Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Yen gains from Tuesday trade have been pared in the first part of Wednesday dealings. We had mixed wages data, solid headline outcomes, but softer same sample base figures for April. JGB futures are sharply higher and at session highs, +41 compared to the settlement levels.

- US Treasury futures have done very little today, ranges have been tight. The better China Caixin services PMI print aided regional risk appetite, but there was no follow through.

- RBA Governor Bullock remained neutral and reiterated the Board’s stance of not “ruling anything or out” and that policy is “restrictive”.

- Later US May ADP employment, final May US & European composite/services PMIs/ISM, euro area April PPI and the Bank of Canada decision are released.

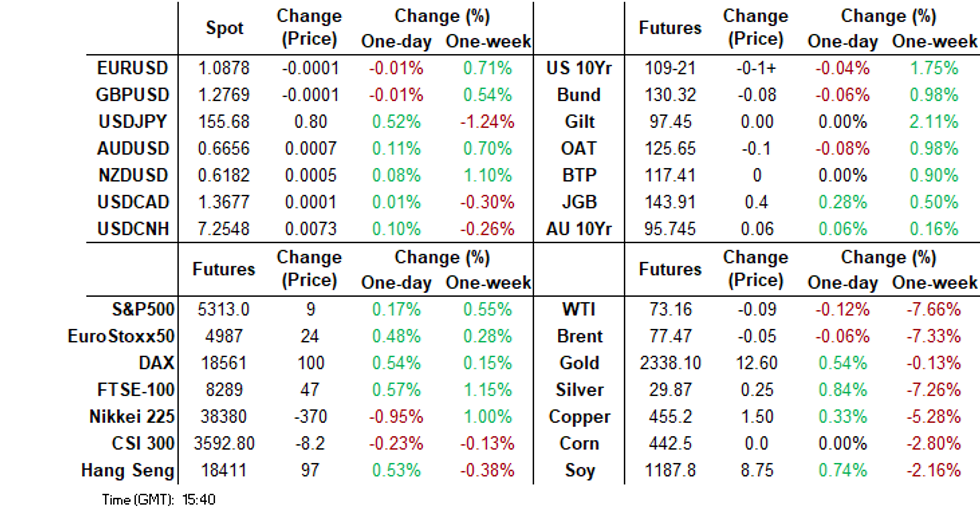

MARKETS

US TSYS: Tsys Futures Off Morning Highs, Ranges Tight Ahead Of ADP Emply Data

- Treasury futures have done very little today, ranges have been tight. TU is trading at 102-02+ vs morning highs of 102-03.375. TY saw earlier buying at 110-00 to 110-00+ area, although we trade off those levels now down -02 at 109-30+.

- Volumes: TU 46k, FV 64k, TY 101k

- Tsys Flow: Block Buyer FV at 106-16.75, while there was TYN4 Option structure blocked, 3 strikes of calls and a put. Calls 10k 109/109.5/110.25, Put 10k 108.75

- The 5-10y tenors have been the best performing part of the curve over the past week with the 10y yield has rallying 30bps in the past four trading sessions. Rate cut projections continue to gain, while the BBG Surprise Index reaches multi year lows - See Chart 1.

- Cash treasuries are 1-2bp higher, the 2Y +1.2bps to 4.783%, the 10Y +1.6bps at 4.342%, 2s10s is +0.114 at -44.342

- APAC Rates: ACGB yields are 4-8bps lower, curve flatter. NZGB yields 3-7bps lower, with better buying through the belly, JGB yields a 1-4bps lower, with the 10Y -2.6bps and back below 1% at 0.993%

- Late year rate cut projections continue to gain vs. late Monday levels (*): June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -16% w/ cumulative at -4.3bp at 5.288%, Sep'24 cumulative -19.3bp (-17.2bp), Nov'24 cumulative -27.8bp (-25.3bp), Dec'24 -44.3bp (-40.6bp).

- Looking ahead; MBA Mortgage Applications, ADP Employment Change, S&P Global US PMI & ISM Services Index

Source - BBG

JGBS: Futures Richer & At Session Highs, BoJ Nakamura Speech & 30Y Supply Tomorrow

JGB futures are sharply higher and at session highs, +41 compared to the settlement levels.

- Outside of the previously outlined Labour and Real Cash Earnings and Jibun Bank PMIs, there hasn't been much in the way of domestic drivers to flag.

- (Dow Jones) Japan labour survey data for April confirms that the gradual increase in wage growth continues, ING economists say. "We expect real wage growth to turn positive by June, giving the BoJ more confidence for another rate hike," Robert Carnell and Min Joo Kang say. ING now expects a 15bp BOJ rate hike in July.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session. The US calendar today will see MBA Mortgage Applications, ADP Employment Change and S&P Global US PMI & ISM Services Index.

- Cash JGBs are richer across benchmarks, with yields flat (1-year) to 4.4bps lower (5-year). The benchmark 10-year yield is 3.3bps lower at 0.997% versus the cycle high of 1.101% set last week.

- Swaps are richer apart from the 20-30-year zone, with rates 2bps lower to 2bp higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see Weekly International Investment Flow and Tokyo Avg Office Vacancies data along with a speech from BoJ Board member Nakamura in Sapporo. The MoF also plans to sell Y900mn of 30-year JGBs.

JAPAN DATA: Headline Wages Rise As Negotiated Increases Start To Impact Data

Japan April wage outcomes were firmer than forecast in terms of the headline results. Labor cash earnings rose 2.1% y/y (against a 1.8% forecast and a revised 1.0% March gain). Real earnings were -0.7%y/y, against a -0.9% forecast and -2.1% in March.

- Scheduled pay (not on a same sample basis) rose 2.3% y/y, up from 1.7% in March.

- The Japan authorities will be looking for further improvement in real wage outcomes (trending back above 0%), which is a key policy objective to ensure a recovery in consumption spending and sustainably achieving the 2% inflation target.

- It was a bit more mixed in terms of cash earnings on a same sample base. In y/y terms we rose 1.7%y/y, versus 2.1% forecast and 1.9% prior (which was revised down from 2.2% initially reported). The trend looks a little softer for this metric, but remains above 2023 lows.

- Scheduled full time pay on a same base basis rose 2.1%y/y, in line with expectations and unchanged from March.

- The recently negotiated wage outcomes, where workers secured a +5% wage gain will have impacted today's data. The BoJ suggests around 40% of the annual gain will be reflected in the April data, while 80% will factored in by July (see this BBG link).

RBA: RBA Stance Unchanged And Will Tighten If Inflation Stickier

RBA Governor Bullock remained neutral and reiterated the Board’s stance of not “ruling anything or out” and that policy is “restrictive”. She said that if inflation turns out stickier than expected then the central bank won’t hesitate to raise rates while a lot weaker economy would lead them to ease.

- Removing monetary policy restrictiveness too early would be costly. The RBA won’t begin reducing rates until it is convinced that inflation will return to the band. While the risks to inflation are seen as balanced the consequences are not with the Board more concerned about upside risks.

- When asked about the budget Bullock didn’t comment on whether it was expansionary or not. She doesn’t expect that the energy rebate will impact core inflation or the RBA’s CPI forecasts materially.

- The RBA has noted that monthly CPI is trending higher again but the series is not comprehensive and so it is waiting for the quarterly data, but that makes it difficult to gauge momentum. The Q2 CPI due on July 31 will be important for the RBA’s outlook but Bullock warned that it is a lagging indicator and the bank looks at other data too. Bullock said that they need to step back and watch.

- The economy is not in recession despite weak growth and falling GDP per capita as the labour market is still growing. Unemployment is only rising because the labour force is growing faster than labour demand. Also despite weak growth the RBA believes that demand is still running slightly above supply, which is driving domestic inflation.

- Around 80% of rate hikes this cycle have been passed onto borrowers with the rest of fixed rate loans rolling over this year. The pass through this cycle was slower than previously due to a higher share of fixed loans at the start of the cycle.

AUSSIE BONDS: Richer, RBA Bullock Neutral, Q1 GDP Miss, Productivity Stalled

ACGBs (YM +4.0 & XM +7.5) are richer but have retreated from the Sydney session's best levels. Following a positive lead from US tsys, the domestic market focused on two key events today.

- RBA Governor Bullock remained neutral in her Senate testimony and reiterated the Board’s stance of not “ruling anything in or out” and that policy is “restrictive”.

- Q1 GDP rose 0.1% q/q, the slowest quarterly rate since Q3 2022. Economic growth slowed to 1.1% y/y from 1.6%, the lowest since Q4 2020 and excluding Covid Q1 1992. Imports and investment were a drag on the economy while government and private consumption plus inventories made solid contributions. The RBA was expecting a weak outturn and so this data is unlikely to change its current on-hold stance.

- After two straight quarters of growth, productivity improvements stalled in Q1. GDP per hour worked was flat on the quarter and compared to a year ago but that was up on Q4’s -0.4% y/y.

- Cash ACGBs are 5-7bps richer, with the AU-US 10-year yield differential at -10bps.

- Swap rates are 5-6bps lower, with the 3s10s curve flatter.

- The bills strip has bull-flattened, with pricing flat to +6.

- RBA-dated OIS pricing is 3-5bps softer for meetings beyond September.

- Tomorrow, the local calendar will see Home Loans Value and Trade Balance data.

AUSTRALIAN DATA: Weak Growth But Consumption Made Positive Contribution

Q1 GDP rose 0.1% q/q, the slowest quarterly rate since Q3 2022. Economic growth slowed to 1.1% y/y from 1.6%, the lowest since Q4 2020 and excluding Covid Q1 1992. Imports and investment were a drag on the economy while government and private consumption plus inventories made solid contributions. The RBA was expecting a weak outturn and so this data is unlikely to change its current on hold stance.

Australia GDP %

Source: MNI - Market News/ABS

- In May, the RBA projected 1.2% y/y growth for Q2 and while Q1 is close to this, Q2 GDP will need to rise 0.5% q/q to achieve this.

- Domestic demand was soft rising only 0.2% q/q and making its lowest contribution since Q1 2019 outside Covid. Private consumption rose 0.4% q/q after 0.3% with annual growth recovering to 1.3% from 1.0% in Q4. Essential spending was robust but discretionary outlays on overseas travel and local events rose too. The savings ratio eased to 0.9% due to lower compensation growth. Both public and private expenditure added 0.2pp to growth.

- Investment was a weak spot with private dwelling construction down 0.5% q/q and non-dwelling construction -4.3% but machinery & equipment rising 2.2% after two negative quarters. Private GFCF detracted 0.2pp from growth and public was neutral. The ABS notes that the level of investment is still high and above mining boom levels of the early 2010s.

- Net exports detracted 0.9pp from growth while inventories added 0.7pp. Imports rose strongly +5.1% q/q, highest since Q1 2022, with much of imported goods going into stocks. Exports rose only 0.7% q/q driven by LNG, gold and meat shipments.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Disinflation Measured By Deflators Also Stalled In Q1

The implicit price deflators in the national accounts also stalled in Q1 consistent with CPI developments. While the GDP deflator eased to 2.4% y/y from 2.8% it rose 1.3% q/q, the third straight quarter above 1%. But domestically driven inflation is significantly higher at 4.5% y/y only slightly lower than Q4’s 4.6%. The household consumption deflator picked up to 4.7% y/y from 4.6% and private capex to 3.2% from 3%. Prices paid by the government returned to recent rates at 4.8% y/y. While this data is backward looking, it shows that domestic inflation remained high at the start of 2024 and little disinflationary progress was made.

Australia domestic IPDs y/y%

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Q1 Productivity Flat, Softer Labour Market Should Help It Recover

After two straight quarters of growth, productivity improvements stalled in Q1. GDP per hour worked was flat on the quarter and compared to a year ago but that was up on Q4’s -0.4% y/y. Hours worked were flat and real GDP rose 0.1% q/q. RBA Governor Bullock reminded us today that productivity is volatile and difficult to measure and so it is important to look at it over time. It remains soft but should trend higher. The RBA is forecasting it to rise 1.8% y/y in Q2.

- Unchanged productivity and wage growth around 4% are not consistent with the RBA’s inflation target and it stated at its May meeting that wage growth is “above the level that can be sustained given trend productivity growth”.

- Hours worked were flat on the quarter but have slowed to +0.9% y/y from 2% and that slowdown is likely to continue.

- Another problem with poor productivity is that it adds to unit labour cost (ULC) growth, which adds price pressures. Q1 rose only 0.5% q/q though to be up 5.8% y/y after 1.1% and 6.7% in Q4. They remain elevated but are off recent highs helped by moderating employee compensation growth.

- Assuming hours worked fall over 2024 and then return to trend growth by H2 2025, productivity should improve each quarter to end-2025 resulting in ULC growth moderating to just over 1% by Q1 2025 before returning to 2%.

Source: MNI - Market News/ABS

NZGBS: Closed Mid-Range, Richer, US ADP Data Later Today

NZGBs closed in the middle of the session’s range, 3-6bps richer across benchmarks.

- Outside of the previously outlined Terms of Trade and the Government’s 10-month Financial Statements, there hasn't been much in the way of domestic drivers to flag.

- The move away from the session’s best levels aligns with a ~1bp cheapening in cash US tsys in today’s Asia-Pac session ahead of the release of ADP Private Employment data later today.

- Swap rates closed 2-6bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 1-4bps softer for meetings beyond August. A cumulative 24bps of easing is priced by year-end.

- Tomorrow, the local calendar will see May CoreLogic House Prices, Q1 Volume of All Buildings and May ANZ Commodity Price data.

- Today, the NZ Treasury launched the syndicated tap of May 2028 nominal bonds, seeking at least NZ$2bn this week. Transaction will be capped at NZ$4bn and priced tomorrow. Initial guidance 3-6 bps under April 2027 nominal bond. The June 6 bond auction is cancelled.

FOREX: Yen Unwinds Some Of Tuesday's Bounce, A$ & NZD Slightly Higher

The BBDXY USD index sits little changed, last near 1252.65. This has masked some divergences within the G10 space though. Most notable has been yen unwinding some of Tuesday's outcomes.

- USD/JPY sits back near 155.50, around 0.40% weaker in yen terms and close to session highs. We had mixed April wages data, with better headline results (boosted by annual wage outcomes of +5%), but the same sample basis was softer than forecast (see this link).

- For the FX pair we still remain comfortably off earlier Tuesday highs near 156.50. US yields are up a little over 1bps, while US equity futures sit higher.

- AUD and NZD are firmer against the USD by around 0.15%/ AUD/USD last at 0.6660, NZD/USD near 0.6185.

- We had a better than expected Caixin services PMI print in China, although follow through has been limited in terms of risk appetite. China equities are lower and HK markets sits comfortably off earlier highs.

- AUD/JPY sits just off session highs, last near 103.55/60. Earlier highs this week were above 104.70. Australian Q1 GDP was slightly below expectations (0.1% q/q, versus 0.2% projected), although private consumption proved more resilient than expected.

- Looking ahead, US ADP, the BOC and ISM Services are coming up. The ECB decision on Thursday and NFP Friday remain key event risks for the remainder of the week.

ASIA STOCKS: HK Equities Outperform Although Off Earlier Highs, China PMI Jumps

Hong Kong & Chinese equities are mixed today, with Hong Kong markets outperforming for the second straight session after a weak US jobs reading increased the hopes for a Federal Reserve interest rate cut. China Caixin PMI grew at the fastest growth in 10 months

- Hong Kong equities are higher today although well of morning highs, tech stocks are the top performers today with the HSTech Index up 0.80% and now trading back above all major EMAs. Property Indices are now lower for the day with the Mainland Property Index down 1.10%, the HS Property Index down 0.60%, the wider HSI is up 0.33%.

- China equites have underperformed today, the CSI300 is now down 0.20% with small-cap indices the CSI1000 and CSI2000 are down 0.30% and 1.10% respectively, the CSI300 Real Estate Index is off 1.80% while the growth focused ChiNext Index is up 0.12%

- Data: Hong Kong S&P Global PMI was 49.2 in May dropping from 50.6 in April, while China Caixin PMI composite for May was 54.1 up from 52.8 in April, and Services PMI was 54.0 vs 52.5 est.

- In the property space, DaFa Properties group have had their wind-up hearing adjourned until June 24.

- (MNI): MNI China Press Digest June 05: A-shares, EU-China, SOEs (See link)

- Looking ahead: Tomorrow we have China Trade Balance data.

ASIA PAC STOCKS: Equities Mixed, Japan Equities Lower On Higher Yen, AU & SK GDP Miss

Asian equities are mixed today, Japan is the worst performing region as the yen strengthens and hurts export names, while other markets edge higher on hopes of a fed rate cut. The Philadelphia Semiconductor index was 0.70% lower overnight, although news that Nvidia is working to certify Samsung's AI memory chips has seen Samsung rally about 3% this morning and helped other region semiconductor names. Indian equity markets have stabilized after selling off over 5% on Tuesday as election results look to be much closer than expected. Earlier, SK & Australian GDP came in just below estimates.

- Japanese equities are lower today, the yen is off overnight highs, but still 1.46% higher over the past week. Earlier, Labor Cash Earnings were 2.1% vs 1.8%, while Jibun Bank Japan PMI Composite was 52.6 vs 52.4 prior and Services were 53.8 vs 53.6. The Topix is down 1.47% and now testing the 20-day EMA support at 2,750, The Bank Index is down 2.29%, while the Nikkei 225 is down 1.12%

- Taiwan equities have edged higher throughout the day, the local market has seen the majority of outflows in the region, with another $528m outflows on Tuesday. Looking ahead we have CPI on Thursday. The Taiex is up 0.50%.

- South Korean equities have gained on fed rate cut expectation gains and Samsung rallying on the back of news that Nvidia is working to certify their AI memory chips. Earlier, GDP came in slightly below consensus at 3.3% vs 3.4%. The Kospi is up 1.20% and now testing the 20-day EMA resistance at 2,690, while the Kosdaq is up 0.47%.

- Australian equities are slightly higher today, Banking stocks are the top performing sector today, while metals and mining underperform. Earlier Judo Bank PMI showed a slightly decline, with composite at 51.1 vs 52.6 prior and services 52.5 vs 53.1 prior, while GDP came in below consensus at 1.1% y/y vs 1.2% est. The ASX200 is 0.38% higher.

- Elsewhere in SEA, New Zealand Equities are 1% higher, Singapore equities are 0.25% higher, Indonesian equities are down 1%, Philippines equities are down 0.10% after CPI came in below consensus at 3.9% vs 4% est, Malaysian equities are 0.20% lower, while Indian equities have found some support after the 5% sell-off on Tuesday and trade little changed today.

ASIA EQUITY FLOWS: Foreign Investors Continue To Sell Asian Equities

- South Korean equities followed global markets lower as concerns grow about a slowdown in the US economy, while SK CPI came in below expectations at 0.1% vs 0.2% m/m. Today, we had GDP which missed consensus at 3.3% vs 3.4% y/y. Foreign investors have been better sellers of local stocks recently as they look to take profits, the past 5 sessions have seen an outflow of $1.96b. The 5-day average is now -$392m, well below the 20-day average of -$25m, and the longer term 100-day average at $132m.

- Taiwan equities were lower on Tuesday, we bounced off the 20-day EMA on Friday and have managed to hold above despite heavy selling from foreign investors as the past 5 sessions have seen an outflow of $3.9b. Local price drivers this week will be CPI on Thursday. The 5-day average is now -$787m, well below both the 20-day average at $69m and the 100-day average is $22m.

- Thailand equities were lower again on Tuesday, and the SET is now testing yearly lows made on Apr 19th. Foreign investors have sold equities for the past 9 sessions, with the past 5 seeing a net outflow of $352m. Focus this week will be on CPI due out on Friday. The 5-day average is now -$70m, below both the 20-day average at -$22m and the 100-day average at -$23m.

- Indonesian equities have now marked 9 straight sessions of selling from foreign investors, with the past 5 session seeing a net outflow of $197m. Looking at technicals, the JCI briefly traded above the 200-day on Tuesday, before closing just below it. The 5-day average is now -$39m, below both the 20-day average at -$44m and the 100-day average at -$1.10m.

- Philippines equities also continue to see selling from foreign investors, we have now marked 7 straight days of selling, with the past 5 sessions seeing a total outflow of $148m. The PSEi ended Tuesday back below the 6,400 level and back near ytd lows. The 5-day average is -$29.6m, below the 20-day average at -$8.5m and the 100-day average at -$4.82m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -73 | -1960 | 13464 |

| Taiwan (USDmn) | -528 | -3937 | 2221 |

| India (USDmn)* | 824 | 690 | -1937 |

| Indonesia (USDmn) | -3 | -197 | -353 |

| Thailand (USDmn) | -61 | -307 | -2342 |

| Malaysia (USDmn) ** | -104 | -264 | -160 |

| Philippines (USDmn) | -89 | -148.1 | -455 |

| Total | -35 | -6123 | 10437 |

| * Data Up To June 3 | |||

| ** Data Up To May 31 |

OIL: Crude Steady, EIA US Inventory Data Out Later

Oil prices are little changed during APAC trading today after falling for the last few days after OPEC decided on the weekend to reduce output cuts from October, which was earlier than expected. Higher US stockpiles have not put further downward pressure on crude today. WTI is around $73.21/bbl after a high of $73.34 and Brent is $77.52/bbl after reaching $77.64 and both benchmarks are down around 5% this week. The USD index is slightly higher.

- Oil prices are likely to face headwinds through 2024 as demand from China is looking soft and the Fed may not cut rates until year end pressuring US demand. There is also strong supply from non-OPEC countries and increased output from OPEC+ in Q4 will add to that, but the group may change its plan to reduce production cuts if prices look weak.

- Bloomberg reported a 4.1mn barrels crude inventory build in the US compared with a 6.5mn drawdown the previous week according to people familiar with the API data. Gasoline rose 4.0mn barrels and distillate 2mn. The official EIA data is released later today.

- Later US May ADP employment, final May US & European composite/services PMIs/ISM, euro area April PPI and the Bank of Canada decision are released. The focus for the oil market now the OPEC meeting is behind it will be Friday’s US May payrolls and the June 12 Fed decision.

GOLD: Weaker Despite Softer US Labour Market Data

Gold is 0.4% higher in the Asia-Pacific session, after closing 1% lower at $2327.01 on Tuesday.

- Tuesday’s move came despite softer US labour market data. JOLTS Job Openings printed 8.059M vs. 8.350M est and 8.488M prior. The result was the lowest since Feb 2021.

- US Treasuries rallied for the fourth successive day, although they finished slightly off session highs amid late position squaring ahead today’s ADP private employment data risk, a precursor to Friday's headline employment report.

- Silver underperformed, falling by ~4.0%, its lowest level since May 17. Silver is now trading within a key support zone between $30.116 - 28.494, the 20- and 50-day EMA values, according to MNI’s technicals team.

- (Bloomberg) UBS Group AG sees gold hitting $2,800 an ounce over the next two years, with continued macro uncertainty and geopolitical risks set to drive continuing strong demand from global central banks. (See link)

PHILIPPINES DATA: CPI Close To Expectations, Core Inflation Moderates, But Rice Inflation Still High

Philippines May CPI was a touch below expectations in terms of the headline result. We printed at 0.1% m/m (0.2% forecast and -0.1% prior), while the y/y print came in at 3.9%, versus 4.0% expected and 3.8% prior.

- Core inflation was 3.1% y/y down from April's 3.2% pace. This metric is closer to the mid-point of the BSP's target band of 2-4%, than the headline outcome.

- Rice prices rose 23% y/y and is expected to remain elevated in the near term. The market will be waiting on details around a reportedly reduced tariff for rice (from 35% to 15%). Details remain light in terms of when this will be implemented but this could help alleviate headline food/aggregate inflation pressures

- Aggregate food prices rose 5.8% y/y, versus 6.0% in April. Housing/utilities, along with transport, were the only categories to see a firmer y/y pace compared to April.

- In m/m terms we saw a modestly firmer backdrop for most of the sub-categories, although transport fell -0.5%m/m.

- The BSP stated that May data was in line with expectations and that average 2024/2025 inflation is expected to be on target. Governor Remolona stated that risks to the inflation outlook still rest to the topside. The next BSP meeting is on June 27.

INDON Sov Curve Twist-Flattens, Spread Continue to Widen

The INDON sov curve has continued it twist-flattening move, again seeing better buying at the 7yr. Spreads continue to widen as US treasuries yields move 10-30bps lower across the curve.

- The INDON curve has again twist-flattened today, yields are 2-6bps lower, the 2Y yield is -2bps at 5.245%, 5Y yield is -3.5bps at 5.04%, the 10Y yield is -4bps at 5.125%, while the 5-year CDS is 1bps higher at 72.5bps.

- The INDON to UST spread diff the 2Y is now 47bps (+2bp), 5yr is 69bps (+3bps), while the 10yr is 78.5bps (+2.5bps). the INDON curve has widen 10-15bp to the UST curve over the past week.

- In cross-asset moves, USD/IDR is nearing ytd highs after trading up 0.35% today to 16,275/80, the JCI has managed to get back above 7,000 however has been unable really tests the 200-day EMA, while US tsys yields are 0.5-1bps higher..

- Looking ahead, it is a quiet week with just Foreign Reserves for May on Friday.

ASIA FX: IDR & CNH Lag Broader USD Weakness, THB Shrugs Off BoT Independence Uncertainty

USD/Asia pairs are mixed. We saw a softer USD trend earlier in the session amid positive equities, but most pairs sit up from session lows. CNH and IDR have lost ground against the USD as well, underperforming the rest of the region. USD/THB spiked higher on headlines around a loss of BoT independence, but the move drew selling interest. Tomorrow, we have the Philippines unemployment rate and Taiwan CPI figures on tap.

- USD/CNH has firmed a touch, back to 7.2540 this afternoon. A weaker yen, coupled with onshore equity market weakness has weighed, offsetting a stronger than expected Caixin services PMI print, which rose to 10 month highs.

- 1 month USD/KRW got sub 1366 in earlier dealings, testing 20-day EMA support, but we sit slightly higher now (last around 1367). Onshore equities are higher, up over 1%, but broader risk sentiment is off post Caixin services PMI highs. Q1 GDP revisions were down a touch in y/y terms.

- USD/THB hit highs of 36.69 post headlines from BBG that the Thailand government would look to exert more influence on the central bank, the BoT. The pair sits slightly lower now, back at 36.55/60, so slightly weaker in USD terms for the session. Bloomberg states that the Thailand Government will look to nominate a more friendly BoT Chair person in September 2025 (when the position becomes available). The Chair can't influence monetary policy decisions as they don't seem to be a member of the MPC but can evaluate the governor's performance and weigh in on potential outside board member appointments.

- USD/INR is tracking modestly lower in early Wednesday dealings. We are back under 83.50, but only 0.1% stronger in Rupee terms. Tuesday highs were around 83.53, which were just below earlier YTD highs of 83.575. Yesterday saw a near 6% fall in onshore equities, the largest drop in 4yrs as Modi's government failed to secure an outright majority. A coalition around Modi's BJP-led alliance will be needed for Modi to continue as PM. Offshore investors sold around $1.5bn of local equities yesterday, nearly double the inflows seen on Monday's session (when exit polls suggested a strong Modi win). Early tones for equities look better today.

- USD/IDR got to fresh highs back to 2020 in early trade, touching 16290. We sit slightly lower now, last near 16270, still 0.30% weaker in IDR terms. The rupiah has underperformed the softer US yield backdrop in the past week or so. The US 10yr real yield is off more than 20bps from recent highs but this is yet to aid the IDR. To be sure, other cross asset signals are working the other way. Local equities are struggling to hold above the 7000 level and remain under the simple 200-day MA. Offshore investors have sold just over $2bn of local equities in Q2 to date, although outflows in June so far have been light. BI stated late yesterday that the FX should average 15700-16100 for 2024. The current YTD average is 15831, so slightly sub the 15900 midpoint expected by the central bank. Next year BI sees an average of 15300-15700

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/06/2024 | 0645/0845 | * |  | FR | Industrial Production |

| 05/06/2024 | 0900/1100 | ** |  | EU | PPI |

| 05/06/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 05/06/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 05/06/2024 | 1215/0815 | *** | | US | ADP Employment Report |

| 05/06/2024 | 1345/0945 | *** |  | CA | Bank of Canada Policy Decision |

| 05/06/2024 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 05/06/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 05/06/2024 | 1430/1030 | | CA | BOC Governor Press Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.