Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

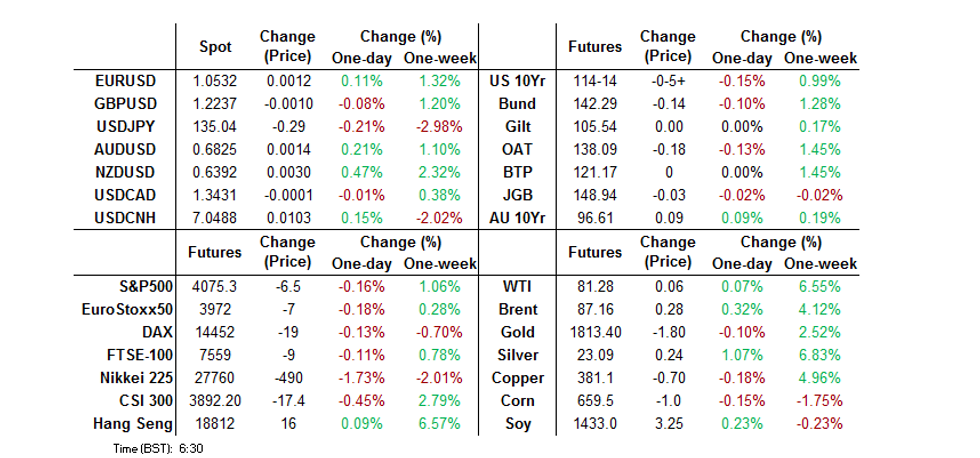

- Tsys cheapened in Asia-Pac dealing, with the aforementioned move lower in JGB futures, on the back of speculation surrounding a BoJ policy review, building on an early regional willingness to fade Thursday’s rally.

- The major USD indices are close to steady so far for the session. We did see a brief move higher earlier, as UST yields rose, but this had little follow through.

- Coming up, we have some Fed & ECB speak, along with the EU PPI. Canada labour force data prints, while the main focus will be on the US non-farm payrolls outcome.

US: MNI Payrolls Preview: Watching Implications For Feb FOMC

EXECUTIVE SUMMARY

- Consensus is very similar to what it pencilled in for last month’s report, before payrolls came in stronger but the u/e rate increased more than expected as participation fell.

- As it is, payrolls growth is seen continuing to moderate but well above a more sustainable 100k with the u/e rate holding at a low 3.7% (slight survey skew lower) and AHE easing to 0.3% M/M (slight skew higher).

- The indicators of slack from the usual combination of unemployment and participation rates plus AHE growth will guide the market reaction.

- The outcome is most likely to affect expectations for the Feb 1 FOMC decision. 50bp is currently seen largely locked in for December (52bp priced), with an additional 35bp priced for the Feb meeting. The recent renewed Fed concentration on the labour market could see this swing either way.

- PLEASE FIND THE FULL REPORT HERE: USNFPDec2022Preview.pdf

US: Primary Dealer NFP Estimates

| Primary Dealer | Estimate | Primary Dealer | Estimate |

| Societe Generale | +270K | Amherst Pierpoint | +240K |

| TD Securities | +240K | Citi | +225K |

| Credit Suisse | +225K | RBC | +220K |

| BNP Paribas | +210K | HSBC | +210K |

| Mizuho | +210K | Scotiabank | +205K |

| BMO | +200K | Daiwa | +200K |

| Deutsche Bank | +200K | UBS | +200K |

| Wells Fargo | +190K | Jefferies | +185K |

| Morgan Stanley | +180K | Nomura | +180K |

| Barclays | +175K | Goldman Sachs | +175K |

| J.P.Morgan | +150K | ||

| Median | +200K | BBG Whisper | +194K |

US TSYS: Cheaper Into NFPs As Asia Fades The Rally & JGBs Soften

Tsys cheapened in Asia-Pac dealing, with the aforementioned move lower in JGB futures, on the back of speculation surrounding a BoJ policy review, building on an early regional willingness to fade Thursday’s rally.

- Cash Tsys sit ~4bp cheaper across the curve as a result, with TYH2 dealing just off the base of its 0-09+ overnight range, last -0-05+ at 114-14.

- Flow of note included a block seller of TY futures (-1,250) & a block buyer of FV futures (+1.6K).

- Focus continues to fall on the well-documented growth headwinds for the Chinese economy, although the daily new COVID case count in the country extended the moderation from the record highs seen earlier this week, albeit at a slow pace.

- A reminder that Thursday saw a further reduction in rate hike premium embedded into Fed dated OIS, with ~51bp of tightening now priced for this month’s meeting & a terminal rate of ~4.85% now eyed.

- NY hours will be headlined by the latest NFP print (see our full preview of that event here). Fedspeak from Barkin & Evans (with the latter soon to depart his post) will supplement that data release.

JGBS: Futures Pressured By BoJ Review Talk, Curve Twist Flattens

Friday’s focus has squarely fallen on comments from BoJ board member Tamura , who has called for a review of the BoJ’s monetary policy framework.

- Tamura stressed that the move “should come at the right time” and was non-committal re: the potential for policy tweaks post-review, pointing to situations whereby tweaks may or may not be required.

- This was the second such instance of tweak discussion in 2 days after BoJ board member Noguchi pointed to a data-dependent stance, albeit with no expectations of policy tweaks in the immediate term, alongside a need for continued monetary easing on Thursday.

- This dominated any secondary headline flow, with a below-/in-line-with-average round of offer/cover ratios at the latest round of BoJ Rinban operations noted, perhaps supporting the longer end of the curve.

- JGB futures are -11 into the bell as a result, more than unwinding their overnight bid. The curve has twist flattened, pivoting around 10s, with the major benchmarks sitting 1bp cheaper to 2bp richer, as 7s lead the weakness owing to the cheapening in futures.

- Elsewhere, BoJ Deputy Governor Amamiya outlined the BoJ’s accounting framework re: JGB holdings in front of parliament, while stressing that any paper losses incurred on its holdings will not impact the Bank’s ability to conduct monetary policy.

- We also heard from BoJ Governor Kuroda, who reiterated already heavily-discussed points re: the Japanese economic outlook.

- There isn’t much of note on the domestic docket on Monday.

AUSSIE BONDS: Firmer And Flatter On Thursday Spill Over

Aussie bonds remained underpinned on Friday, even with the likes of JGBs and U.S. Tsys cheapening as the day wore on.

- Onshore participants were more attuned to catching up to Thursday’s rally in U.S. Tsys than the aforementioned dynamics observed in the remainder of the core FI sphere, with dips bought. That allowed YM & XM to extend through and close above their respective overnight highs, with the former +7.0 & the latter +9.0. Cash ACGBs were 6-12bp richer as the curve bull flattened.

- Bills were 1-11bp richer through the reds, with flattening also in play there.

- In terms of domestic headline flow, RBA Governor Lowe largely went over old ground on inflation expectations and the resilience of domestic consumers. He also flagged the potential for a more elongated than usual round of delayed pass through from monetary tightening into the economy, highlighting this as a key point re: the RBA’s recent step down in the pace of tightening.

- ACGB Sep-26 supply was well received.

- Looking ahead, Monday’s docket includes final services & composite PMI from S&P Global, Melbourne Institute inflation metrics and another round of Q3 GDP partials.

- The latest RBA decision (Tuesday) & Q3 GDP print proper (Wednesday) headline next week’s domestic docket. 19bp of tightening is priced into dated OIS for next week’s meeting, with a terminal cash rate of 3.60% eyed, in a touch on the day.

NZGBS: Receiver Side Swap Flow & Move Lower In RBNZ Dated OIS Helps Early Bid Extend

NZGBs looked more to the extension in ACGBs than the light cheapening in U.S. Tsys during Friday trade, extending on the early richening that was inspired by the move in U.S. Tsys on Thursday, after the space initially lagged Thursday’s rally in Tsys. That left the major benchmarks running 9-10bp richer at the bell, while swaps were 9-11bp richer, leaving swap spreads little changed to a touch tighter as the swap curve flattened.

- RBNZ dated OIS was little changed to a touch lower in lieu of Thursday’s move in market pricing re the U.S. Fed, with 61bp of tightening now priced for the first RBNZ meeting of ’23, while terminal OCR pricing hovers around 5.30%. This aided the bid in NZGBS.

- Domestically, terms of trade data printed much softer than expected, with the headline index seeing a ‘surprise’ fall.

- Governor Orr will take part in a BIS panel discussion late on Friday, although the topic of “A Digitalised Monetary System in the Making” should limit the scope for comments on meaningful monetary policy issues.

- Further out, Q3 manufacturing activity and monthly card spending data headline next week’s domestic docket, with NZGBs set to adjust to the impending U.S. NFP print at Monday’s open.

FOREX: USD Holds Steady Ahead Of NFP Print

The major USD indices are close to steady so far for the session. We did see a brief move higher earlier, as UST yields rose, but this had little follow through. The BBDXY sits at 1257.40 currently.

- As has been the case for much of the week, JPY and NZD have remained on the front foot. NZD/USD is up a further 0.33% for the session so far, this puts us back above 0.6380, although we are still below overnight highs of 0.6400. A downside terms of trade surprise did little to impact sentiment.

- USD/JPY hasn't been able to break below 135.00, but the earlier move above 135.50 was sold into. This comes despite UST yields holding higher levels for much of the session. Bloomberg reports that Japan lifers may be raising offshore asset hedge ratios, which would naturally benefit the yen.

- AUD/USD is back to 0.6815, but is still tracking recent ranges. Housing finance data was close to expectations, while RBA Governor Lowe reiterated recent comments in a panel session in Thailand.

- Coming up, we have some ECB speak, along with the EU PPI. Canada labour force data prints, while the main focus will be on the US non-farm payrolls outcome. Fed's Barkin is also due to speak.

ASIA FX: South East Asia FX Outperforms On UST Real Yield Pullback

The bias for most USD/Asia pairs remains skewed to the downside. South East Asian FX has outperformed today, likely on account of catch-up with the overnight sharp pullback in UST real yields. There has been some recovery in nominal UST yields today, along with a weaker tone in equity markets, but this hasn't impacted regional FX sentiment a great deal. On Monday, the China Caixin services PMI prints, along with South Korean FX reserves.

- USD/CNH has continued to track recent ranges, last sitting around 7.05. The CNY fixing was close to neutral once again, while China equities are generally trading on the soft side.

- USD/KRW 1 month hasn't made fresh lows, last close to 1300. Onshore equities are down 1.6% at this stage, while offshore investors have sold in excess of $300mn of local shares. Earlier November CPI came in softer for the headline but core pressures remain sticky at 4.8% y/y.

- USD/THB continues to track lower, spot last under 34.80, fresh cyclical lows back to June for the pair. Some of this is likely catch up with overnight USD weakness, although baht been an outperformer in recent weeks.

- IDR has played some catch up today, the pair last around 15430, up from earlier lows near 15400, but still +0.85% firmer for the session in IDR terms. The BI Governor stated inflation expectations are coming down and the core inflation trend remains fairly benign.

- USD/PHP is back under 56.00, with the peso around +0.50% stronger for the session so far. The BSP Governor stated that the board is likely to consider a 25bps or 50bps move at the mid-December policy meeting. Tuesday's inflation data could dictate how much the BSP tightens by. A 2.3% pullback in Philippines' equities hasn't impacted FX sentiment.

EQUITIES: Weakness Across The Board After Recent Strong Gains

Asia Pac equities are seeing some consolidation after recent strong gains. Weakness is evident across all the major indices. US futures are also down, -0.20/-0.30% at this stage, after an indifferent overnight session. Higher UST yields (+3bps or so across the curve) is likely contributing to today's weakness.

- China stocks are off by 0.50% for the CSI 300, while the Shanghai Composite is 0.25% lower. Hong Kong stocks tried to push higher, but the HSI is now down around 0.8% or so, with banks and property companies weighing.

- Japan stocks are down 1.70% in terms of the Nikkei, as a firmer yen (near 135.00) weighs on the export segment. The Kospi has retraced by 1.45%, as foreigners sell local stocks ($-334.mn in net outflows at this stage). The Taiex is holding up better, just off 0.20% at this stage.

- In South East Asia, the Philippines bourse is the worst performer, down 2.3%.

GOLD: Dips Following Break Above $1800

Gold has slipped back below the $1800 level, last tracking around $1796. This is -0.40% below NY closing levels. Dollar indices are broadly unchanged so far today, so the precious metal is underperforming slightly. Still, cumulative gains over the past 3 sessions were in excess of 3.5%, so some profit taking flows may be in play.

- Today's slightly firmer UST yield backdrop (2yr +3.5bps to 4.26%), is likely encouraging some profit taking flows as well.

- From a technical standpoint, we currently sit near the simple 200-day MA for gold, which comes in at $1796.26. A close above this level at the end of this week is likely to maintain a bullish outlook for the metal.

- A move towards June highs around $1880 is a possible medium term target, while on the downside, mid November highs close to $1786.50 may act as a support point.

OIL: On Track For A Solid Weekly Gain Ahead Of Weekend OPEC+ Meeting

Brent crude is holding close to $87/bbl, slightly up on NY closing levels. At this stage we are sitting at a gain for the week near 4%, the best since early October. WTI sits at $81.20/bbl, tracking an more impressive +6.44% for the week.

- Optimism around an improved demand outlook from China going forward has been a key drive of sentiment this past week. We remain below key moving average levels for Brent, but we need to clear overnight highs (near $89.40/bbl) and then we can target $91.48/bbl, the 50 day MA.

- Looking ahead the weekend focus will be the OPEC+ meeting on Sunday. While there has been some discussion of potential further supply cuts, sell-side analysts see the status quo being maintained as the most likely outcome.

- The G7 is also reportedly close to an agreement on a $60/bbl oil price cap for Russian exports. This comes ahead of Monday's EU oil import ban on Russian crude oil imports (via sea trade).

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/12/2022 | 0700/0800 | ** |  | DE | Trade Balance |

| 02/12/2022 | 1000/1100 | ** |  | EU | PPI |

| 02/12/2022 | 1200/1300 | | EU | ECB de Guindos Speech at OK Diario Event | |

| 02/12/2022 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 02/12/2022 | 1330/0830 | * | | CA | Production Estimate of Principal Field Crops |

| 02/12/2022 | 1330/0830 | *** |  | US | Employment Report |

| 02/12/2022 | 1415/0915 | | US | Richmond Fed's Tom Barkin | |

| 03/12/2022 | 0230/0330 | | EU | ECB Lagarde at Bank of Thailand Roundtable | |

| 05/12/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

| 05/12/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Services PMI |

| 05/12/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 05/12/2022 | 0145/0245 | | EU | ECB Lagarde Speech on Green Economy | |

| 05/12/2022 | 0700/0200 | * |  | TR | Turkey CPI |

| 05/12/2022 | 0745/0845 | * |  | FR | Industrial Production |

| 05/12/2022 | 0815/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 05/12/2022 | 0845/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 05/12/2022 | 0850/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 05/12/2022 | 0855/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 05/12/2022 | 0900/1000 | ** | | EU | IHS Markit Services PMI (f) |

| 05/12/2022 | 0930/1030 | * | | EU | Sentix Economic Index |

| 05/12/2022 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Services PMI (Final) |

| 05/12/2022 | 1000/1100 | ** | | EU | retail sales |

| 05/12/2022 | - | | EU | ECB Panetta at Eurogroup Meeting | |

| 05/12/2022 | 1330/0830 | * | | CA | Building Permits |

| 05/12/2022 | 1445/0945 | *** | | US | IHS Markit Services Index (final) |

| 05/12/2022 | 1500/1000 | *** | | US | ISM Non-Manufacturing Index |

| 05/12/2022 | 1500/1000 | ** | | US | factory new orders |

| 06/12/2022 | 0001/0001 | * | | UK | BRC-KPMG Shop Sales Monitor |

| 06/12/2022 | 0330/1430 | *** | | AU | RBA Rate Decision |

| 06/12/2022 | 0700/0800 | ** | | DE | Manufacturing Orders |

| 06/12/2022 | 0830/0930 | ** | | EU | IHS Markit Final Eurozone Construction PMI |

| 06/12/2022 | 0830/0930 | | DE | S&P Global Germany Construction PMI | |

| 06/12/2022 | 0930/0930 | | UK | S&P Global/CIPS UK Construction PMI | |

| 06/12/2022 | 0930/0930 | ** | | UK | IHS Markit/CIPS Construction PMI |

| 06/12/2022 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 06/12/2022 | 1130/1130 | ** | | UK | Gilt Outright Auction Result |

| 06/12/2022 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 06/12/2022 | 1330/0830 | ** | | US | Trade Balance |

| 06/12/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 06/12/2022 | 1400/1500 | | EU | ECB Publication of Monthly APP/PEPP update | |

| 06/12/2022 | 1500/1000 | * | | CA | Ivey PMI |

| 07/12/2022 | 0430/1000 |  | IN | India RBI Rate Decision | |

| 07/12/2022 | 0645/0745 | ** |  | CH | Unemployment |

| 07/12/2022 | 0700/0800 | ** | | DE | Industrial Production |

| 07/12/2022 | 0700/0800 | *** |  | SE | GDP |

| 07/12/2022 | 0700/0800 | ** | | SE | Private Sector Production |

| 07/12/2022 | 0710/0810 | | EU | ECB Lane Speech at China FX Global Perspective | |

| 07/12/2022 | 0745/0845 | * | | FR | Foreign Trade |

| 07/12/2022 | 0745/0845 | * | | FR | Current Account |

| 07/12/2022 | 0900/1000 | * | | IT | Retail Sales |

| 07/12/2022 | 1000/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 07/12/2022 | 1000/1100 | * | | EU | Employment |

| 07/12/2022 | 1000/1100 | *** | | EU | GDP (final) |

| 07/12/2022 | 1200/0700 | ** | | US | MBA Weekly Applications Index |

| 07/12/2022 | - | *** | | CN | Trade |

| 07/12/2022 | 1300/1400 | | EU | ECB Panetta Speech at at LBS-AQR Insight Summit | |

| 07/12/2022 | 1330/0830 | ** | | US | Non-Farm Productivity (f) |

| 07/12/2022 | 1500/1000 | *** | | CA | Bank of Canada Policy Decision |

| 07/12/2022 | 1530/1030 | ** | | US | DOE weekly crude oil stocks |

| 07/12/2022 | 2000/1500 | * | | US | Consumer Credit |

| 08/12/2022 | 0001/0001 | | UK | RICS House Price Balance | |

| 08/12/2022 | 1200/1300 | | EU | ECB Lagarde Intro at European Systemic Risk Board Conf | |

| 08/12/2022 | 1330/0830 | ** | | US | Jobless Claims |

| 08/12/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 08/12/2022 | 1500/1000 | * | | US | Services Revenues |

| 08/12/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 08/12/2022 | 1730/1230 | | CA | BOC Deputy Kozicki speech |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.