a $550m inflow on Tuesday the largest inflow since early March, while equities surging higher to close the day up 1.85%. Taiwan CPI missed expectations coming in at 2.14%, vs 2.50% estimated. The 5-day average is now -$22m, 20-day average is now -$195m while the longer term 100-day average is $168m

- South Korean equities had $211m of foreign investor inflows now marking 13 of the past 15 trading session of inflows, and now still well above other regional markets in terms of flows. The kospi close down 0.46%, while the 5-day average is now $114m, the 20-day average is $255m above the longer term 100-day average at $187m.

- Thailand saw the largest inflow since Feb 21 and the second largest inflow 29 Dec 2022, ahead of the BoT rate decision later today, the SET closed up 1.86%, The 5-day average is $38m, vs the 20-day average at -$38m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 1.1 | -3.5 | 62.3 |

| South Korea (USDmn) | 212 | 572 | 13584 |

| Taiwan (USDmn) | 551 | -111 | 4619 |

| India (USDmn)** | 0 | -92 | 1267 |

| Indonesia (USDmn) ** | 0 | -584 | 1102 |

| Thailand (USDmn) | 166 | 192 | -1717 |

| Malaysia (USDmn) *** | -12 | -62 | -270 |

| Philippines (USDmn) *** | -16 | -33.7 | 137 |

| Total (Ex China USDmn) | 900 | -118 | 18722 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Apr 5th | |||

| *** Data Up To Apr 8th |

OIL: Holding Tuesday Losses Ahead Of Key US Event Risks

Brent crude sits close to unchanged in the first part of Wednesday dealing. We were last close to $89.45/bbl, just up from end Tuesday levels in NY. It's a similar backdrop for WTI, with the front month contract near $85.30/bbl. This follows falls in Tuesday trade of a little over 1% for both benchmarks.

- BBG noted that industry sources are pointing to a rise in US oil inventories, with official data due for release during Wednesday US trade. This has taken some of the gloss of the recent rally in crude, albeit at the margins.

- Elsewhere, Iran’s Islamic Revolutionary Guard Corps naval forces said that Iran is choosing not to disrupt flows through the Strait of Hormuz in the Persian Gulf.

- Also, world oil demand growth for 2024 has been revised down by 480k b/d to 0.95m b/d in the EIA’s Short-Term Energy Outlook.

- These developments may have also seen some tempering of bullish sentiment, particularly ahead of the US CPI and FOMC Mins due later.

- Not much has changed from a technical standpoint though, for WTI the next objective is $89.08, a Fibonacci projection. On the downside, initial firm support to watch lies at $82.80, the 20-day.

GOLD: Winning Run Continues Ahead Of US CPI & FOMC Minutes

Spot gold reached a new high ($2365.35) on Tuesday, before closing 0.6% higher at $2352.78, as demand remained strong ahead of tomorrow’s US data. Bullion is little changed so far in the Asia-Pac session.

- Tuesday’s move was supported by lower US Treasury yields ahead of today’s US CPI & FOMC Minutes. (See MNI U.S. CPI Preview: Apr 2024 - Key Framing Of Trends With June Cut Seen As A Coin Toss here)

- According to MNI’s technicals team, the next objective is $2376.5, a Fibonacci projection. Initial firm support is at $2222.4, the 20-day EMA.

- (AFR) One of the reasons for their price strength is that investors are increasingly using gold and oil to hedge against economic uncertainty and geopolitical tensions. So far, the rally in the precious metal has been mainly driven by central bank buying, particularly by the People’s Bank of China. (See link)

ASIA FX: CNH Shrugs Off Ratings Outlook Shift, BoT Decision Still To Come

The USD is seeing a slightly softer tone against Asian currencies, although overall moves have been modest. TWD and KRW have outperformed, although for the won this has been in the 1 month NDF space (with onshore markets shut). CNH hasn't been impacted by the Fitch ratings outlook downgrade. THB is slightly firmer ahead of the upcoming BoT decision, while details of the digital wallet scheme have been released. Tomorrow the focus will rest on China's CPI and PPI prints.

- USD/CNH has largely tracked close to the 7.2400 level, little changed for the session. Spot USD/CNY is a little lower last near 7.2300. Fitch downgraded the ratings outlook for China, citing the steady rise in debt levels. The announcement hasn't impacted the yuan, while local equities remain in the red, although we were already down prior to the ratings headlines crossing.

- 1 month USD/KRW is down around 0.30%, last near 1346.5. Onshore markets are closed today for general assembly elections. We don't expect the election outcomes will have a large impact on market sentiment, although Yoon's policy agenda may be impacted. KRW has likely been aided at the margin by better HK tech equity trends (local markets in Seoul have been closed due to the election).

- USD/TWD has weakened in the first part of Wednesday trade. Spot is back to 32.00, a TWD gain of around 0.35% so far (earlier lows were around 31.95). Recent highs in the pair rest at 32.12. Over the past month we have risen from the low 31.40 region, with dips supported. The 20-day EMA sits back near 31.89. Today's pull back may reflect some position squaring ahead of the upcoming US CPI release (per BBG). Yesterday net equity inflows from offshore investors were quite strong, +$551mn, although April to date is still running at a negative in terms of this investor segment. Coming up later we have March trade figures. The market looks for an improved trend to 7.5% for export growth.

- For the baht, focus will rest on the upcoming BoT decision. No change is expected by the consensus although the prior meeting did see some BoT board members calling for a cut, hence some sell-side names see risks of a cut at today's policy meeting. USD/THB was last near 36.315, slightly lower for the session. Details of the government's digital wallet scheme have been filtering out this afternoon. PM Srettha believes the scheme, which will be rolled out in Q4 of this year, will boost growth by 1.2% to 1.6%. The MOF believes the scheme will also help the economy grow by nearly 5% in 2025. Note recent growth outcomes have been around the 2% level.

CHINA CREDIT RATING: Fitch Revises China Outlook To Negative

Fitch has revised China's long term issuer default rating outlook to negative. The current rating was maintained at A+.

- Fitch noted the following, which prompted the shift in the outlook: "The revision reflects increasing risks to China’s public finance outlook as the country contends with more uncertain economic prospects amid a transition away from property-reliant growth to what the government views as a more sustainable growth model"

- See this BBG link for more details.

THAILAND Digital Wallet Scheme To Be Rolled Out In Q4, Funding Through The Budget

Details of the government's digital wallet scheme have been filtering out this afternoon. PM Srettha believes the scheme, which will be rolled out in Q4 of this year, will boost growth by 1.2% to 1.6%. The MOF believes the scheme will also help the economy grow by nearly 5% in 2025. Note recent growth outcomes have been around the 2% level.

- Under the plan, 50 million Thai adults will be given 10,000 baht. The 500bn baht (14bn USD) scheme will be financed through the state budget, with 175b from this year's budget and 152bn from next year's budget. The remainder will come from money that was slated for the state owned Bank for Agriculture (see this BBG link for more details).

- Earlier plans had indicated the program would be funded by fresh borrowings.

- The market reaction hasn't been large so far. USD/THB is relative steady, last in the 36.30/35 region. We do have the BoT decision later, where some in the market are calling for a rate cut. Thailand equities are up around 0.50%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/04/2024 | 0600/0800 | ** |  | SE | Private Sector Production m/m |

| 10/04/2024 | 0600/0800 | *** |  | NO | CPI Norway |

| 10/04/2024 | 0800/1000 | * |  | IT | Retail Sales |

| 10/04/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 10/04/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 10/04/2024 | - | *** |  | CN | Money Supply |

| 10/04/2024 | - | *** | | CN | New Loans |

| 10/04/2024 | - | *** | | CN | Social Financing |

| 10/04/2024 | 1230/0830 | *** | | US | CPI |

| 10/04/2024 | 1230/0830 | * |  | CA | Building Permits |

| 10/04/2024 | 1345/0945 | | CA | BOC Monetary Policy Report | |

| 10/04/2024 | 1345/0945 | *** | | CA | Bank of Canada Policy Decision |

| 10/04/2024 | 1400/1000 | ** | | US | Wholesale Trade |

| 10/04/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 10/04/2024 | 1430/1030 | | CA | BOC Governor Press Conference | |

| 10/04/2024 | 1645/1245 | | US | Chicago Fed's Austan Goolsbee | |

| 10/04/2024 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 10/04/2024 | 1800/1400 | ** | | US | Treasury Budget |

| 10/04/2024 | 1800/1400 | *** | | US | FOMC Minutes from March meet |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.