- With Japan markets out today, we have seen no US cash Tsy trading. Futures have been biased lower, but remain within ranges from late last week. The USD is mixed, higher against the safe havens, but softer against higher beta plays.

- Regional equity sentiment has been positive, in part helped by a cut to the 14-day reverse repo rate in China. Whilst this is largely a catch up move it is seen as supporting the policy bias, something which the PBoC Governor stated would intensify from a monetary policy standpoint.

- Looking ahead on the data front, we have EU and US September preliminary PMIs are released. The Fed’s Bostic, Goolsbee and Kashkari also speak.

MARKETS

US TSYS: Futures Weaker, No Cash Trading Due To Japan Holiday

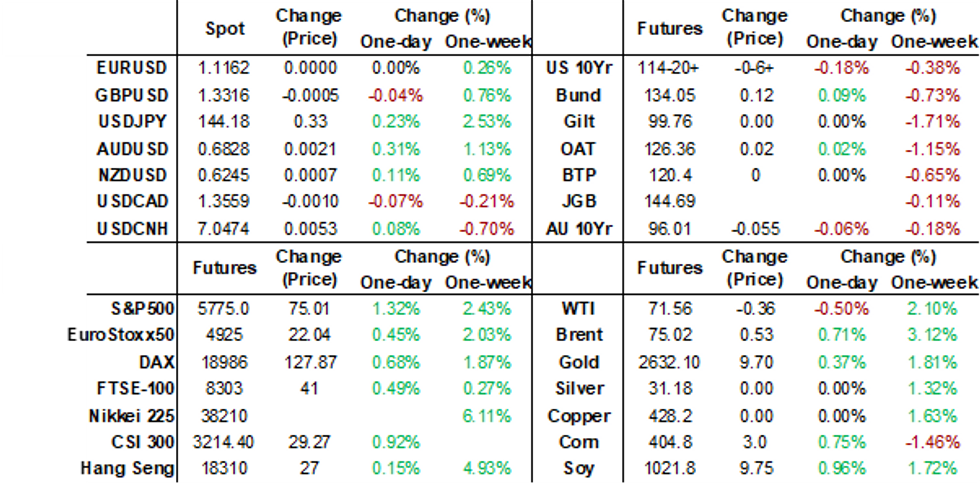

TYZ4 is trading at 114-20, -0-07 from NY closing levels.

- There has been no cash trading for US tsys in today's Asia-Pac session due to a holiday in Japan.

- Newsflow has also been light so far today, leaving Asia-Pac market participants to digest Friday’s conflicting Fedspeak.

- Fed Governor Bowman (voter) issued a statement on Friday explaining why she dissented against the FOMC’s decision to cut the Fed Funds target range by 50bps last Wednesday. Her comments were in contrast to Governor Waller’s remarks in a CNBC interview, which were concerned with risks of inflation undershooting.

- Projected rate cuts into early 2025 bounced off early session lows on Friday, with the latest vs. late Thursday levels (*) as follows: Nov'24 cumulative -37.8bp (-35.9bp), Dec'24 -75.0bp (-72.4bp), Jan'25 -108.5bp (-106.5bp).

- Looking ahead to today’s US calendar, we will see more Fedspeak from Bostic, Goolsbee and Kashkari, alongside data including flash PMI data from S&P Global.

AUSSIE BONDS: Subdued Start To A Busy Week, RBA Tomorrow, CPI On Wednesday

ACGBs (YM -4.0 & XM -5.0) are weaker after dealing in narrow ranges in today’s Sydney session. Without cash US tsy dealing in today's Asia-Pac session due to a holiday in Japan, the local market has traded without conviction.

- TYZ4 currently deals at 114-20+, -0-06+ from Friday’s closing levels.

- The RBA's Policy Decision is due tomorrow, with Bloomberg consensus unanimous in expecting a no-change outcome.

- Following the decision and statement at 1430 AEST, RBA Governor Bullock will hold a press conference at 1530 AEST. She last spoke on September 5 and since then survey data have been soft but labour market and lending data strong. So, we don’t expect that the Board has changed its view that it is too soon to discuss rate cuts.

- August CPI is released on Wednesday with the headline forecast to moderate to 2.7% from 3.5% driven by federal government electricity subsidies. The trimmed mean will be the focus (3.8% in July).

- Cash ACGBs are 4bps cheaper.

- Swap rates are 4bps higher.

- The bills strip has bear-steepened, with pricing -4 to -6.

- RBA-dated OIS pricing is 2-5bps firmer across 2025 meetings. A cumulative 15bps of easing is priced by year-end.

STIR: RBA Dated OIS Year-End Easing Pared Ahead Of RBA Decision

Ahead of tomorrow’s RBA Policy Decision, RBA-dated OIS pricing is 2-5bps firmer across 2025 meetings, with a cumulative 15bps of easing priced by year-end.

- Australia stands out within the $-bloc in terms of year-end official rate expectations, with rates firming over the past ten days.

- Meanwhile, in the rest of the $-bloc, year-end rate expectations have softened by 19bps in the US, 12bps in Canada, and 5bps in New Zealand.

- The latest setback for easing expectations in Australia came after Thursday’s Employment Report for August surprised on the upside, with employment rising by 47k m/m versus the 26k estimate.

- The December 2024 expectations and the cumulative easing across the $-bloc are as follows: 4.14%, -94bps (FOMC); 3.53%, -72bps (BoC); 4.17%, -16bps (RBA); and 4.42%, -83bps (RBNZ).

Figure 1: Official Rate: Current Vs. Year-End Market Expectations

Source: MNI – Market News / Bloomberg

NZGBS: Closed Cheaper, Subdued Session, Light Local Calendar

NZGBs closed 1-4bps cheaper after a relatively subdued session. There has been no cash trading for US tsys in today's Asia-Pac session due to a holiday in Japan. TYZ4 currently deals at 114-20+, -0-06+ from Friday’s closing levels.

- Outside of the previously outlined Job Ads data, there hasn't been much by way of domestic drivers to flag. It is a reasonably quiet week for NZ, with Friday’s ANZ Consumer Confidence data as the highlight.

- Across the ditch, the RBA Policy Decision is due tomorrow, with Bloomberg consensus unanimous in expecting a no-change outcome.

- Swap rates closed flat to 4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed. A cumulative 83bps of easing is priced by year-end.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond, NZ$225mn of the 4.50% May-35 bond and NZ$25mn of the 2.75% Apr-37 bond.

FOREX: Safe Havens Down, A$ Firms On Regional Equity Gains Post China Repo Cut

Safe havens have lost ground in the first part of Monday trade, while the AUD has outperformed. The BBDXY and DXY USD indices sit little changed. Yen is off around 0.25%, while CHF is down by a little over 0.10%.

- The backdrop from a regional equity market standpoint has been positive, with most major markets higher at this stage. China related sentiment has been supported by a 10bps cut to 14 day repo rate. This is not a widely used benchmark but may signal further policy easing is coming. A press conference will be held tomorrow, where the PBoC Governor will be in attendance.

- US equity futures are also firmer higher, up 0.30% for Eminis and nearly 0.60% for Nasdaq futures.

- This has likely helped AUD/USD, which is the outperformer in the G10 space, up 0.35% to 0.6835. Recent highs at 0.6839 are very close by. Late December 2023 levels rested just above 0.6870.

- We had earlier preliminary PMI data in Australia, for September, but sentiment wasn't shifted. NZ's trade deficit widened in August, but didn't impact NZD much. NZD/USD was last a touch higher at 0.6240/45. The AUD/NZD cross is close to recent highs, last near 1.0940/45.

- USD/JPY got close to Friday highs (144.49) but ran out of steam at 144.46, the pair last near 144.25, still 0.25% weaker in yen terms. Japan markets have been out today, so no cash Tsy trading has taken place. US 10yr futures have edged down but remain within Friday's ranges.

- Commodities have been mixed, with oil up on the China news and continued geopolitical tensions. Iron ore is softer but hasn't impacted AUD.

- Looking ahead on the data front, we have EU and US September preliminary PMIs are released. The Fed’s Bostic, Goolsbee and Kashkari also speak.

FOREX: Short AUD Positions Built Ahead of Last Week's FOMC

CFTC positioning data generally saw shifts towards the USD in the lead up to last week's Fed announcement. The table below outlines the weekly change and outright positions across leveraged investors and asset managers. This data is the for the week ending the 17th of September (so last Tuesday).

- By currency, in the leveraged space, we saw extension of shorts against the USD, for JPY and AUD, while GBP longs were cut back noticeably. CAD shorts were added to as well.

- For asset managers the modest yen long was added to, but EUR and GBP longs were cut. GBP/USD's position for asset managers is almost back to flat. AUD/USD shorts were added to in a decent size as well.

Table 1: CFTC FX Positioning Data As At End Sep 17 2024

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -1208 | -15780 | 2073 | 29992 |

| EUR | -7109 | 5718 | -12289 | 306139 |

| GBP | -10965 | 45659 | -15456 | 552 |

| AUD | -8513 | -17115 | -22106 | -34143 |

| NZD | 2536 | 4143 | 3183 | -1205 |

| CAD | -6796 | -51618 | -4268 | -77769 |

| CHF | 1221 | -2902 | 6117 | -18165 |

| MXN | -1313 | -12094 | 5400 | 40828 |

Source: CFTC/MNI - Market News/Bloomberg

CHINA STOCKS: Strong Start to the Week Ahead of Next Week’s Holidays

- China and Hong equity markets are starting the week on a positive note following on from last week’s shortened week.

- The Shanghai Composite finished the week +1.21% higher with only three days of trading.

- This morning the Shanghai composite is up 0.43% in early trade.

- The PBOC announced the reduction in the interest rate for the 14-day repo rate ahead of next week’s holidays.

- Whilst not as widely used, the reduction in the 14-day is seen as a timely reminder of authorities’ willingness to alter policy to support the economy and the Monday’ rally in part is due to expectations that today’s policy changes are potentially a sign of more to come.

- The other focus point remains on domestic calls for further economic stimulus. See our onshore China press briefing for more details.

- Across in Hong Kong, the Hang Seng too had a strong week last week, up 5.12% as investors digested the HKMA’s first cut in rates in four years.

- The Hang Seng too is opening strong Monday, up 0.41% in morning trade as investors take a positive view on last week’s monetary policy decisions ahead of National Day Holidays next week.

ASIA STOCKS: Signs of Strength, with South East Asia Lagging.

- Asian stocks started the week strongly after the PBOC reduced the interest rate on a lesser used liquidity tool.

- The 14-day repo rate is in place to support the daily used 7-day repo rate in the event of holidays.

- With the upcoming National Day Holidays, the 14-day rate was reduced following July’s cut of the 7-day rate.

- For many regional equity investors this was a sign of things to come that the PBOC is willing to support the ailing Chinese economy and that the potential for further stimulus remains.

- In India, data shows that net foreign purchases this quarter are the strongest they have been since 2023, unsurprisingly given the outlook for GDP growth.

- Last week saw investors in India starting to look forward to interest rate cuts from the RBI, buying interest rate sensitive stocks like banks and real estate. Whilst it may be some time off before the RBI cuts rates (given the seasonality expected in September data), the October 9 meeting could put rate cuts in play for the following meeting.

- The Nifty 50 firmed 2.03% last week.

- Trade data out this morning in Korea continues to show that the semi-conductor boom is continuing rising by 26.2% in the first part of September.

- The push pull between the Central Bank and Politicians in the desire to cut rates will be a driving factor for Korea in the coming months.

- Having risen 0.70% last week, the KOSPI is up 0.33%. The relative underperformance of the KOSPI is possibly a reflection of the disparity of views between the BOK and politicians.

- Elsewhere in the region, Malaysia is bucking the trend off -0.25% ahead of its upcoming CPI number and the Jakarta composite is following this trend down 0.36%

OIL: Crude Rallies On China Rate Cut And Rising Geopolitical Tensions

Oil prices are higher today after range trading on Friday driven by escalating geopolitical tensions in the Middle East and China’s 10bp reduction in the 14-day repo rate. WTI rose 0.9% to $71.61/bbl, close to the intraday high, and Brent is up 0.8% to $75.06. The USD index is little changed.

- Oil markets have been concerned about the outlook for China’s economy for some time, as the country is the world’s largest oil importer. Today’s rate cut has buoyed the market though as it signals that the authorities may be prepared to stimulate demand. The Fed’s 50bp rate cut last week may also open the door.

- Israel targeted rocket launchers in southern Lebanon over the weekend after striking Hezbollah leadership in Beirut. Hezbollah fired around 150 rockets and missiles into Israel. The UN has counselled both sides to step back from the brink. Iran supports Hezbollah and there could be risks to oil markets if it were to become more involved in the conflict.

- Later the Fed’s Bostic, Goolsbee and Kashkari speak and preliminary September US/European PMIs are released.

GOLD: Fresh All-Time High After Fed Waller’s Dovish Remarks

Gold is 0.3% higher at a new all-time high of $2631.13 in today’s Asia-Pac session, after closing 1.4% higher on Friday.

- Friday’s move was aided by dovish comments from the Fed’s Waller. Governor Waller expressed concern with inflation undershooting, not overshooting, noting firms' limited pricing power and wage inflation coming down, and that inflation is potentially on a lower path than had previously been expected.

- However, Fed Governor Bowman (voter) issued a statement explaining why she dissented against the FOMC’s decision to cut the Fed Funds target range by 50bps last Wednesday.

- Projected rate cuts into early 2025 bounced off early session lows, latest vs. late Thursday levels (*) as follows: Nov'24 cumulative -37.8bp (-35.9bp), Dec'24 -75.0bp (-72.4bp), Jan'25 -108.5bp (-106.5bp).

- Looking ahead to today’s US calendar we see more Fed speak from Bostic, Goolsbee and Kashkari, alongside data including flash PMI data from S&P Global.

- From a technical perspective, having pierced initial resistance at $2,613.3 on Friday, the next resistance is seen at $2,642.7, the 2.236 projection of the Jul 25 - Aug 2 - Aug 5 price swing.

- Analysts at Quantix Commodities say that although a near-term pull-back in prices is possible, given extreme positioning, the beginning of a Fed easing cycle will undoubtedly be bullish for gold.

CHINA: PBOC Cuts 14-day Repo Rate to 1.85% to Align Policy.

- The lesser used 14-day repo rate was cut from 1.95% to 1.85%.

- Following the cut of the widely used 7-day repo rate in July to 1.7% today is merely a policy adjustment to reflect other policy initiatives.

- The 14-day repo rate is typically only used when the maturity for 7-day repo falls on a holiday.

- Whilst seemingly insignificant, it could amount to an indication that the PBOC is aligning existing policies in anticipation of further moves ahead.

SOUTH KOREA: Export Headline Skewed By September Holidays.

- Korea’s export momentum seasonally adjusted continues to prove the resilience of the economy and challenges those calling for a rate cut.

- Exports when seasonally adjusted rose 18% (whilst non s/a showed contraction of -1.1%).

- September sees Chuseok holidays which results in a large discrepancy for data.

- Consistent with prior releases, semi-conductor shipments continue to drive exports rising 26.2%yoy as Korea positions itself as a key provider in chips in the ongoing trade war between the US and China.

- Whilst spokespeople in the government point to slowing consumer data as a reason to cut rates, the BOK has maintained its focus on the housing market’s growth in Seoul.

- Today’s exports support the BOK’s stance for now, proving that the economy remains robust despite the higher interest rates.

INDIA: PMI’s – Still Expanding.

- HSBC India PMI Manufacturing came in a 56.7 versus 57.5 in August.

- HSBC India PMI Services came in a 58.9 versus 60.9 in August.

- PMI Composite 59.3 versus 60.7.

- Whilst PMI’s are moderating, the pace is very slow and remain well in expansion territory.

- The question now resides with the growth ambitions of the new government. Whilst India growth is on track to outperform its neighbours, is a moderate slowdown of activity enough for the RBI to cut rates.

- With new MPC members, next month’s rate decision remains difficult to judge given no knowledge of the new members bias.

SINGAPORE: CPI and Core Slightly Above Expectations.

- CPI yoy 2.2% versus 2.4% prior and 2.1% survey.

- Core CPI yoy 2.7% versus 2.5% prior.

- Housing +.3.4%.

- A strong number for pricing for Singapore, suggesting that not all of the inflationary pressures have been fallen away both in Singapore and the broader region.

MALAYSIA: CPI Slips Below BNM’s Target

- Malaysia’s CPI slipped to +1.9% you for August, a modest drop from the prior month and estimates.

- Core inflation printed at +1.9% also.

- Within that data, Food and Beverages +1.6%, Housing, Water and Electricity +3.1% and Transport +1.3%.

- Malaysia is forecast to achieve GDP growth of 4.90% in 2024.

- Economic data in Malayia of late has continued to be show a balanced, strong economy.

- Whilst it does not appear that the BNM has been in a rush to cut rates, today’s print likely opens the door to that possibility at their next meeting on November 6th.

ASIA FX: North Asia Currencies Modeslty Weaker Post China 10bps Repo Cut

North Asia currencies are mostly weaker against the USD. Negative spill over from softer yen levels is in play, while a 10bps cut to the 14 day repo rate in China has weighed on CNH at the margins. This has offset a positive tone for local equities.

- USD/CNH found selling interest above 7.0500, post the 10bps cut to the 14 day repo rate. The pair was last near 7.0470. Whilst the 14 day is not a frequently used tool, it does perhaps signal greater policy easing going forward. PBoC Governor Pan was also on the news wires stating that the central bank will intensify monetary policy adjustments. Note tomorrow morning local time we will hear from the Governor as well as from the CSRC and NRFA on financial support for economic development (per BBG). This will be held at 9am local time tomorrow. China equities are higher today, the CSI 300 up 0.70%. Onshore media also continues to discuss the need for stimulus measures to aid the growth outlook.

- Spot USD/KRW has drifted a little higher today, but ran out of steam around the 1337.5 level. We were last under 1336. Earlier data showed weaker headline exports for the first 20-days of September, but after adjusting the day count, it still painted a resilient picture for trade. Export growth in terms of chips and to the US remain the positives.

- Spot USD/TWD is a little higher, but remains under 32.00 at this stage, comfortably off recent highs. The Kospi and Taiex have only posted modest gains today.

CHINA: Bond Wrap

- Ahead of National Holiday’s next week, the PBOC cut the 14-day repo rate by 10bps. The 14-day rate is typically used around holiday times where a 7-day repo would expire.

- The market saw this as potential evidence of further policy moves to come.

- Equity markets were strong again, following last weeks’ rally. Bonds were quiet.

2yr 1.374% 5yr 1.705% 10yr 2.035% (-0.5bp) 30yr 2.150%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/09/2024 | 0645/0845 |  | EU | ECB's Elderson at Real Estate summit | |

| 23/09/2024 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 23/09/2024 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 23/09/2024 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 23/09/2024 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 23/09/2024 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 23/09/2024 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 23/09/2024 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 23/09/2024 | 0830/0930 | *** |  | UK | S&P Global Manufacturing PMI flash |

| 23/09/2024 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 23/09/2024 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 23/09/2024 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 23/09/2024 | 1200/0800 |  | US | Atlanta Fed's Raphael Bostic | |

| 23/09/2024 | 1300/1500 | | EU | ECB's Cipollone statement on digital euro at Hearing | |

| 23/09/2024 | 1345/0945 | *** | | US | S&P Global Manufacturing Index (Flash) |

| 23/09/2024 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 23/09/2024 | 1415/1015 | | US | Chicago Fed's Austan Goolsbee | |

| 23/09/2024 | 1530/1730 | | EU | ECB's Cipollone in panel discussion at House of the euros | |

| 23/09/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 23/09/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 24/09/2024 | - |  | SE | Riksbank Meeting |